Cross posting from another thread:-

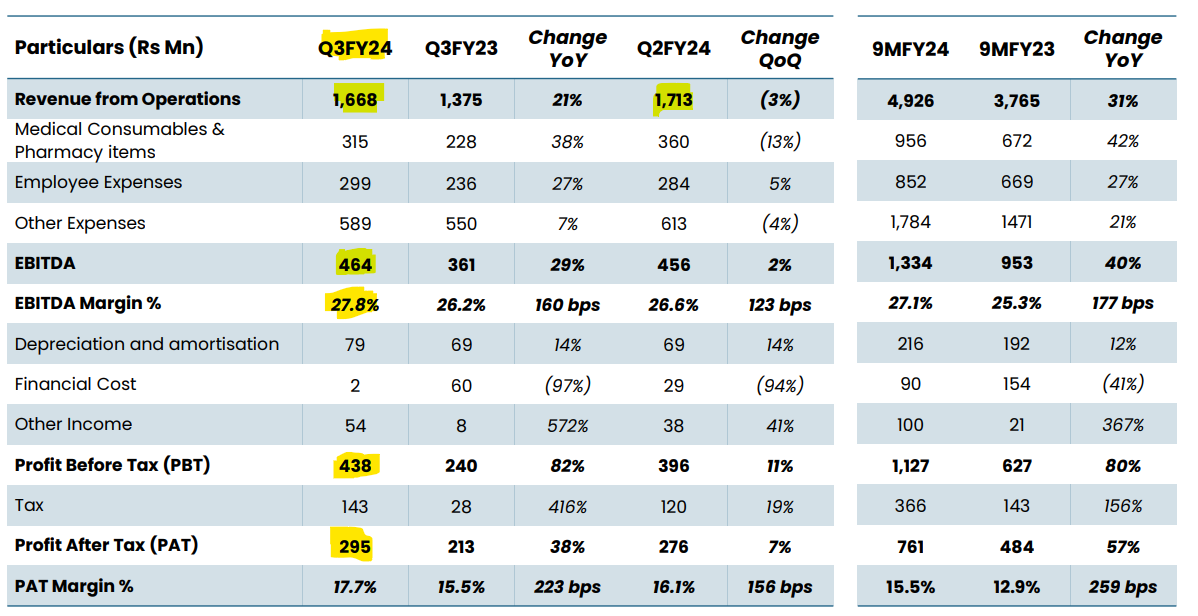

Yatharth Hospitals posted its results yesterday:-

Can someone help explain to me if Q3 has any sort of seasonality? I don’t see a reason for QoQ degrowth otherwise.

Anyways, posting few of my observations:-

- Noida extension is emerging as a super speciality hub with robotic surgeries starting in Q3FY24 and Oncology treatment starting in Q4FY24. One can see the effect in ARPOBs, which is substantially higher (at 34k) vs the next best in Yatharth i.e. Noida hospital at 30k

To build on this further, the Noida extension occupancy is currently at 45% and the company is undergoing a brownfield expansion to add 250 beds to take total hospital capacity at 700.

Imo, this is a very favorable upside trigger for the ARPOBs and for overall ROCEs.

-

Greater Noida hospital also registers a 10% ARPOB increase (possibly driven by transplants?). Despite lower footfalls, the overall revenue of the hospital is up by nearly 20%. This indicates the growing mix of higher specialities. Occupancy levels remain at around 70% and the company is undergoing another brownfield expansion of 200 beds.

-

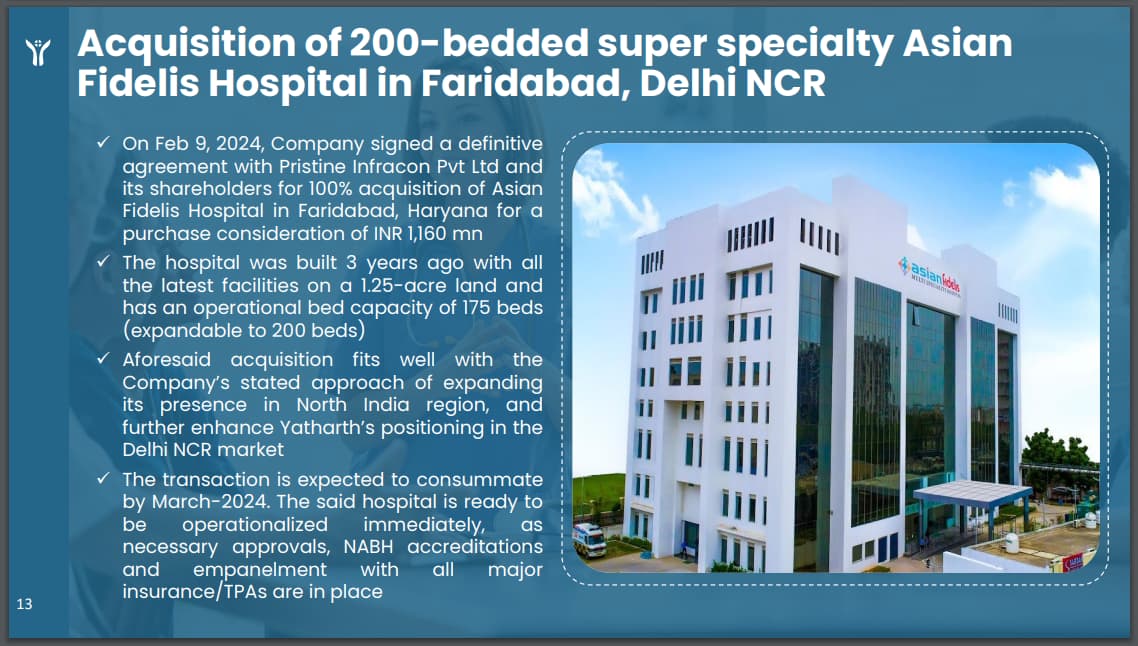

Acquisition of Asian Fidelis for 116crs cash. Sector-88 is a fairly populated area in Faridabad and with upcoming infra (connectivity from Jewar Airport in next 1-2 years), Faridabad will naturally have higher residence density. Needs to be seen how Yatharth can scale the metrics in this hospital. Prima facie, the acquisition looks fairly cheap.

Zooming out, Yatharth is adding nearly 250+200+175 = 625 beds, taking total bed capacity to >2k in next 1-2 years. This is a near 40% capacity addition.

- Valuations, I estimate FY24 EBITDA to be at around ~180 crs and with current acquisition, the net cash comes out to be around 180 crs. So EV is 3600 crs or lower if cash accruals in 9MFY24 are somewhat healthy. Assuming 3600crs though, current EV / EBITDA is 20x. Peers trade at much higher valuation:-

However, the peers in NCR region trade at much higher valuation. Part of the higher valuation is justified because Apollo, Max, Medanta, Fortis all are well recognised and much older brands with greater surgical prowess.

Hard to estimate the EBITDA growth for next year, but conservatively I expect EBITDA to register 40% increase primarily due to:-

a) Contribution from Asian Fidelis (around 20crs total).

b) Higher ARPOBs across hospital (barring Noida). I expect ARPOBs to inch up by 10-15%

FY25E EBITDA: 252

Expected net cash surplus: ~ 300 crs

Basis the above, Yatharth is currently trading at ~14x FY25E EV/EBITDA.

D – Invested (from lower levels) & biased

| Subscribe To Our Free Newsletter |