Hi @banjobaj,

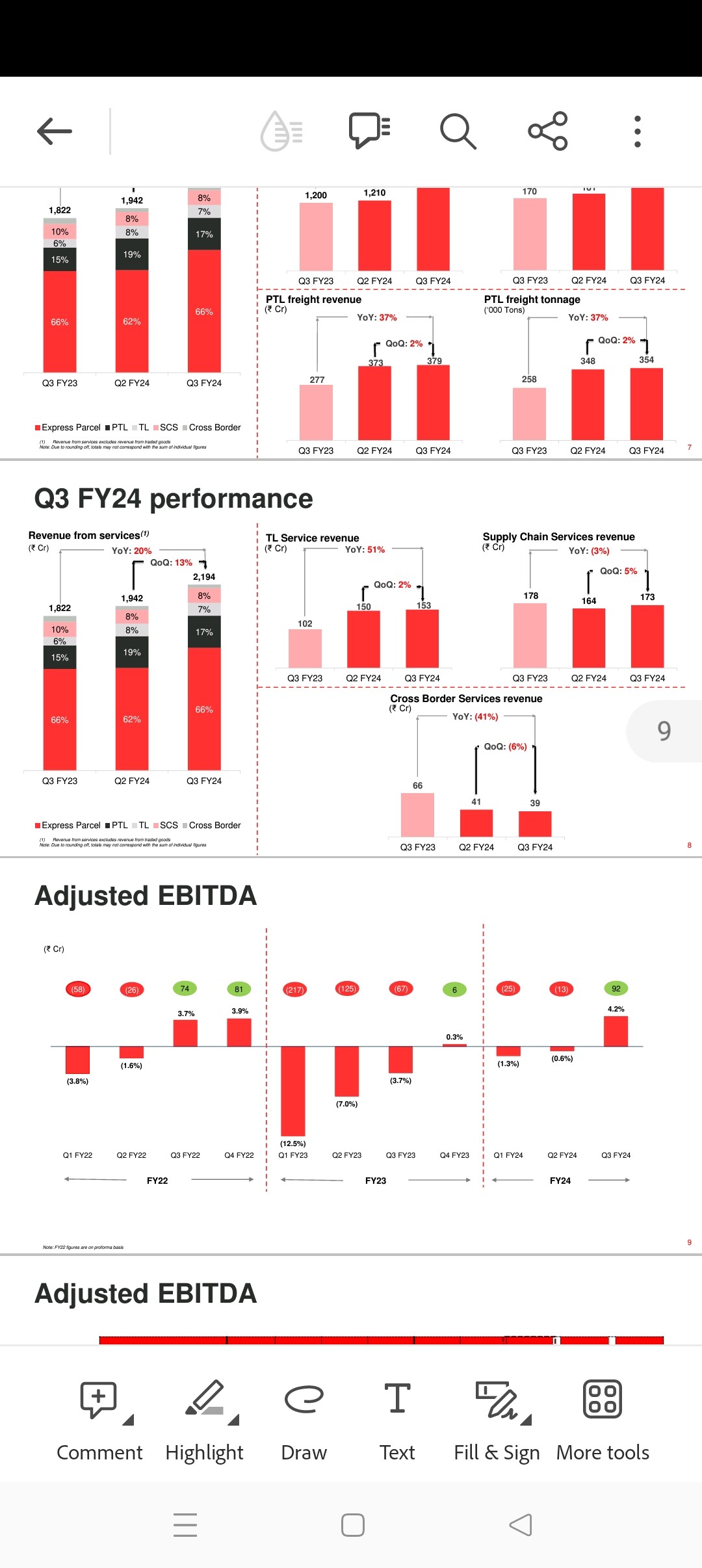

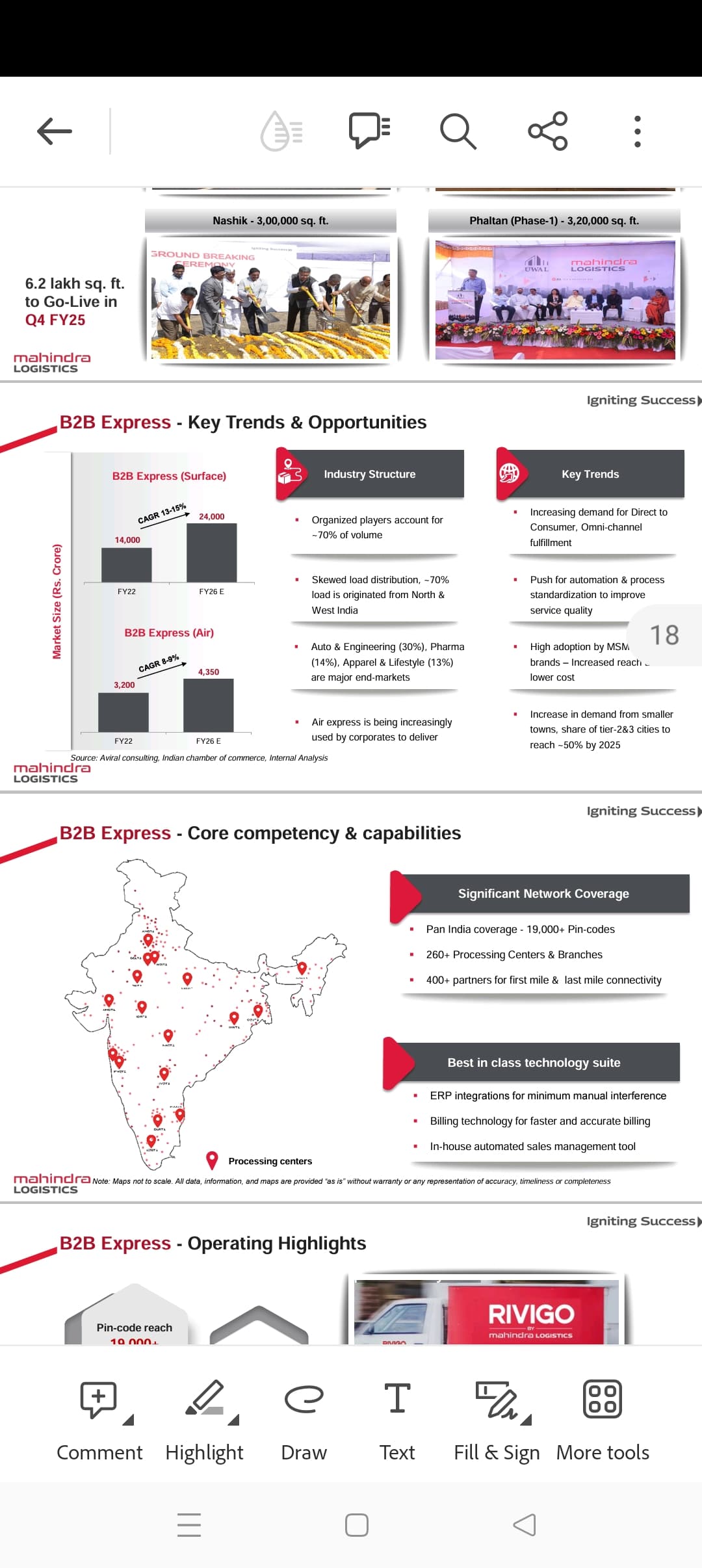

Delhivery’s part truckload (PTL) segment is the one into B-B express which has grown from 273 cr to 373 cr y-y in their q3 this year which is 17% of their revenue. (Check the screenshot-1 from their q3 presentation)Mahindra logistics also has B-B express (from Rivgo ). Both of them have aggressive expansion plans like our TCI express capex plan of 500 crores for fy-23 to 28. Please check this delhivery interview in CNBC for quick reference.https://youtu.be/MKDFzktOLP8?si=xNMAuyFl_oqZ58Nt

Delhivery is putting in 7% of their revenue as capex until Fy27 and 4% later on, with focus in PTL segment as that is the bigger opportunity. I am attaching here yearly growth guidance in Mahindra for their B-B express for your reference.

Overall PTL B-B express works like a niche space where service differentiation like delivery speed etc let the players enjoy a premium. Service offerings mix also varies among different players.New service offerings such as rail express, pharma cold chain express in TCI express is expected to grow faster. Business models also varies like PTL in Delhivery doesnt follow traditional hub and spoke, bit something different called Mesh. TCI is the most asset light one in my understanding as they dont own trucks. Competition is expected to intensify with aggressive capex plans to grab market share from unorganized and many of the peers will enjoy economies of scale and operational efficiency etc in coming years.The main worry for me is as with TCI express ‘s adamant stance on not giving away a bit of margin, will they be left far behind.?Delihivery reporting their first PAT was a surprise for me last quarter.

Those with deeper industry knowledge can comment better in comparing competitive advantages and who could potentially gain the most in coming years.

| Subscribe To Our Free Newsletter |