Hi @Anubhav_Garg , thanks for writing in.

I am not aware of the guidance given by the company.

On cyclicality: I think underlying industry is cyclical. However, company has not shrunk substantially on margins or revenues in the last 7 years (barring covid years). Mainly driven by introduction of new products (metal sheet, die casting), higher content value per vehicle (manual locks to smart locks) and ram-up of subsidiary operations (capex fruition).

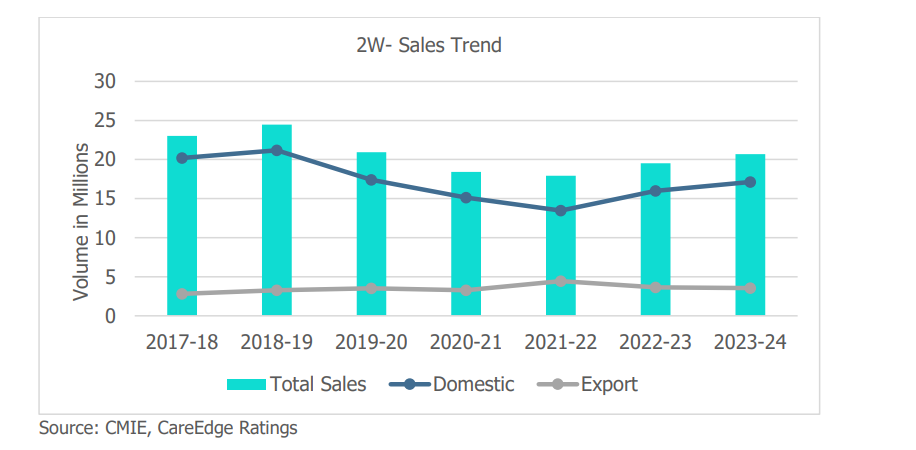

2 Wheeler sales has been largely flat over the past 3 to 5 years. However, company has grown its sales in 20-25% range for the past two full fiscals and current 9M.

Source: https://www.careratings.com/uploads/newsfiles/1685956360_Two%20Wheeler%20FY24%20Outlook_CareEdge.pdf

Disclosure: own it and added more in last 30 days.

Disclaimer: I am not a financial advisor and nor a SEBI registered Analyst. The content shared here is only for learning purpose. All the names mentioned here are for example purpose. I may buy more, exit or partly sell the stock/bonds without any prior intimation.

| Subscribe To Our Free Newsletter |