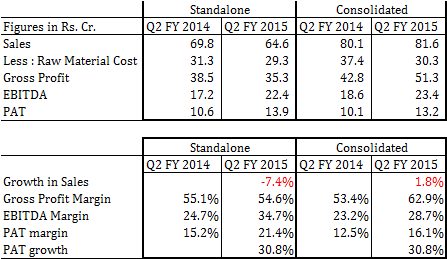

Q2 FY2016 results are out : strong improvement in gross profit margin (all thanks to USA plant) and hence meaningful PAT growth of 30% y-o-y and q-o-q both. In fact, PAT growth is so strong that H1 FY2016 PAT of Rs. 23 cr. is ~42% higher than H1 FY2015 PAT of Rs. 16.5 cr!!

Key questions which come to mind –

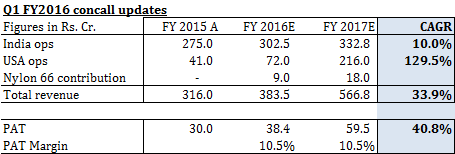

1. Why is there no sales growth from India plant?

2. Gross profit margin at USA plant seems very high. Are they sustainable?

3. For FY2016 guidance, it seems management will over achieve its PAT guidance very easily. However, will it be able to achieve sales guidance?

4. Are we on track to start commercial production of Nylon 66 plant at Silvassa?

5. The big client from USA, who had approved yarn package supplies from Sarla’s USA plant, did that dialogue progress?

6. Any other meaningful update at USA plant?

| Subscribe To Our Free Newsletter |