Abbott India is a Multinational pharma company.

The key revenue drivers in India as of now are the following segments:

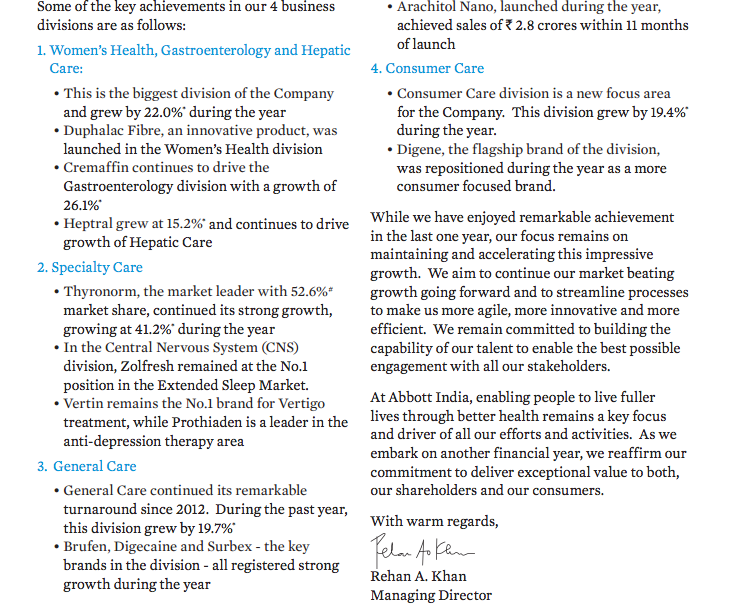

-Women’s health(biggest division)

-Specialty care(key product: Thyronorm)

-General care

-Consumer care(expected to be future growth driver)

Their parent company in the US, Abbott Nutrition private ltd sells popular products such as Pediasure (Note that these revenues don’t reflect in the Indian company as it is a 100% subsidiary of Abbott USA)

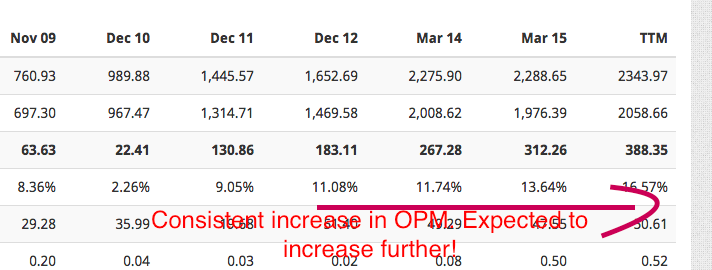

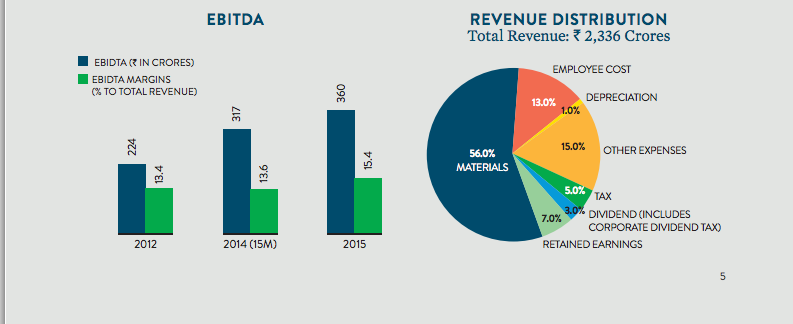

The operating profit margins show a rising trend indicating their focus on increased profitability. They are investing in assets such as real estate currently to develop the future growth drivers through branding and marketing products to consumers with high spending power. The focus seems to be in creating the brand Abbott as is reflected in the big logo which they paste on their products.

Overall, this seems to be a futuristic MNC pharma company with high growth potential. Attaching some images from the recent annual report of the company.

Key risks in my opinion include the decreasing spending power of the Indian consumer, profitability decrease for current products due to governmental norms etc.

Views & criticism from senior members & others are invited as I may be biased due to recent tracking position in my portfolio and family’s portfolio.

Disclosure : Recent tracking position

| Subscribe To Our Free Newsletter |