Highlights of Piramal Enterprises Q32024 result –

Prima Facie does not look exciting but if you look deeper, there is a lot of positivity and resilience. Obviously long playout story but seems like narrative and promises made since last few years remain intact.

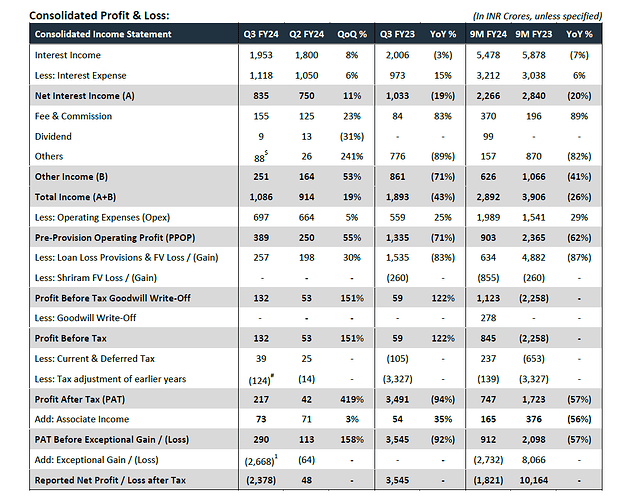

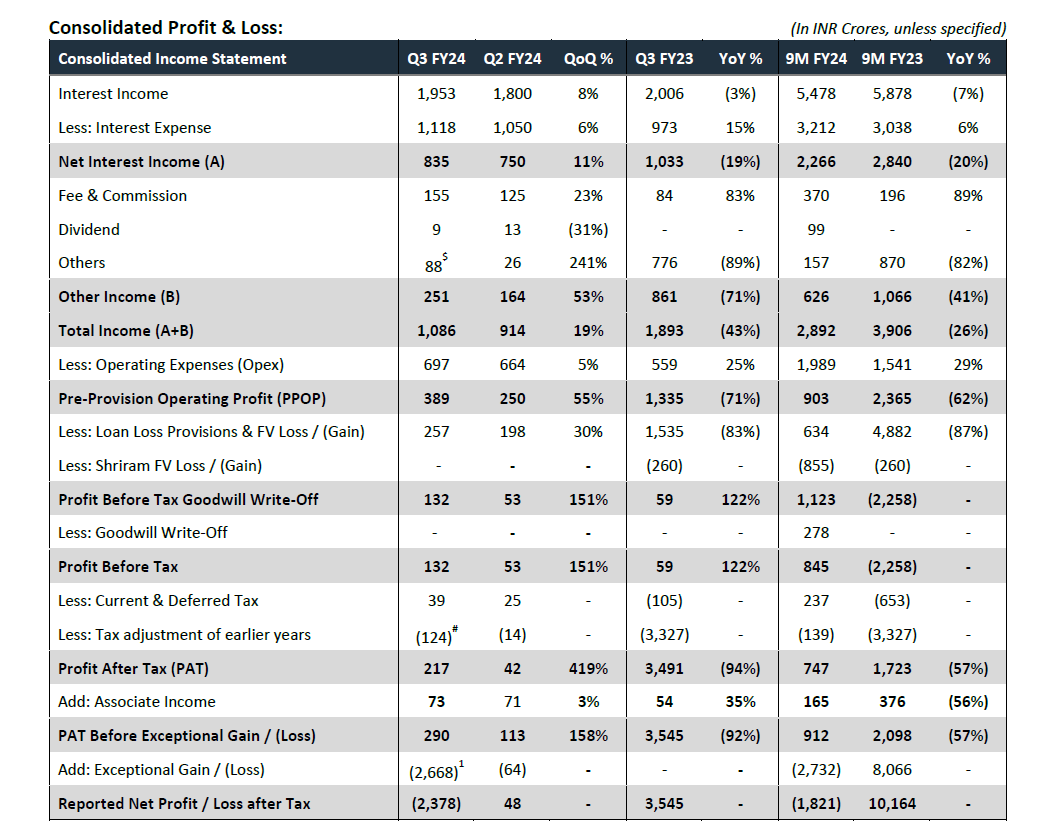

- Reported Net Loss of INR 2,378 Cr (vs PAT of INR 48 Cr in Q2 FY24) after the impact of AIF provision. AIF provision, on post tax basis, is 2668 Crores.

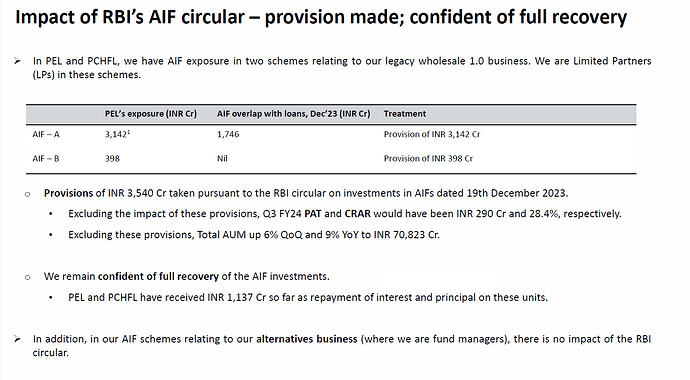

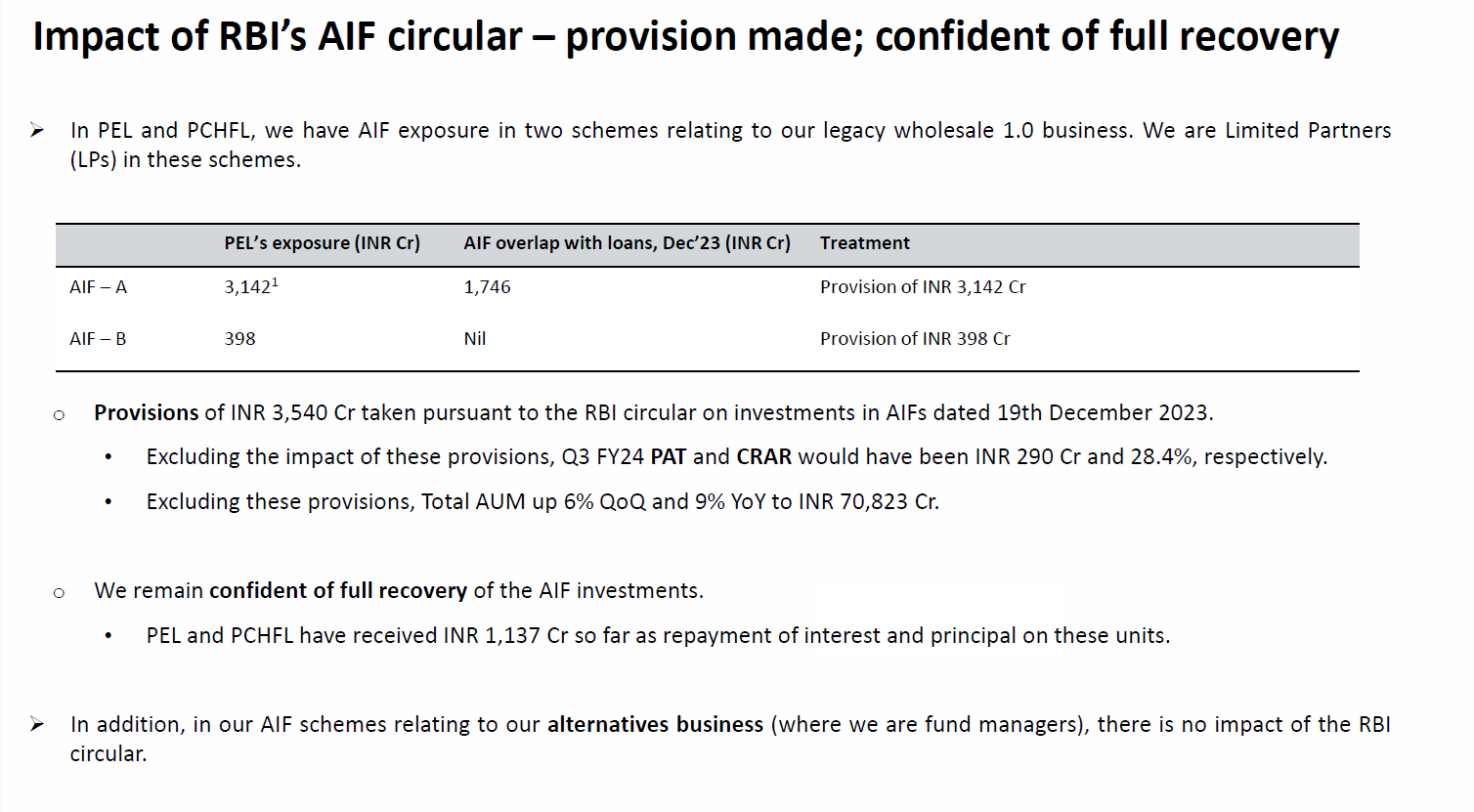

Noteworthy slide attached – Provisions of INR 3540 Cr taken pursuant to the RBI circular on investments in AIFs dated. Management is confident of full recovery of AIFs – have received INR 1137 Cr so far as repayment of interest and principal on these units.![]()

-

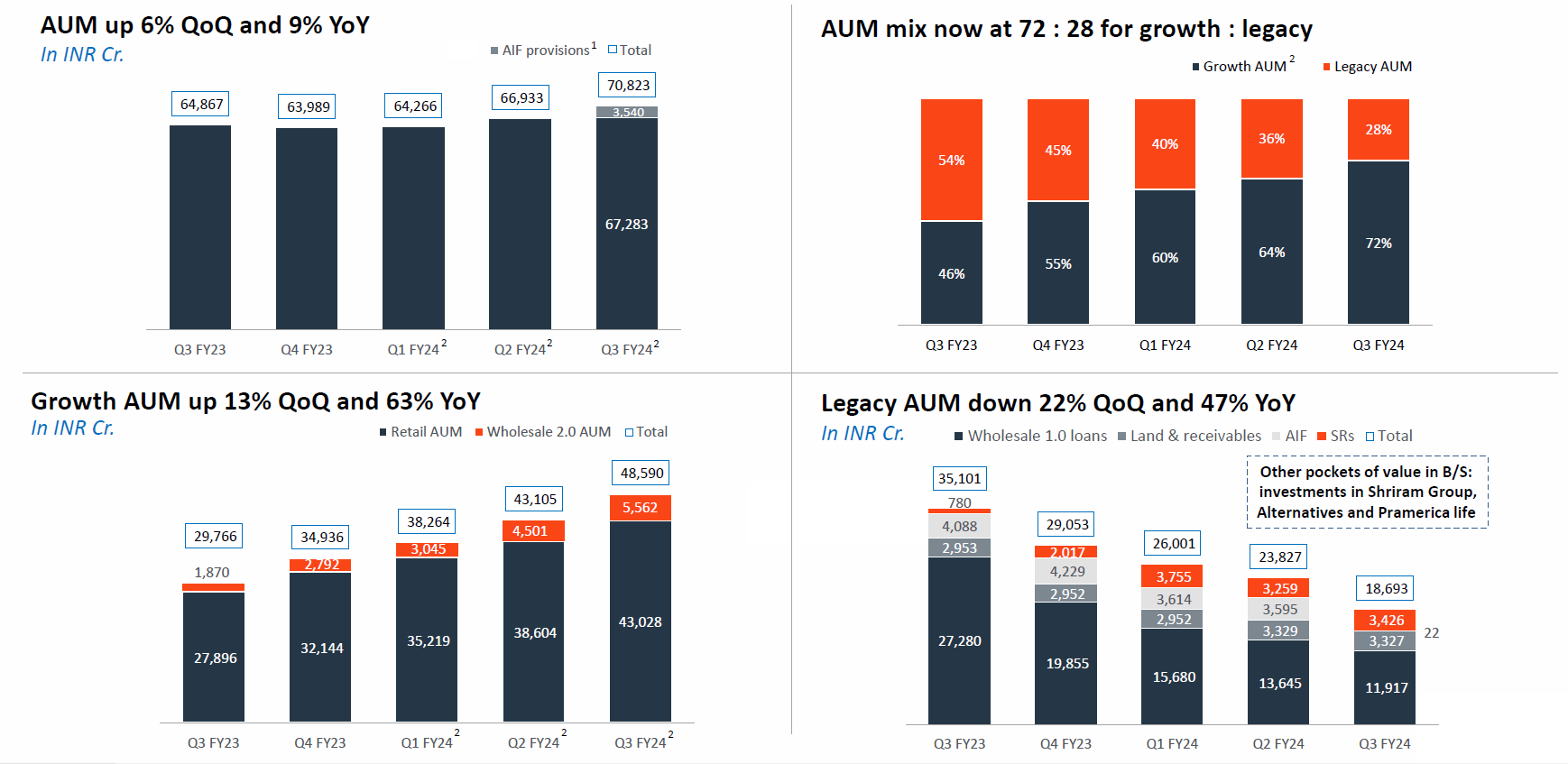

Growth Book AUM

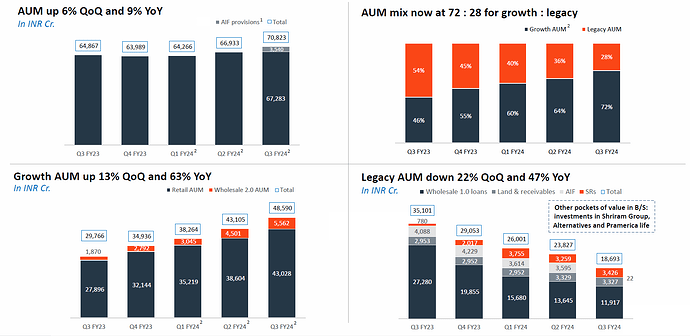

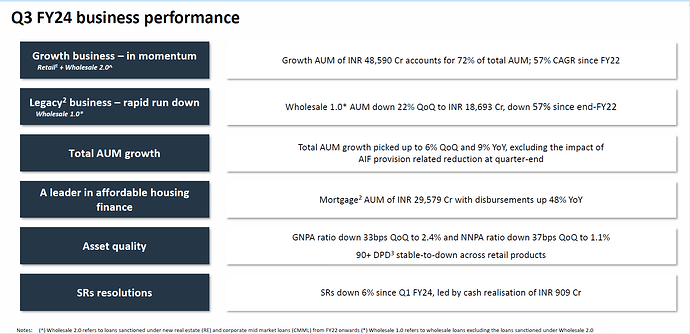

Retail AUM grew 54% YoY

Mortgage AUM grew 27% YoY – contributing 72% to Retail AUM.

-

Growth Book Disbursements

Quarterly disbursements grew 50% YoY

Mortgage disbursements grew 48% YoY -

Wholesale 2.0 AUM grew 24% QoQ

-

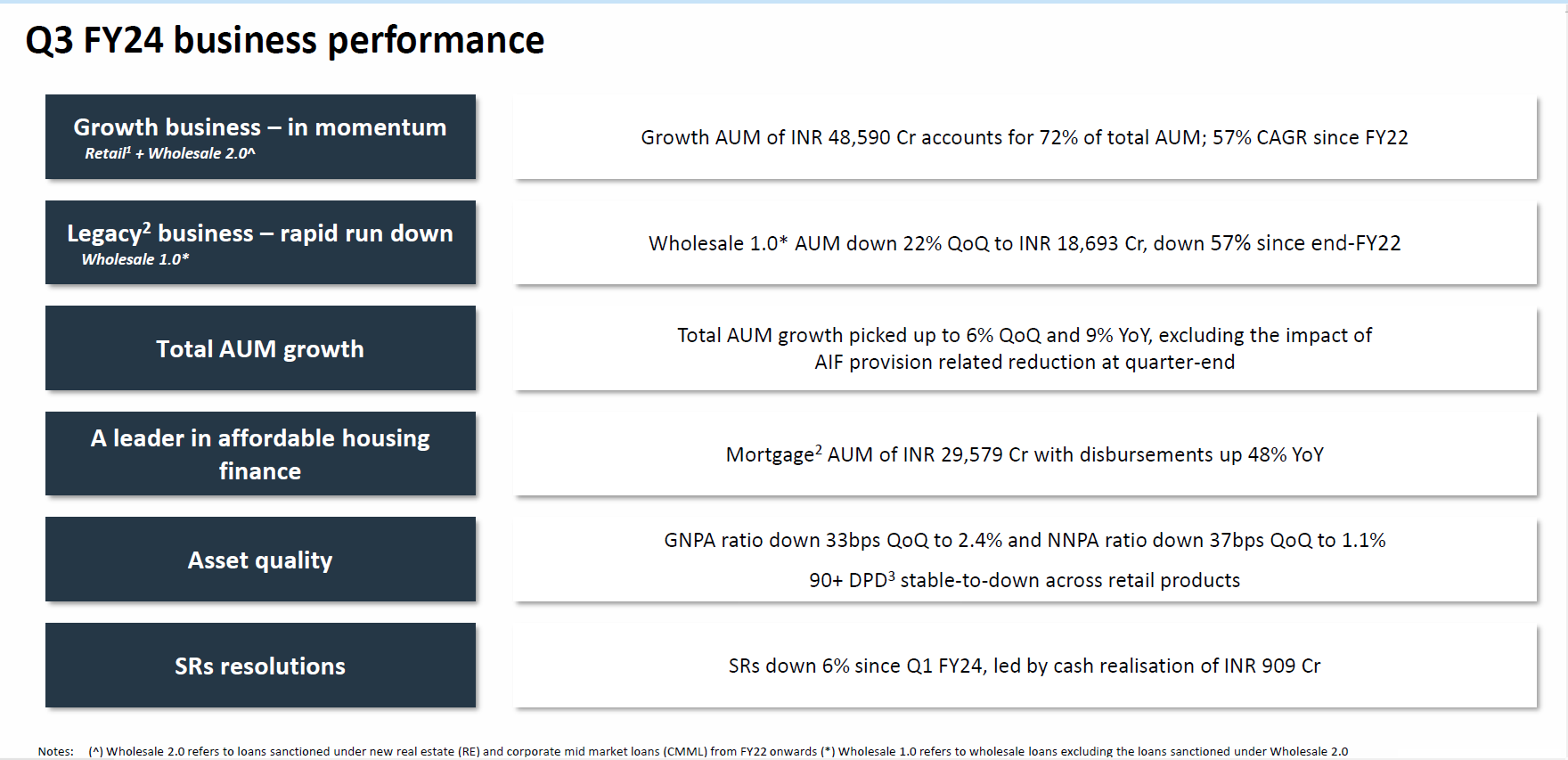

Wholesale 1.0 AUM reduced 47% YoY to INR 18,693 Cr and management is continuing to guide rapid rundown of legacy book over coming quarters also

-

GNPA ratio down 33bps QoQ to 2.4%

NNPA ratio down 37bps QoQ to 1.1% -

Net worth stood at INR 26,376 Cr with capital adequacy ratio at 24.3% on consolidated balance sheet. Announced sale of INR 1,440 Cr from Shriram investments (carrying value of INR 569 Cr) – expect

closure in Q4 FY24; the proceeds from the transaction will further strengthen balance sheet -

Wholesale stage 2 3 assets are down 54 YoY to INR 4 721 Cr with PCR of 32 unchanged QoQ

-

OpEx is gradually moderating – reduced from 6.5% to 5.6% in last four quarters. Long term goal of 3-4%

-

ALM is well-matched with positive gaps across all buckets. Strong positive in a competitive environment.

| Subscribe To Our Free Newsletter |