For any QSR, there are fixed costs at the corporate level (rent, office salaries, sales & promotions, app development) as well as other initial costs that do not rise linearly with rise in revenues (initial training costs, new equipment, one time fee for opening up new store, etc). Hence, operating leverage should play out after a certain scale has been reached. Jubilant Foodworks is a good example of that in India. Dominos India EBIDTA grew much faster than their revenue growth in the past decade. The overall numbers are skewed because of their investments in Sri Lanka and in Dunkin Donuts.

You can look at Burger King itself. In the latest quarter, a 20% increase in revenues has resulted in a 34% increase in Restaurant level EBIDTA and a 48% increase in overall EBIDTA. You can see that Corporate and General expenses have reduced from 6.3% of sales in Q3 FY23 to 5.4% of sales in Q3 FY24 as Sales have increased. This is operating leverage at play.

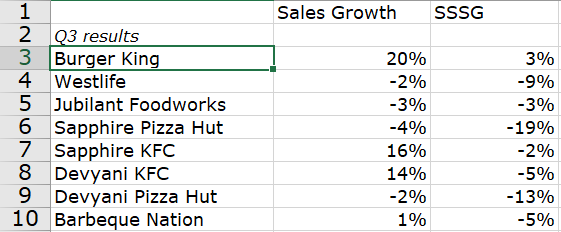

@iyeron I don’t think I agree with your hypothesis. McDonalds is definitely a stronger brand but I don’t think selling cheaper products is the only way to take market share. There are multiple factors which determine where people go to eat and price is just one of them. Product quality, Variety of products, ambience, location, marketing, deals and promotions, brand loyalty, etc are some of the other factors that also influence decision making. If it was so easy for McDonalds to take away BKs market share, why do the numbers indicate otherwise so far? BK has grown from 0 to almost 1600 cr (FY24) of sales in less than a decade. Even in the latest quarter, BK has shown positive SSSG as opposed to negative growth shown by Westlife.

Q3 update –

Q3 numbers look great for RBA. They grew the highest out of all the QSR players, with the only one to achieve positive same store sales growth. McDonalds, on all fronts has underperformed when compared to BK. The Pizza brands are really struggling, with KFC showing good positive growth. For the kind of growth most QSR players have shown, they trade at really absurd valuations.

RBA has a much smaller base, trades at lower valuations and has significantly much larger headroom for growth (they have pan India rights). I am optimistic about its growth prospects in India. Their Indonesia business did see a slight slowdown, but considering it is a new market for them we can give the management some time to show execution. Indonesia will need to be monitored closely to make sense of the prospects there.

| Subscribe To Our Free Newsletter |