Valuation Note 3 – UPDATED [22nd February 2024]

Current Valuations can only be judged from the vantage points of How the future turns out.

If 1 year Down the line PAT growth is 30% or higher, and there is visibility for Robust Orders even beyond that, Current Valuations are approx ~ 20X P/E

If 1 year Down the line PAT Growth is 30% or higher BUT the order book starts to dwindle, the stock will be punished. Fast & Hard.

Therefore, What is cheap or expensive is based on our understanding of the future.

The question then becomes: How confident are we that Order book will remain Robust?

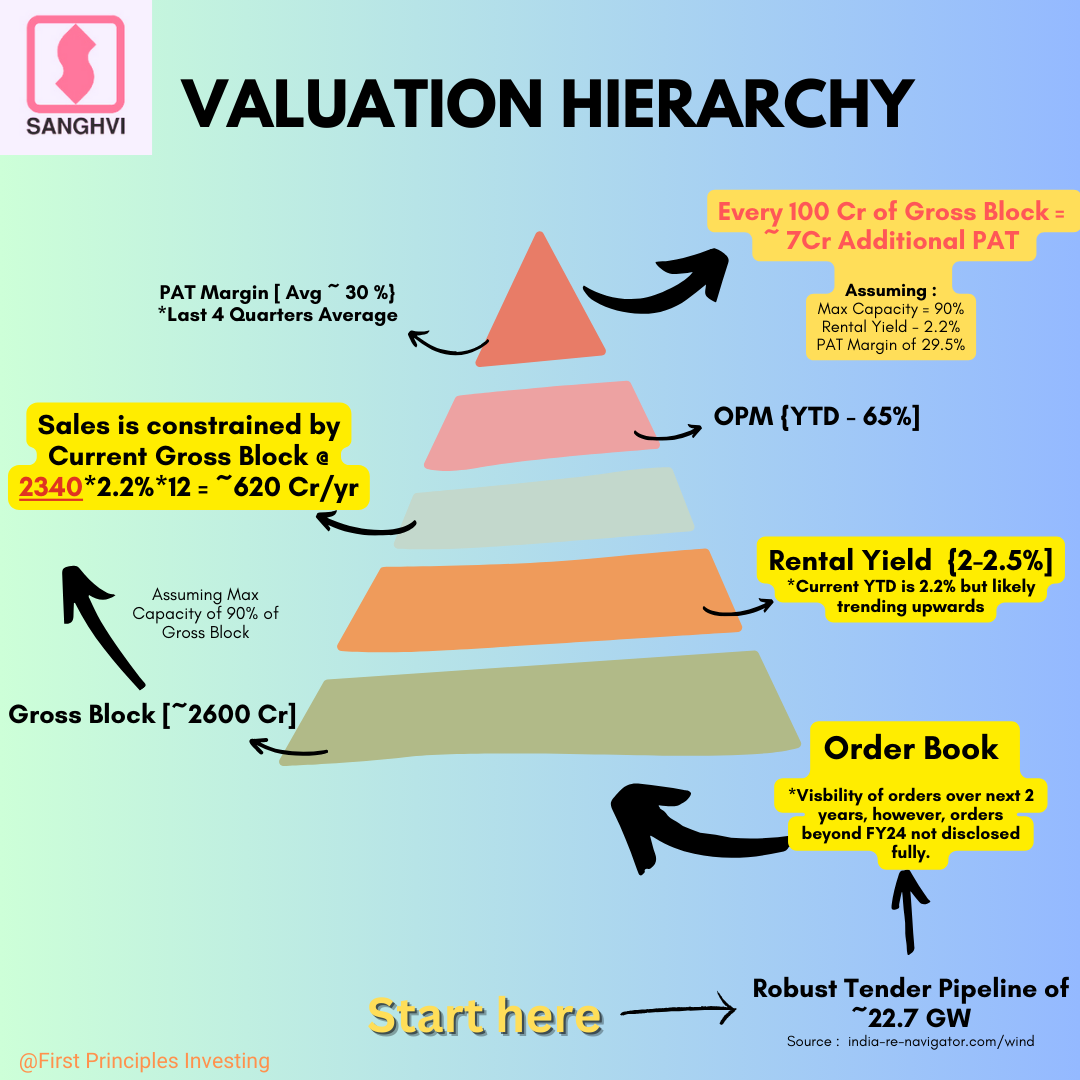

Firstly, Tender Pipeline for Wind/Hybrid projects & Awarded Capacity give us confidence that this most likely will be the case (Thanks to @rcinvestor999 for regularly updating us on the same)

Secondly, the Management Commentary is bullish (Disclaimer: Management has a strong incentive to paint a rosy picture, so this is not always the most reliable Signal)

Given a 75% Market Share in Wind Energy Sector, plus a high % of Cranes with 100 MT and above capacity (most suited for higher Hub heights), Sanghvi is well placed to milk this Wind Energy boom.

The second question then becomes: If Demand is well taken care of for the foreseeable future, what can limit Sanghvi’s Growth?

My 2 cents : Its own capacity.

Even after spending ~400 Cr this year, Sanghvi has an Soft upper limit of ~154 Cr per Quarter of Sales or 615 Cr per year.

In FY24, Its already hitting that number (Q4FY24 Sales should be ~155 Cr),

If despite a huge capex of 400 Cr in FY24, Sales have a limit of ~154 per Quarter, where’s the 30% Growth going to come from?

- Rental Yields will need to increase

- More investments in buying Cranes

- EPC Business (Order book of 111 Cr to be executed by January 2026)

First Let’s Checkout Rental Yields :

| Rental Yield (%) | 2.3% | 2.5% |

|---|---|---|

| Sales (Cr) | 646 | 702 |

**Assuming Current Gross Block of 2600 with 90% Max utilisation. Sales = 0.9*Gross Block Rental Yield

If Rental yield increases to 2.5%, Sanghvi can eke out as much as ~700 Cr. Nearly 80 cr more.

So, the same Crane Capacity can accommodate at least up to ~11% Sales Growth without spending more on increasing crane capacity (i.e – buying more cranes)

But there’s the kicker, an increase in Rental Yields to 2.5% goes straight to the bottom line.

This 80 Cr, on a post-tax (25%) basis, has the potential to increase PAT from 180 to 240 Cr.

A 30% PAT Growth.

Although the probability of Sanghvi hitting a Rental yield of ~2.5% should be viewed with a healthy Skepticism, it is NOT entirely outside the realm of possibility.

The Second driver is capex.

From the Graphic below, we can see that Every 100 Cr spent on Capex can increase PAT by ~ 7 Cr assuming Rental Yields & Net Margins at 2.2% & 30% respectively.

This means if the co’ spends another 400 Cr, PAT Growth is likely to be just about 15% (28/180 Cr)

Hardly inspiring. If viewed in silos.

The 3rd Driver is is the outstanding EPC Order book of ~111 Cr to be executed ~ 71 cr in FY25 and remaining 40 Cr in FY26.

I have no clue what the PAT Margins for EPC book can look like (@rajdori, @Vaibhav_Temani – Any reliable sources?) but 25% PAT for EPC may seem a little too optimistic. I also have no clue as to the distribution of the EPC order book. Whether Co’ will recognise this 71 Cr equally per Quarter in FY25 or any other way.

A conservative 10-15% PAT Margin, would lead to a PAT of 7-11 Cr in FY25, which is a 4-7% Growth over FY24 full year PAT of ~180 Cr.

Bottomline is that there are 3 Growth Drivers, all of which rest on the foundation that Order book will NOT be an issue.

- Rental Yields increasing

- A Sizeable Capex Program to Increase Capacity

- EPC Book (111 Cr) & potentially Growing further.

If this basic premise fails for whatever reason, these 3 Key Drivers will be significantly weakened.

Growth (if) is likely to be a function of a combination of the 3, with Rental Yields being the most preferable (Increases ROE too) and Capex being the least preferable way to pursue growth.

In Conclusion, Current P/E of 28-29X are justifiable only if PAT Growth is strong. For me, a 30% growth in PAT is a minimum benchmark for valuations to make sense. Maybe for you its a different number.

Thanks again @aditya_kedia, @rajdori & @Vaibhav_Temani for your valuable inputs.

Look forward to hearing your views. Please Feel Free to point out any errors.

| Subscribe To Our Free Newsletter |