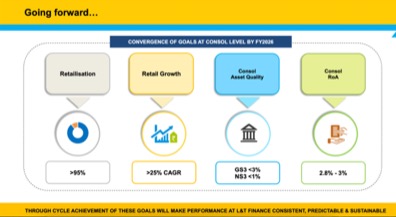

L&T FH delivered another great set of numbers this quarter, whilst Lakshya 2026 goals have been met 2 years in advance.

-

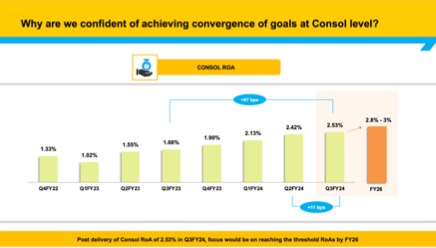

Consol ROA is now at 2.53% vs 1.66% Q3 last year, consol ROE is now 11.35%

-

Consol PAT is up 41% YOY at ~640 Cr for Q3

-

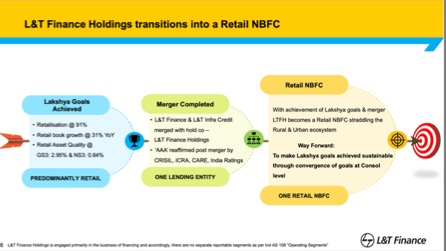

Merger is completed with L&T AMC sold off and L&T Infra and L&T Finance now merged into this company

-

Retail book grew at 31% YOY and is now > 90% of the business. I think this is now largely a retail NBFC and with only a small part of the wholesale book to sell post bringing it down so sharply, do not understand with these growth/ROA metrics why is it still valued at under 2 PB when the likes of Chola, FiveStar are trading much higher (>4 PB).

-

Even in pre covid times (Jan 2020) when things were terrible for NBFCs after 2018 and this was not a retail NBFC this has traded at 2x book. Whilst in great times in 2018 with the credit cycle, valuations were much higher than that as well when it traded at 5x book

-

Management has addressed doubts on personal loans/contracting NIMs well in the concall and have mentioned not much impact, but this remains to be seen in future results

-

CEO transition handled quite well and old/new CEO were both on the last concall with lots of positivity. Current CEO Mr Sudipta Roy is ex ICICI/Citi/Deutsche bank and ex CEO Mr Dubhashi superannuates from the company in April’24

-

Below snapshots from Q3 investor presentation sum up last years progress quite well

- Charts also look good in my opinion with clear respect for 50 DMA on the way up and comfortably having broken through a couple of key resistances and upward trendlines

Disclosure : I am invested in self and family accounts for the last 1 year odd and am biased. Have further buy transactions in family accounts in last 90 days. I am not a SEBI registered advisor and this is not investment advice.

| Subscribe To Our Free Newsletter |