Valuation Note 3 [21st February 2024]

Current Valuations can only be judged from the vantage points of How the future turns out.

If 1 year Down the line PAT growth is 30% or higher, and there is visibility for Robust Orders even beyond that, Current Valuations are approx ~ 20X P/E

If 1 year Down the line PAT Growth is 30% or higher BUT the order book starts to dwindle, the stock will be punished. Fast & Hard.

Therefore, What is cheap or expensive is based on our understanding of the future.

The question then becomes: How confident are we that Order book will remain Robust?

Firstly, Tender Pipeline for Wind/Hybrid projects & Awarded Capacity give us confidence that this most likely will be the case (Thanks to @rcinvestor999 for updating us on the same)

Secondly, the Management Commentary is bullish (Disclaimer: Management has a strong incentive to paint a rosy picture, so this is not always the most reliable Signal)

Given a 75% Market Share in Wind Energy Sector, plus a high % of Cranes with 100 MT and above capacity (most suited for higher Hub heights), Sanghvi is well placed to milk this Wind Energy boom.

The second question then becomes: If Demand is well taken care of for the foreseeable future, what can limit Sanghvi’s Growth?

My 2 cents : Its own capacity.

Even after spending ~400 Cr this year, Sanghvi has an Soft upper limit of ~154 Cr per Quarter of Sales or 615 Cr per year.

In FY24, Its already hitting that number (Q4FY24 Sales should be ~155 Cr),

If despite a huge capex of 400 Cr in FY24, Sales have a limit of ~154 per Quarter, where’s the 30% Growth going to come from?

- Rental Yields will need to increase

- More investments in buying Cranes

| Rental Yield (%) | 2.3% | 2.5% |

|---|---|---|

| Sales (Cr) | 646 | 702 |

**Assuming Current Gross Block of 2600 with 90% Max utilisation. Sales = 0.9*Gross Block Rental Yield

If Rental yield increases to 2.5%, Sanghvi can eke out as much as ~700 Cr. Nearly 80 cr more.

So, the same Crane Capacity can accommodate at least up to ~11% Sales Growth without spending more on increasing crane capacity (i.e – buying more cranes)

But there’s the kicker, an increase in Rental Yields to 2.5% goes straight to the bottom line.

This 80 Cr, on a post-tax (25%) basis, has the potential to increase PAT from 180 to 240 Cr.

A 30% PAT Growth.

Although the probability of Sanghvi being able to hit a Rental yield of ~2.5% should be viewed with a healthy Skepticism, it is NOT entirely outside the realm of possibility.

Either way, in my view there are 3 Growth Drivers :

- Robust Order book

- Rental Yields increasing

- A Sizeable Capex Program to Increase Capacity

Personally, given my understanding as of today I am least worried about point 1. The Demand for once does not seem to be a problem. Capacity might be.

My Guesstimate is that a combination of Rental Yields and Capex is likely to drive growth.

An announcement of a sizeable capex program in the near future should be an important trigger because it would be akin to “putting your money where your mouth is”

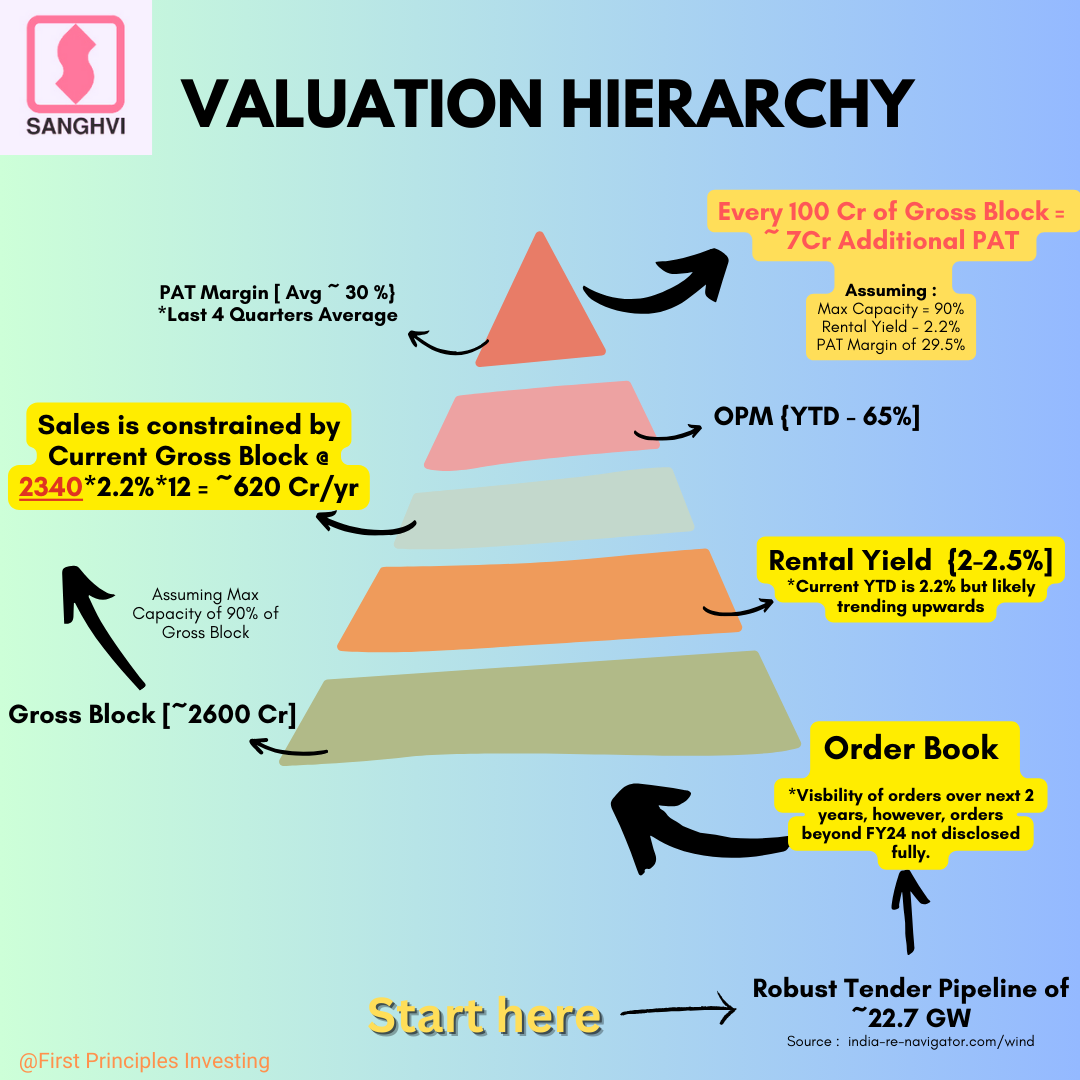

We’ve already got a sense of what Rental Yields can do for Sales and PAT, here’s a diagram that can help us understand the impact of Capacity on Sales and its limitations.

In short, Every 100 Cr spent on Capex can increase PAT by ~ 7 Cr. This means if the co’ spends another 400 Cr, PAT Growth is likely to be just about 15% (28/180 Cr)

Hardly inspiring.

This is why I believe, Rental Yields, Capex and Op. Lev Combined would be needed to hit a 30% or higher PAT growth, a minimum benchmark for us to conclude with confidence the Stock is Currently cheap or reasonably priced.

Look forward to hearing your views. Please Feel Free to point out any errors.

| Subscribe To Our Free Newsletter |