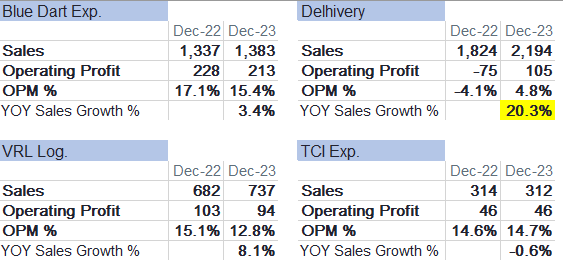

Q3FY24 results of all peers:

Key personal takeaways from Q3FY24 Conf Call [rephrased]:

• Expect growth rates of 15~20% for eCom and 30% for PTL segments in FY25.

• Factors that will help to grow: Service quality, reach of the network, and cost leadership.

• Focus area: Gain heavy volume. In turn, source PTL loads from across the country. Seeded salesforce in 80 cities. Will back them with enhanced marketing spend.

• Incremental gross margins continue at 50% and shall continue in the coming quarters. In the long run, it might settle at 30% – basis 12 yrs. of own historical data. In the very long run, the stable transportation margin [OPM, I think so] shall be at 16~18% plus some delta due to better network engineering.

• OS1 based DispatchOne [SaaS] offering is expected to be monetized from Q1FY25.

Overall:

As of now, the software driven logistics ecosystem of delhivery provides incremental gross margins at 50%. In future, industry players intend to pass general price increase [from inflation] to their customers whereas Delhivery would maintain the same prices, benefitting from its network efficiency. Competitors can replicate Delhivery cost structure and network efficiency only if they invest in the automation of all the core areas and fine tune their systems after spending similar amounts of time.

Disc: Have a position.

| Subscribe To Our Free Newsletter |