My takeaways from the conf call ( any mistakes are truly mine, as they were my running notes ):

- Highest EBITDA ( but on lower production volumes). Have been able to control costs.

- There is spending in O&G sector, and orders are getting topped up.

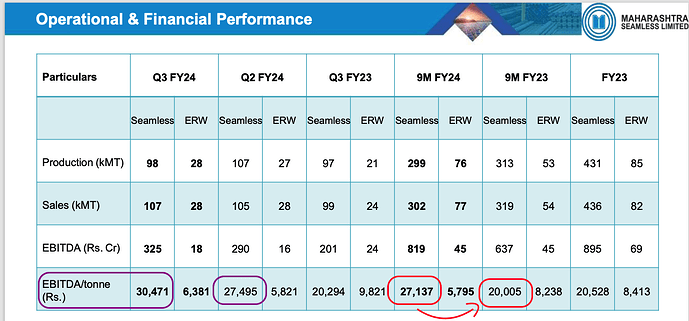

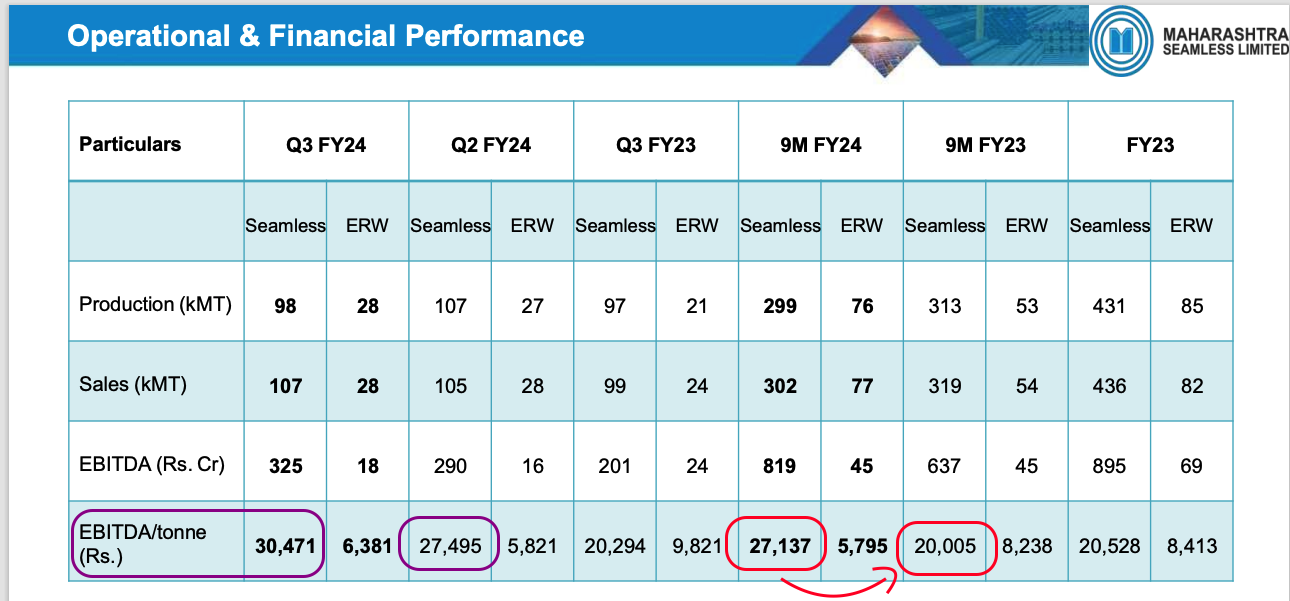

- Seamless pipe product down by approx 10% to 98 kMT from 107 QoQ but sales have been higher, indicating higher price for seamless pipes. Ebitda/tonne has also increases Q, Y and 9m YoY too.

- Domestic demand is high. Exports is only 10% and has not picked up over last 9 months, domestic has compensated. If we wanted to get export order, we could have gotten it by reducing the prices/margins, but we had more than enough domestic orders and hence export is lower.

- Promoter stake has increased over the past 2 years from 63 to 68, when will it improve to 75? No timeline, but would like to get to 75%

- Order book: 1563 cr.

- Orders are typically 3-4 months only

- why is there an increase in EBITDA/Tonne:

- Good domestic market. Export started declining from April of last year, and our margins started increasing from the same time. This indicates the domestic market is good and is indicative of higher margins.

- RM prices have declined. Steel price has come down. When the tender from ONGC came 3 months back and we book RM at a lower price. Not all or 100% of RM is booked, hence lower steel [RM] prices have helped in this quarter.

- FY25 the EBITDA/tonne will go back to 20,000 and will not sustain at 30,000 level. FY24 might close closer to 27,000 levels but FY25 will be lower. [ this year was more opportunistic – volatile market, higher prices for end product and RM was lower ]

- No plans for deploying cash back to shareholders. No opportunities seen yet for buying other companies, we are ‘hoping’ for an opportunity. Dividends plan will be in consideration.

- ONGC comes out with lower value and lower duration order, compared to in the past when it was a large one and for a full year out, unlike today where its for 3-4 months.

- We are one of 3 participants and are the market leader, we will get good orders.

- Exposure to oil and gas segment is 70% other area we cater too are: boiler and general engineering. Power sector uses boiler segment.

- ERW margins are going down. Two types of sectors for ERW we cater to: Oil and water. Depending on the sector, the margins fluctuate. Oil ERW has better margins than water ERW.

In my view, given that the margins are at an elevated level and the mgmt has stated that the EBITDA might not sustain at these levels of 30k and might revert to 20k levels in the next financial year, I have sold most of my holdings. Have transactions in the past 30 days.

| Subscribe To Our Free Newsletter |