Some insights from Bharat Wire Ropes Q3FY24.

Organized scrappily to save time. Source: [Concall Q3FY24]

Sales mix and customer insights

80% of revenues from exports. Most of the products are sold through distributors. Management could not ascertain which sectors were driving the demand. The commentary was generic – “getting good traction from all sectors”. Mgmt indicated they don’t have unique SKUs for different applications such as O&G and Marine.

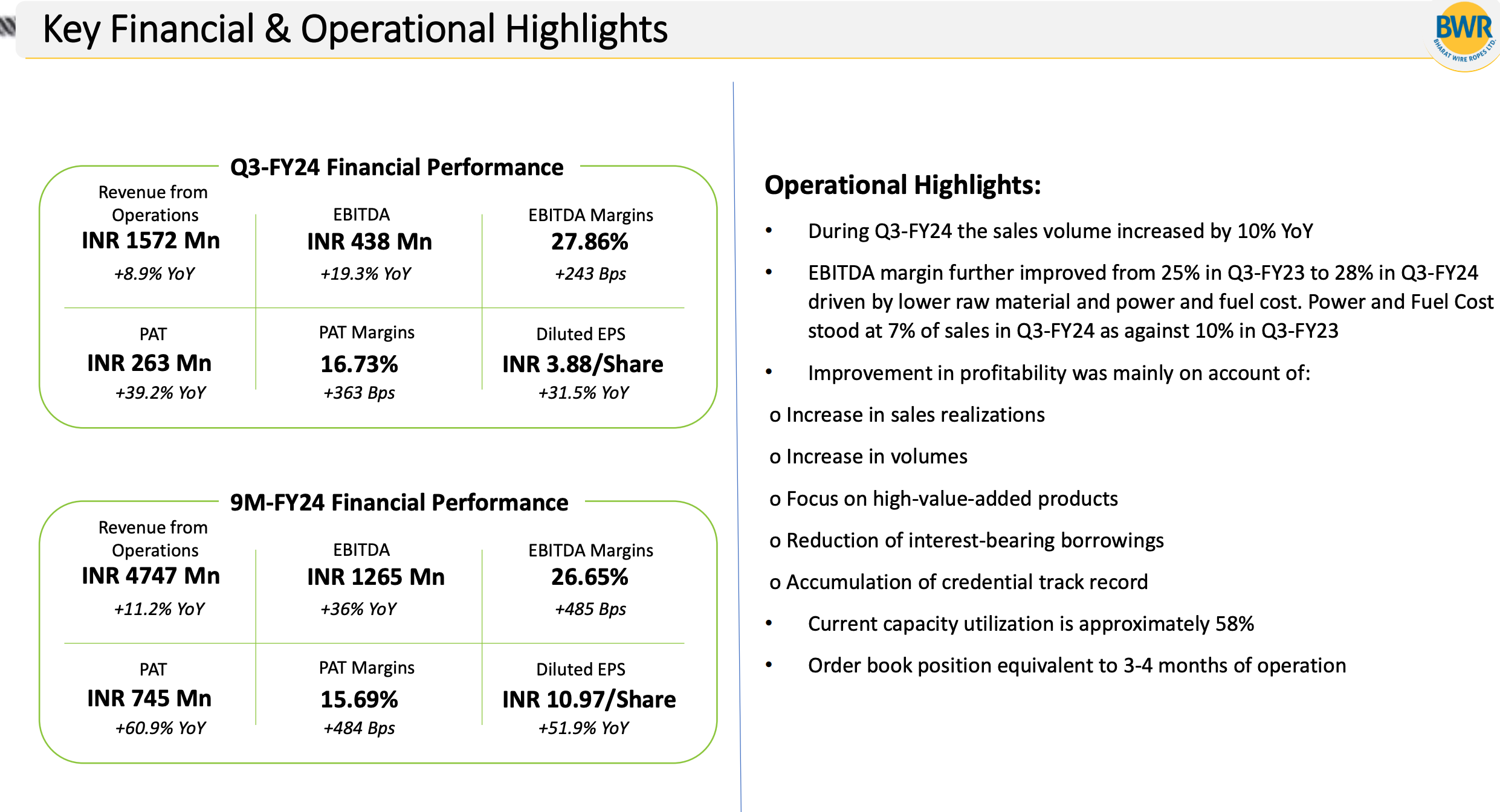

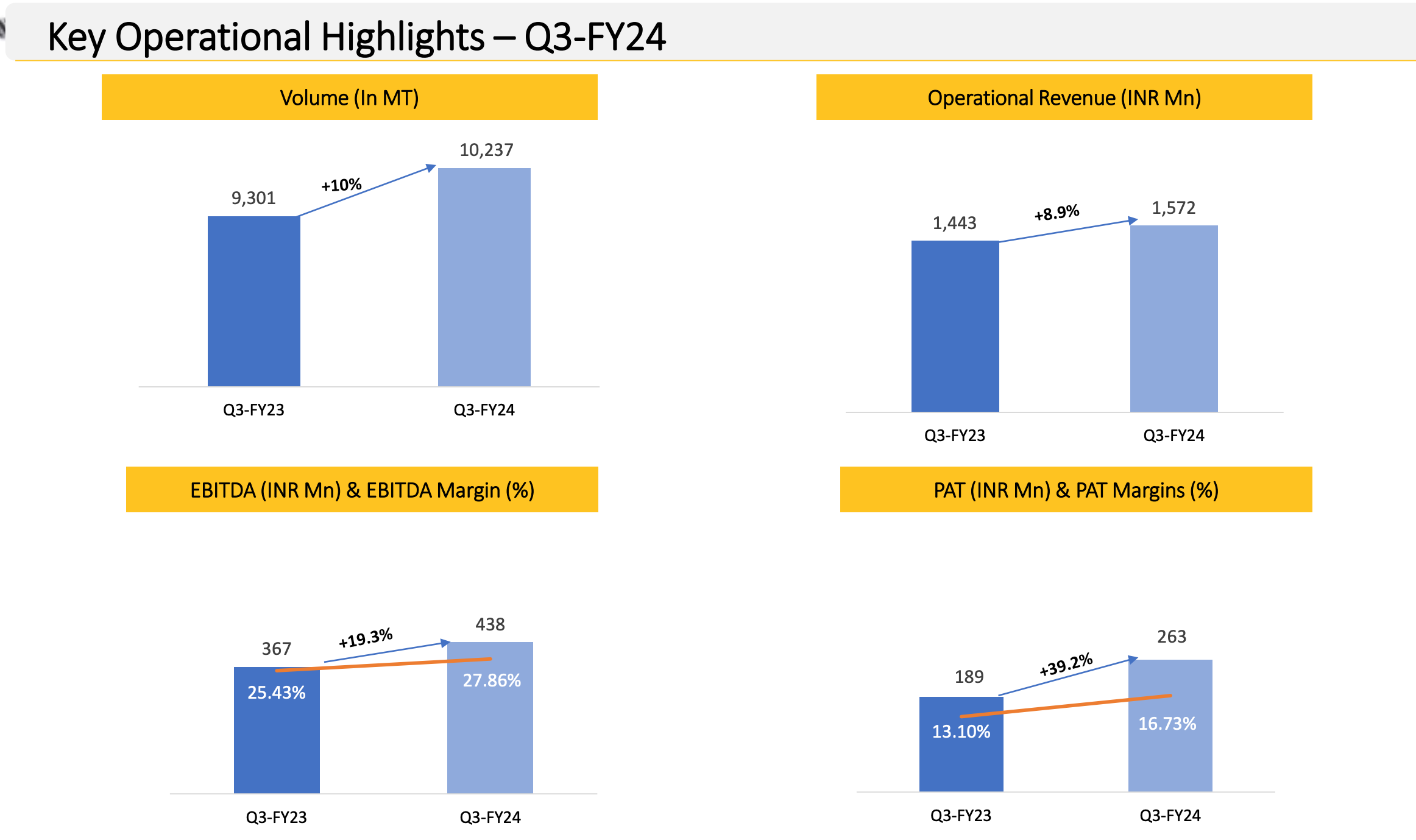

Growth: Steel and product prices declining over the last few qtrs. Volumes have gone up. The company is increasing its global footprint, distribution, and working on new product lines. Expects 20% of revenues from special ropes in the next 2-3 years.

Cap utilization

- The strategy is to increase cap utilization from 60-65% to 80+% by de-bottlenecking.

- This will cost 25-30 Cr over the next 18-24 months.

- ROCE/Asset turns on capex: No clue.

- Capex: Only on the drawing board.

Competition: No clear answers on competition and the supply scenario.

Current order book: 150 cr, 2-3 months

EBITDA margin expansion over the last 2-3 years: We’ve achieved these numbers by putting numerous efforts – sales efficiency, product mix, cost controls. This business is asset heavy and asset turnover is low.

Q: Why are you being conservative?

A: Wire rope is a conservative product. Buyers don’t switch brands easily. We’re continuously adding new customers and products. We’re participating in conferences and exhibitions at global level.

Disclaimer: Invested

| Subscribe To Our Free Newsletter |