Was able to look up some info for the two competitors that they spoke about during Q3 concall.

Raychecm RPG (website):

-

Incorporated in 1984 as a JV between Raychem Corporation, USA, and RPG Group. Raychem Corporation was then acquired by TE Connectivity Limited (formerly Tyco Electronics Ltd) in 1999. Currently, both TE Group (promoter holding entity of TE group – Raychem International Manufacturing LLC) and RPG are equal shareholders in the company. The Board of Directors of the company consist of members from both, TE group and RPG group.

-

TE Connectivity Limited (website) is a technology leader which designs and manufactures electronic connectors, components, and systems. TE’s contribution is in the form of technology, global practices, and customer insights, whereas RPG supports in the form of management of various compliances, local support.

-

In FY23, around 22% of net sales were derived from the TE Group.

-

Raychecm RPG’s business is distributed into four segments:

- energy products – 54% of revenue

- Transformers division at 24% of revenue

- engineering business unit (EBU) at 17% of revenue

- oil & gas at 5% of revenue

-

In FY23, around 61% was contributed through domestic sales and remaining 39% through exports.

-

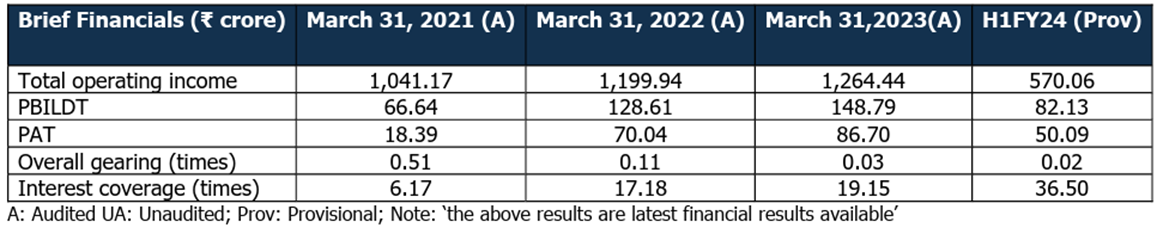

Financials: Top line of Rs 1260 Crs (across all divisions, Transformer revenue must be 300 Crs) Revenue growth of 5.34% Y-o-Y in FY23. EBITDA of 11.77%

-

H1FY24 witnessed a substantial PBILDT margin rise to 14.23% from 11.53% in H1FY23 as a result of selective acceptance of orders having high margins in the transformers business which is expected to continue at similar levels going ahead.

-

High credit period of around 6 months for few clients, though the average collection period remains comfortable at around 77 days in FY23.

-

A promising order book of ₹729 crore for the next 6 months.

-

Cash and cash balance of the company stood at ₹121 crore

Danish Pvt Ltd (website). Active Linkedin page (link)

-

Incorporated in 1985, DPL manufactures and exports transformers for power distribution and transmissions. The company started with manufacturing of LT Panels & Battery Chargers and gradually diversified into Control Relay Panels followed by Transformers.

-

Within Transformer division, have three broad segments:

- Oil Immersed; Manufactured with prime CRGO using step-lap design for low losses along with availability of Hydraulic Core Lifting Facility. Ratings: 3 phase upto 66 kV 50 MVA & 1 phase upto 33 kV 333 kV.

- Dry Type: 3 phase upto 33 kV 10,000 kVA.

- Special Type: Primarily used for Solar / Wind Power Generation. Typical range from 1 MVA to 20 MVA. Upto 6.3 MVA (2×3.15 MVA Transformers).

-

Annual plant rolling out capacity of 2400 MVA, ensuring timely delivery.

-

In- House NABL accredited test laboratory as per IS:2026 & IEC:60076.

-

The revenue growth CAGR of 23% during past three fiscals through Fiscal 23. In fiscal23, company had already clocked in turnover of Rs. 188crores, as against Rs 148 crore during FY22.

-

Further, the revenue visibility over the medium term stands strong backed byRs 130 crore of order book outstanding as of May-23 and ramp of operation in new unit started from Dec’22 will further add to support the revenue profile over medium term.

Plotting Shilchar performance while keeping the competitor info at the background, revenue acceleration, margin health, export mix, working capital intensity etc. are still remarkably distinct (in favour of Shilchar). Raychem looks to be promising from tech-know how and parent capabilities perspective. Also, transformer division is approx. same size that of Shilchar (~300 Crs ish revenue). Raychem at enterprise level has 40% export mix. On margin front, both Raychem and Danish are at mid single digit PAT margins.

Personally, there is more to the story than meets the eye. On export side they are just killing it (as of today) with projection to continue maintaining the margins and growth rate. Looking at size of first presentation and cut-the chase approach during maiden concall, it appears that they are not too interested to tom-tom about good things that may be happening behind the scene.

Thanks,

Tarun

Disc: Invested

| Subscribe To Our Free Newsletter |