As per the last BalanceSheet published in Sept23, Cash Equivalent was 234Cr; whereas short and long term borrowings were ‘Zero’. Am not able to understand what is accounting for this Interest cost?

The inventories at 496Cr!! Almost 96Cr rise in last 3 quarters!!

More than 2 quarters of sales is tied up in inventory…

If its raw cotton inventory, why do they speculate and buy so much in advance… Does it show that they are not able to pass down the increased raw material cost and hence consider hoarding cheap raw material as their real moat…

What if the cycle does not turn soon and they are forced to liquidate at the low point of the cycle after holding for long? Why cant they hedge through commodity exchanges. Currently they are not doing the same, check point 6 below from their last annual report.

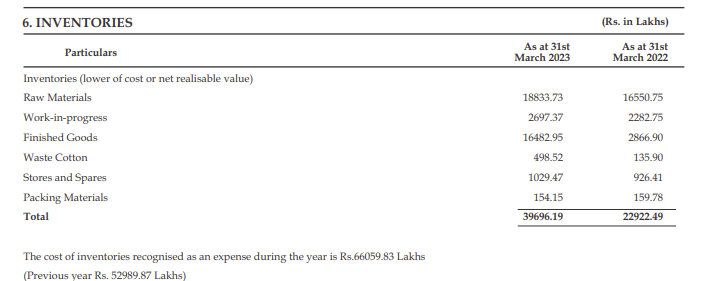

I was hoping that finished goods would be a small miniscule portion of this inventory, since that would loose value as the fashion fades in future. however the below disclosures in their last annual report (Mar23 data) are a little worrying. Raw Material had increased slightly from 165Cr to 188Cr, however Finished Goods had increased from less than 29Cr to 165Cr. (as per last annual report). Only hope can be that the FG is majorly in yarm form rather than knitted as mentioned by @sunilkumarca3101 above

But pls note that Knitted Fabrics is more than 22% of Revenue while Yarn is 64%; so inventory can be in similar ratio…

Disclosure: Holding since i consider it cheap, however now worried that it maybe cheap given this reason of growing inventory over multiple quarters…

| Subscribe To Our Free Newsletter |