Q3 FY24 Concall notes

-

Project Highlights:

- Completed 7 projects in Q3FY24, including Adani Realty’s residential and industrial warehousing for Reliance Jamnagar.

- Awarded 2 major projects: Kalamkhush Campus at Gandhi Ashram and Gujarat Biotechnology Research Centre.

-

Order Inflow and Bookings:

- Q3FY24 order inflow at Rs.1,060 crore; total Rs.1,995 crore post recent letter of acceptance.

- Outstanding order book at Rs.4,443 crore (51% government projects) as of 9MFY24.

-

Project Development Updates:

- Legal proceedings for Surat Diamond Bourse underway.

- UP Projects revenue: Rs.250 crore (Q3), Rs.1,429 crore (9MFY24).

- SMC administrative building progressing; Q3 revenue Rs.49 crore, 9MFY24 total revenue Rs.171 crore.

-

Recognition and Awards:

- Awarded “Fastest Growing Construction Company in India” at 21st Construction World Global Awards, 2023.

-

Financial Outlook:

- Company bids for large projects in new states, displaying confidence in effective nationwide execution.

-

Strategic Vision:

- Gradual move up value chain, targeting higher-ticket projects.

- Bid book spans Madhya Pradesh, Odisha, Delhi, UP.

- Aligns with 2024 budget’s Rs.11 lakh crore infrastructure allocation (3.4% of GDP).

- Commitment to India’s growth, positive development, confident in solid economic fundamentals.

-

Financial Performance (Q3FY24 vs Q3FY23):

- Revenue from Operations: Rs.697 crore (40% YoY increase).

- EBITDA: Rs.71 crore (16% YoY increase).

- EBITDA Margin: 10.25% (down from 12.39%).

- Net Profit: Rs.33 crore (8% YoY decrease).

- PAT Margin: 4.63% (down from 7.01%).

-

Expense Analysis:

- Other Expenses: Increased from Rs.5.2 crore (Q2) to Rs.8.51 crore (Q3), includes ECL provision on Trade receivables.

- Employee Costs: Rose from Rs.29.56 crore (Q2) to Rs.33.75 crore (Q3) due to appraisals.

- Finance Cost: Increased from Rs.12 crore (Q2) to Rs.15 crore (Q3) due to short-term borrowings and bill discounting.

-

Capital Expenditure and Balance Sheet:

- Capex during 9 months: Rs.142 crore, with Rs.74 crore for precast facilities.

- Long-term Borrowings: Rs.75 crore (including short-term maturities of Rs.50 crore).

- Short-term Borrowings: Rs.403 crore (excluding short-term maturities of Rs.50 crore).

- Gross Block of Assets: Rs.543 crore, Net Block Rs.325 crore (additions in Q3: Rs.34 crore).

- Net Unbilled Revenue: Rs.409 crore.

-

Working Capital and Credit Facilities:

- Working Capital Days: Debtor – 63, Creditor – 60, Inventory – 35, Total – 38.

- Utilized Credit Facilities: Rs.1,030 crore; Rs.467 crore available for utilization.

-

Fixed Deposits:

- Total Fixed Deposits: Rs.257 crore; Lien-free deposits: Rs.47 crore; FDs under lien: Rs.210 crore.

Business Growth:

- Order Book and Revenue:

- Current year’s target: Rs.3,000 crores order book.

- Next year’s projection: Rs.3,000 crores revenue, Rs.3,500 crores order book.

- Profit Margin:

- Targeted margin: 11% to 12%.

- Commitment to maintaining margins through tender criteria.

Promoter Shareholding:

- Reduced from 74% to 66% over 2-3 years.

- Reductions due to personal requirement.

- Commitment to maintaining current level (66.2%) for the next year.

- Reductions driven by personal needs.

- Approximately 10 employees beyond the promoter family earn over Rs.50 lakhs.

Revenue Growth and Projections:

- Nine-Month Performance:

- Achieved 15% revenue growth in the last nine months.

- FY24 Revenue Projection:

- Projected revenue between Rs.2,500 and Rs.2,600 crores for FY24.

Margin Outlook:

- Margin Range Adjustment:

- Margin range revised to 11-12% due to uncertainties in EPC projects.

- Fourth Quarter Margin Expectation:

- Anticipation of returning to the original margin levels after the completion of UP projects.

- Previous quarter’s lower EBITDA margin of 10.3% attributed to UP project expenses.

Equity Raising and Financial Strategy:

- Equity Enabling Resolution:

- Enabling resolution for potential growth capital needs.

- Not an urgent requirement, contingent on order book expansion and bank guarantees.

- Bank Guarantee Requirements:

- Anticipated bank guarantees for Rs.1,500 to Rs.1,600 crores order book.

- Potential need for Rs.350 to Rs.400 crores in bank guarantees, requiring a minimum margin of Rs.300 crores.

Project Updates and L1 Orders:

- L1 Order Clarification:

- L1 order of Rs.928 crores includes Science City and Gati Shakti, Vadodara projects.

- Exclusion of the dairy plant, Rajkot project, due to cancellation related to budget constraints.

- Dairy project expected to be re-tendered in March or April.

Bid Pipeline and Project Status:

- Delhi Railway Station Project:

- Status: Tender of Rs.4,800 crores has been cancelled.

- Overall Bid Pipeline:

- Total Bid Book: Stands at Rs.6,000 crores.

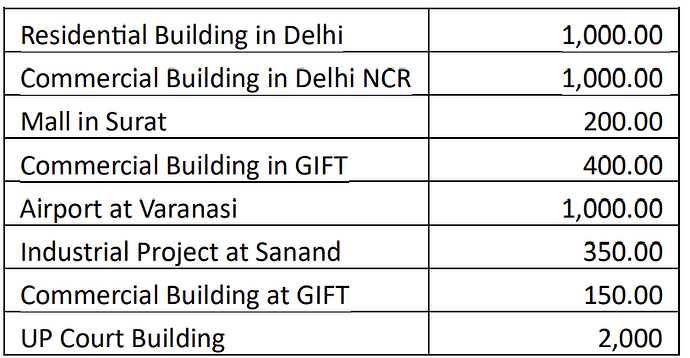

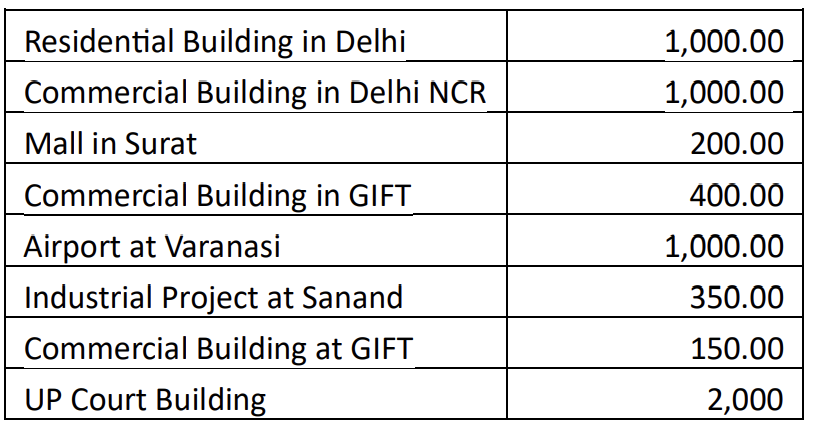

- Major Projects in Bid Pipeline:

Financial Strategy and Debt Management:

- Surat Diamond Bourse (SDB) Claim:

- Claimed amount: Rs.539 crores

- Section 9 proceedings initiated to protect funds.

- Outcome expected by end of February.

- Potential settlement of Rs.300 to Rs.400 crores.

- Equity Raising Consideration:

- Decision on equity raising contingent on SDB outcome.

- QIP option under consideration if needed.

- Monitoring the situation for the next 1-1.5 months.

- Debt Situation:

- Current combined short-term and long-term debt: Rs.478 crores.

- Rise in debt attributed to SDB and UP projects’ receivables.

- Anticipating Rs.300 crores from SDB by March to normalize debt levels.

- QIP Enablement:

- QIP enabled to address potential working capital needs.

- Ensures smoothness in working capital and reduces interest costs.

- Unbilled Revenue and CAPEX:

- Net unbilled revenue: Rs.409 crores.

- Nine months CAPEX: Rs.142 crores.

- Additional CAPEX of 2-3% anticipated for new projects in the fourth quarter.

- Upcoming Projects:

- Initiating 2-3 large projects, including Gatishakti (Rs.630 crores) and Dharoi and Sabarmati Riverfront (Rs.400+ crores).

- Anticipating minimal CAPEX for Dharoi and Sabarmati Riverfront initially.

Precast Revenue and Margins:

-

Nine-Month Precast Revenue:

- No specific figure available due to orders being from various clients.

- Anticipated overall revenue from Precast by year-end: Over Rs.180 crores.

-

Margins Expectation:

- Initial stages focused on market penetration.

- Targeting margins of 11% to 12% in the long run.

- Potential for higher margins (3% to 4%) when technology is universally accepted.

-

Current EBITDA Status:

- Presently EBITDA-positive but not at the targeted margin levels.

-

Current Utilization and Capacity:

- Present utilization: 40% to 50%.

- Total plant capacity: 30 lakh square feet per year.

-

Potential Margins with Increased Utilization:

- At 80% utilization, expected margins of 11% to 12%.

| Subscribe To Our Free Newsletter |