Q3 FY24-

Added 7 new branches during Q3FY24 across AP,Delhi,Karnataka and TN.

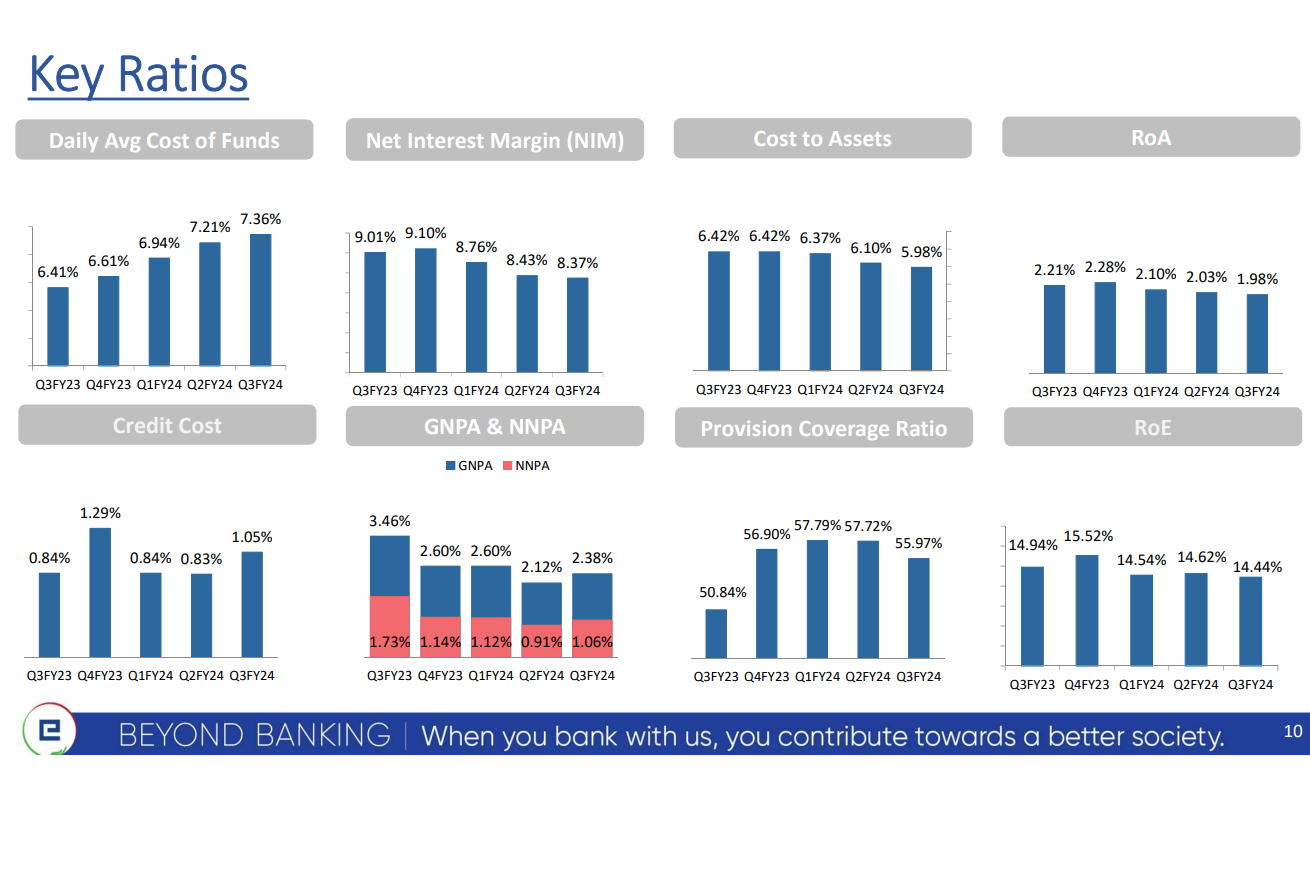

GNPA and NNPA increase bcz of flood in TN(temporary issue).

Yes, the pressure on CASA will continue to be there.

launch of credit card.

No new branch expansion, earlier expanded branch will become profitable in 2-3 years which increase our revenue.

NIMs will be at 8% in FY24

- And in the beginning of the year, we had mentioned that for this current financial year, we should be looking at around 8.5% NIM for the full year as a whole and also a possible 8.25% exit NIM for the fourth quarter.

So see, if you – last year, we had guided on a credit cost of 1.5%. And we landed at about 1.56%. This year, we feel that our credit costs will be at around 1.25%.

So our nine-month credit cost run rate is 90 basis point-odd. And when we are saying our full year guidance is 1.25%, does it mean that Q4 will be higher in terms of credit cost?

I mean, if you remove some of the Black Swan years, otherwise, historically, our credit cost has always remained in the 1.1% to 1.2%.

Yes, see, we don’t want to sacrifice NIM for the sake of only top line growth. So some of the low-yield products, we have stopped focusing. And we have focused on our high-end products. That is a yes. So the last year, we had the opportunity to do a lot of NBFC funding. And we did get our rates.

And this is the first quarter after last 2, 3 quarters, I think, we have shown growth in SA also. And the increased focus on ASBA as well as trading account, I think we should develop that module. The differentiated solution in current account, for example, virtual account numbers and solution-centric approach, along with TD suite is helping us to grow the CAR account to the current accounts.

One is our AD-I project and the other one is credit card launch. The AD-I project is underway and there’s going to be some amount of investments we need to make both on tech and on people to get us enabled and ready to commence that business. And credit cards, again there’s going to be an investment both on tech and on people before the product will go live.So these are the two products where some investments will come shortly in the future. But otherwise, if you see branch expansion, as we have mentioned in the past also, we have put up a very large number of branches quite early on. And so thankfully, the cost of increasing our network of branches is behind us. So that is not something you should see – for the next at least 2 to 3 years, you won’t see too much of increase in cost because of branch expansion.

That’s one thing. Second thing is that other than these two new products, so credit card and AD-I, we don’t really see any particular new /other new products coming into the system. So there is most of the products that we have already invested and many of the products will become profitable across their loss-making cycles and become profitable. The affordable housing is still at an early stage. But this year, they should break even and the next 2 years, they should be pulling their full weight in the system. So minus credit card and the AD-I, we are all really not looking at any other major product investment.

Next quarter, when we come back, we will give you the data. Yes, we will give you a good amount of idea of the kind of money that we are going to invest in these two and also give you some maybe a ballpark idea in terms of the launch date and also the likely break-even time span. So we’ll give all of that in the next call.

Our slippages have increased slightly for the reason that there have been heavy floods in Tamil Nadu. And primarily, slippages have gone up in vehicle finance and micro finance. But if you look our slippages, they have always been range-bound between 3% to 4%. I think this is we feel that this is normal and 3% to 4% is a range-bound for our business.

l deposit mobilized during the third quarter, about 80% of them came from retail term deposits. The franchise is coming up well. And over the next few years, our strategy is to move to a customer segment approach from a product segment approach, which should help us deepen our offering for families, NRIs and digital-savvy customer segments.

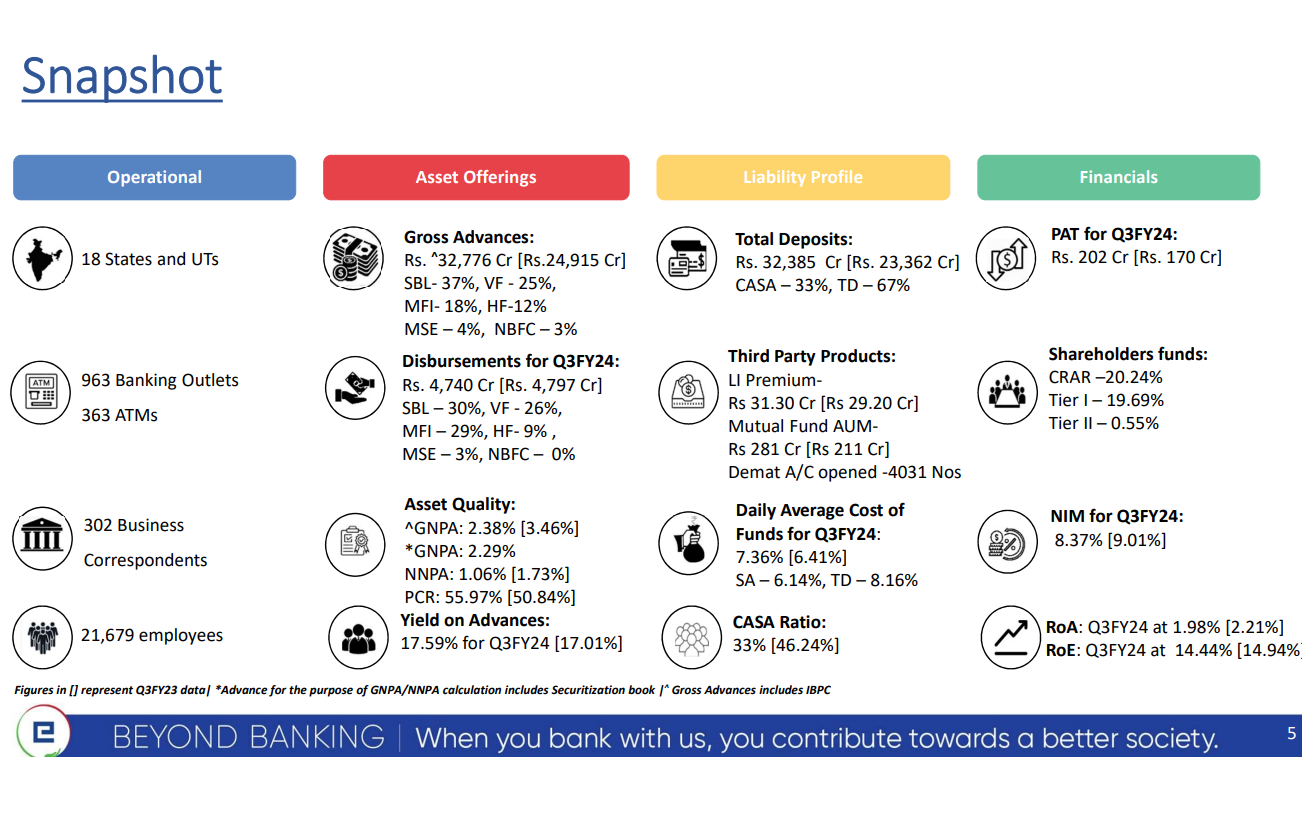

RoA – 1.98 and RoE- 14.44%.

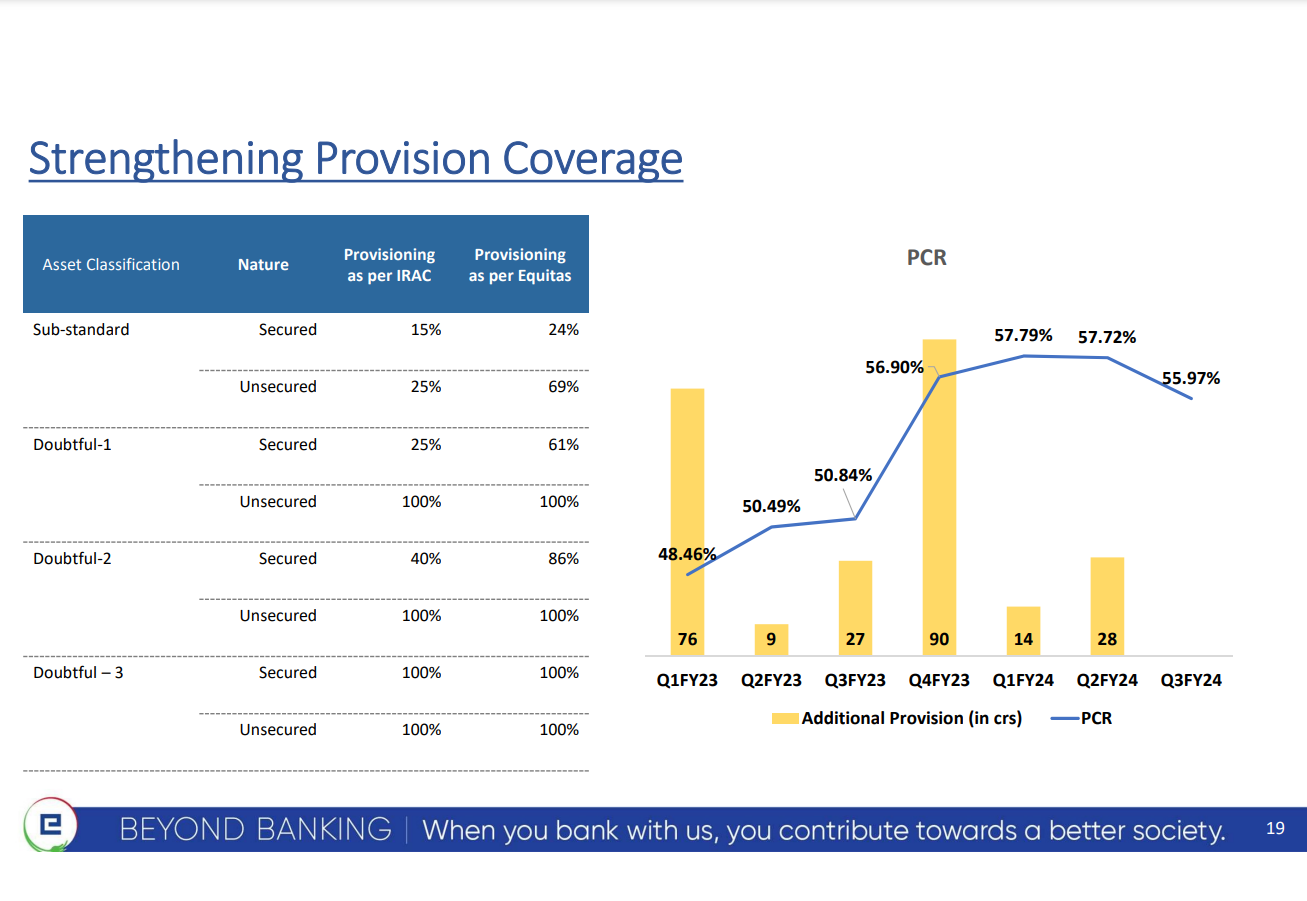

The provision coverage ratio(PCR) remains at 55.97% .(HIGHER THE BETTER)

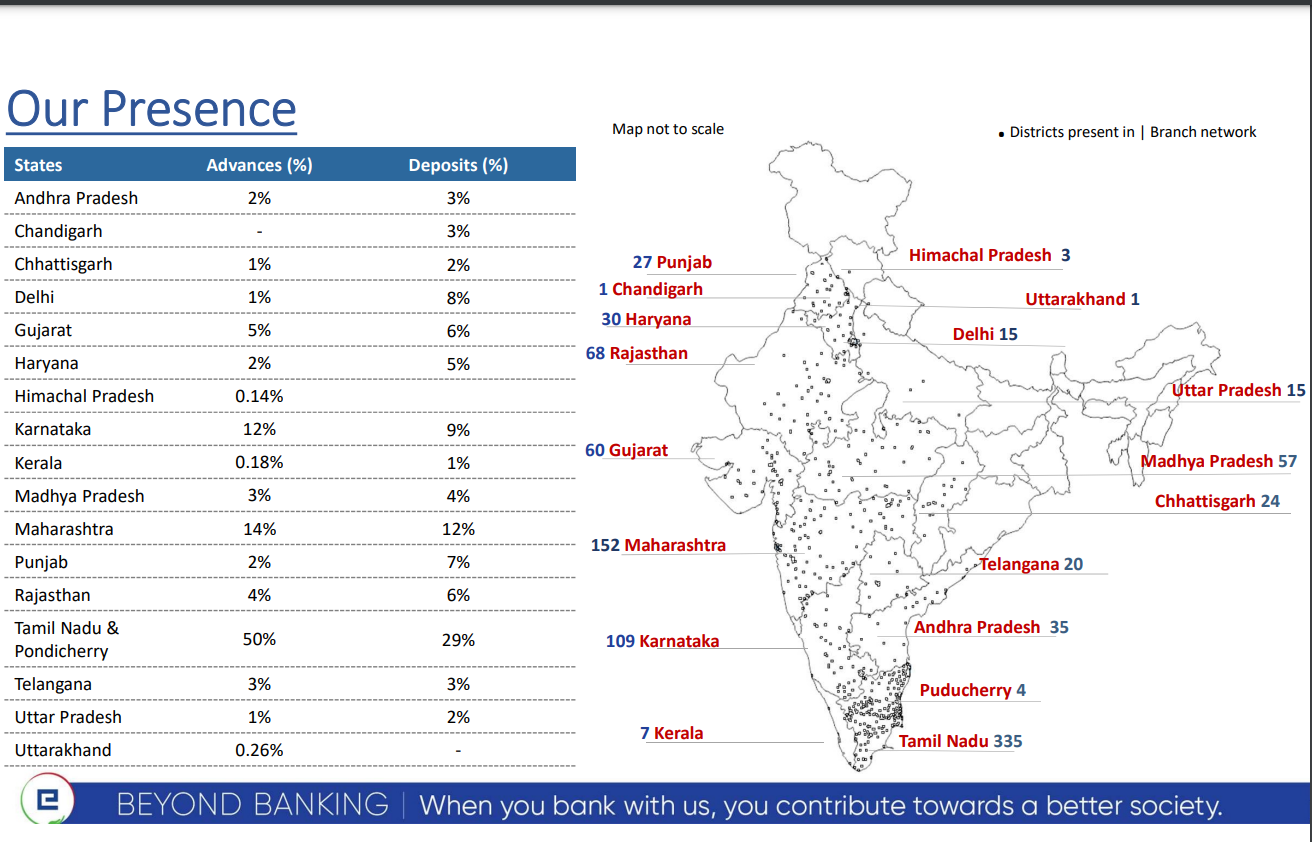

As of December 22, the composition of disbursements of TN and non-TN were 65% and 35%, whereas as of last month at December end, TN disbursement had come down to 54% and non-TN disbursements have gone up by 46%. Ex-bucket collection efficiency continues to be at 99.5%.(Risk- High concentration in Tamil Nadu).

Screenshot 2024-02-05 120902.png 348.99 KB

Screenshot 2024-02-05 121157.png 375.19 KB

Screenshot 2024-02-05 121253.png 202.41 KB

Screenshot 2024-02-05 121919.png 204.13 KB

The business seen steady growth in the states of AP, CG, Karnataka, and Maharashtra in the non-TN states. The new LoS has been rolled out and is now active in 182 branches across the country. Another 200 branches will go live this quarter

So our continued focus on retail is helping us to penetrate us into investor segment as well as trader segment, so coupled with the fact that you see mutual fund AUM is showing a trajectory growth of 36%, couple of effects, our brokerage account, which we have a 3-in-1 tie-up, is showing very good traction of again a growth of 25%, 26% and, most importantly, ASBA helping us to actually retain SA balances. So expansion from saver to an investor to trader is significantly helping us.

Yes. As we keep saying that we lend to the under-banked or the bottom of the pyramid. So we don’t find much difficulty in increasing the rate. But we also have to keep in mind that there has to be a threshold that there has to be also there. Affordability has to be borne in mind. That is one thing that we have to keep in mind while increasing the rate.

| Subscribe To Our Free Newsletter |