Q3FY24 Concall notes –

- Guidance – FY25 EBITDA to be 1450-1700 Cr

- Guidance is built on 30-40% contractual business from 2 contracts and rest is quarterly contracts that customers buy on. Aarti is building guidance through projections basis the volumes customers are projecting.

- Sequential improvement of EBITDA by 15%, even though margins were 100 bps lower. Sequential revenue increase was 18%

- Going forward, management expects gross profit to increase on back of increased volumes and increased realisation per kg. This should mostly trickle to EBITDA as opex remains subdued

- We are observing a rebound in demand for various products catering to the discretionary applications such as dyes, pigments, additives, polymers and more. Agrochemicals and pharmaceuticals is still soft as customers want to carry lean inventory due to muted demand. In agrochemical, demand is more molecule specific

- Contracts –

- Entered into new contract with ag-chem major for some herbicide intermediate. The contract value is 3000 Cr over 9 years. EBITDA margins of 20% expected on stable RM prices in this contract. This product is already part of Aarti’s portfolio. 300 Cr in FY25 and 350 Cr FY26 onwards expected here. 200 Cr would happen in FY24

- Secured 6000 Cr contract over 4 years for niche specialty chemical. Margins here would be 15-17%. This product is being supplied already and this is an incremental contract but due to new demand areas of this chemical, volumes would be higher now. Linear 1500 Cr in each year expected. This product would contribute 900 Cr to sales in FY24

- Key thing about contracts –

- Margin projections are on current stable RM prices. If RM prices rise the margin in contract 2 could be even 12% and if it falls it could even be 20%+. Margins are fixed on per KG basis

- No incremental capex is required for these

- Some pricing improvements are taking place as demand is improving

- While its hard to pinpoint geography level demand as products sold to some customer might get used in some other geography but in general US recovery is better than others

- Tax rate in FY25 will be 15-17%

- Ethylation capex is for agrochemical while Nitro-Toluene is for wider product profile

- Chloro-toluene capex will commercialize in FY26 and substantial EBITDA would be added in FY27. These are import substitute products. This capex would have 1.2 asset turn (1500 Cr capex size) translates to 1800 Cr revenue. EBITDA would be 25-30% in this product range

- Red sea crisis has raised container costs and it will take month or quarter lag to push the prices up.

- NCB capacity ramp up will happen from 80 KT to 108 KT

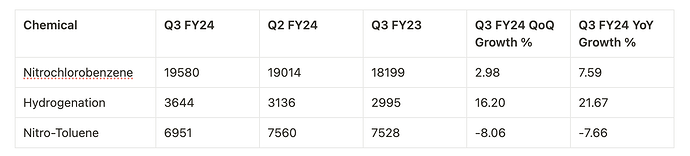

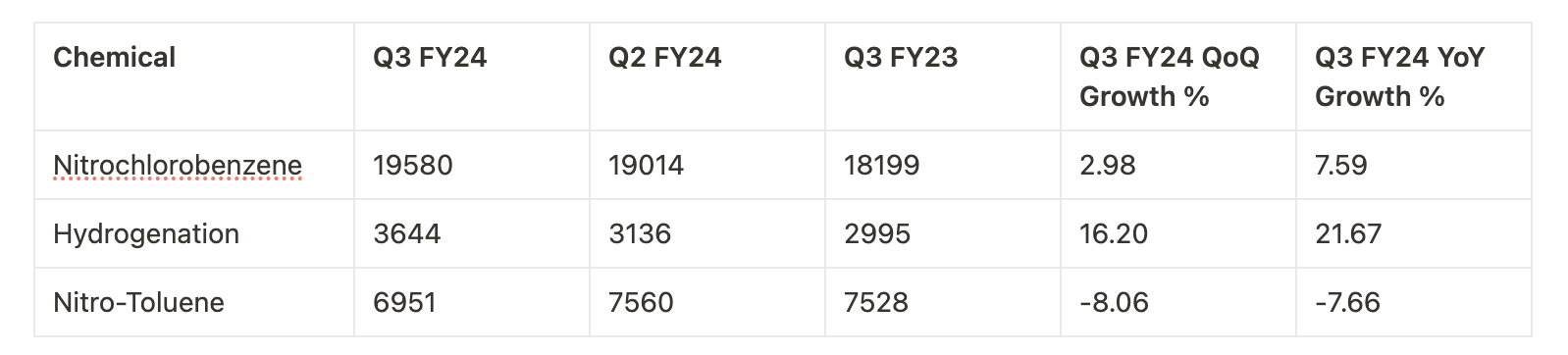

- Volume numbers –

| Subscribe To Our Free Newsletter |