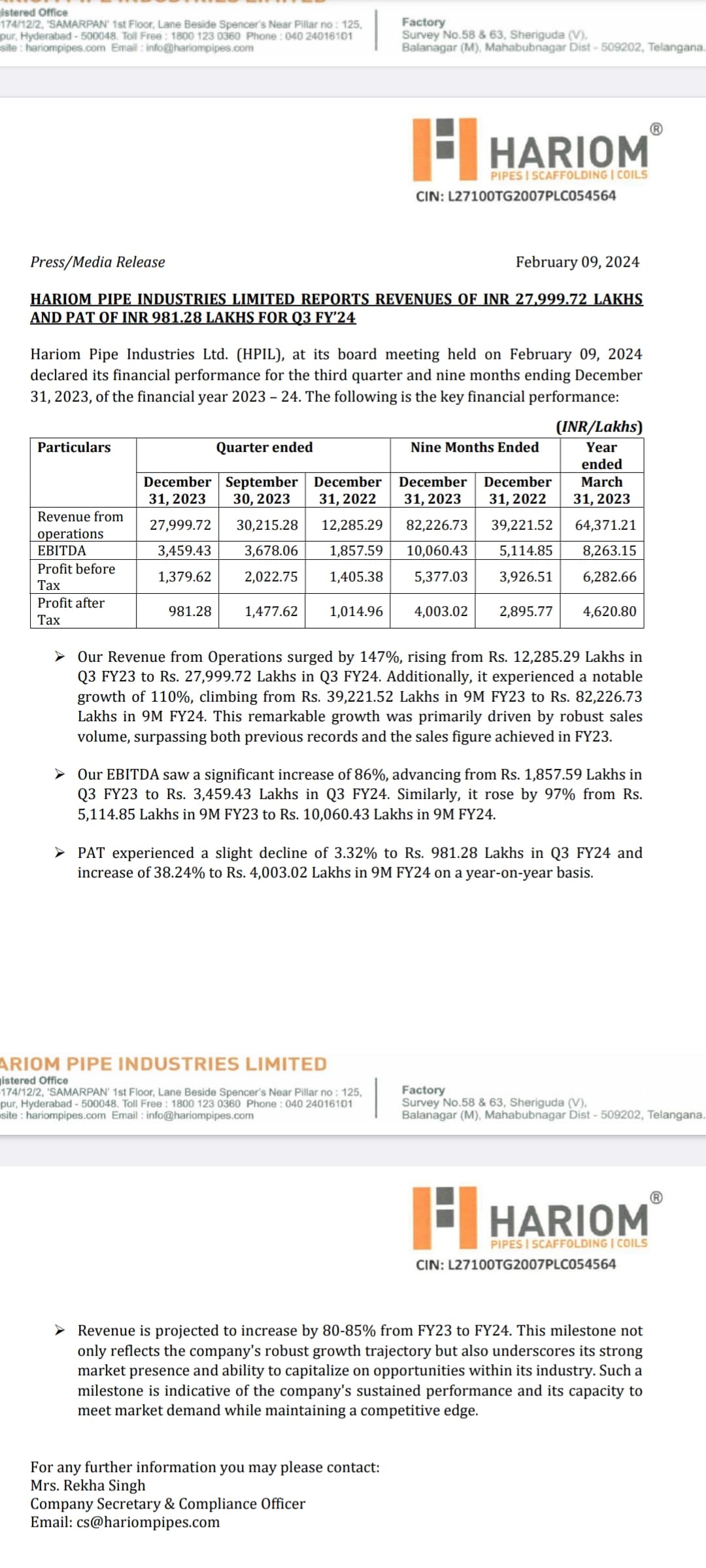

Hariom Pipe Results update:

-Revenue growth of 146% n QoQ fall

-EBITDA growth of 86% n QoQ fall

-PAT fallen QoQ n YoY led by dep & int exp

-Lack of disclosure in press release, what I believe industry weak demand + South flood had led the impact on operations

-Management released a simple press release compared to the last one which was detailed…

-Poor results were already backed in price as suggested by fall of 20% from ATH

-Behind the words guidance is given of 80-85% growth in FY24 over FY23

Q4E Sales: 360-375 cr

Q4E PAT: 15-17 cr

-Warrants money allotted can take care of Q4 WC requirements

-CF needs to be improved to have some impact on PAT & Free cash flows… if not happens then growth guidance (2500 cr revenue Target in FY26) will turn out to be a hindsight

-My honest review

No Reco

Disc: Invested

| Subscribe To Our Free Newsletter |