Hi Thanveer,

Pls read the above thread carefully. If I were to summarize, Lactose India is largely a 3 part story (as of now)…

1) Significant capex for Kerry for Lactose (from 3500tpa to 11000tpa)..Demand is quite clear here as Kerry intends to put up even more capacity but Lactose India wants to stabilise the existing capex first.

2) Contract Manufacturer for Sanofi…small but stable cashflow business.

3) Lactulose capacity of 2400MT/Annum. Lactose India has done 30cr capex for putting up Lactulose. This is better margin business as it is 3rd derivation of Lactose. This business is very interesting (pls try reading up more on this). Impact of Lactulose will largely come in FY17/FY18. Current numbers are largely reflection of stabilization of Lactose for Kerry.

According to me…1&3 points are big game changer for the company. (Pls refer above thread for more)

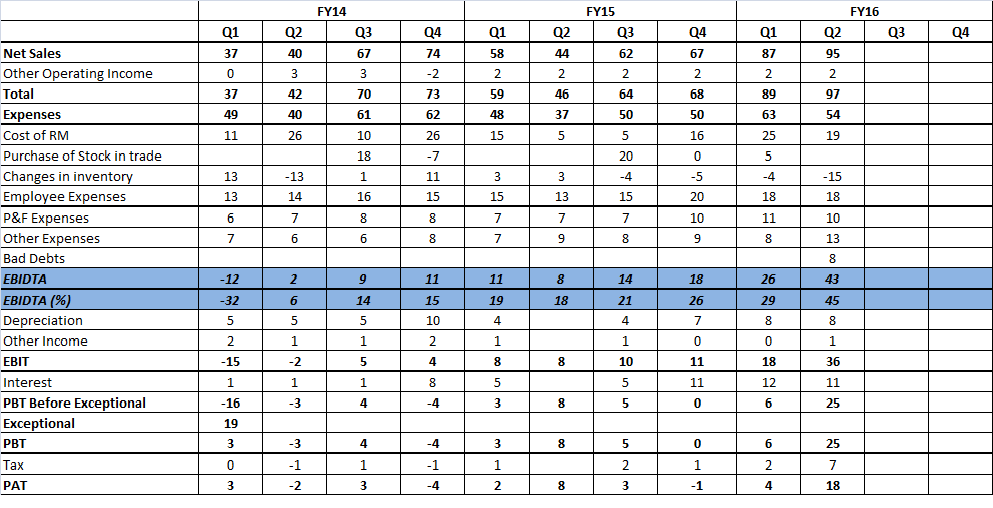

Yesterday’s quarterly numbers were excellent and showing where company is headed.

1) Margins continue to expand very smartly (EBIDTA Margins at 45% compared to 29% in previous quarter and 18% same quarter last year). This is big improvement. Even after adjusting for inventory gains & bad debts. Margins are 37% odd.

2) I believe lactose will be very high ROE, ROCE story. Company’s networth stands at Rs 19cr and if i were to annualise quarterly PAT…ROE can be as high as 38-40%. This is largely because of client funding the capex

3) Reduction in Long Term Debt by Rs 3cr was another pleasant surprise. LT now stands at Rs 26cr and ST at Rs 3.7cr.

Lactose India is a very unique play on Lactose/Lactulose with company at inflection point. Delta in numbers should continue to be big and provides extremely lucrative risk/reward. Potential upside can be really big.

Disc – Invested.

Hope that helps.

Thanks.

| Subscribe To Our Free Newsletter |