Supriya Lifesciences

Sector: Pharmaceuticals – Indian – Bulk Drugs & Formln companies

About the company:

Supriya Lifescience Ltd. (SLL) is engaged in manufacturing of-:

-

Active Pharmaceutical Ingredients (APIs) with a backward integrated business model and advanced manufacturing capabilities.

-

Backward integration of API business, lead to better margins and reduce dependency on import of raw material

-

The company has diversified operational presence in 86+ countries with exports contributing to ~80% of its revenue in FY23.

-

SLL is the largest exporter of -:

—–Chlorpheniramine Maleate(45-50% export from india),

—–Ketamine Hydrochloride and Salbutamol Sulphate(60-65% export from india)

—-with a niche product basket of 38 APIs as of 3QFY24. -

They were among the largest exporters of Salbutamol Sulphate contributing to 31% of the API exports from India in FY 2021 in volume.

-

Export contributes to 77.47% of FY2021 revenues, Company export to 86 countries to 1296 customers including 346 distributors

Strength and Investment Rationale

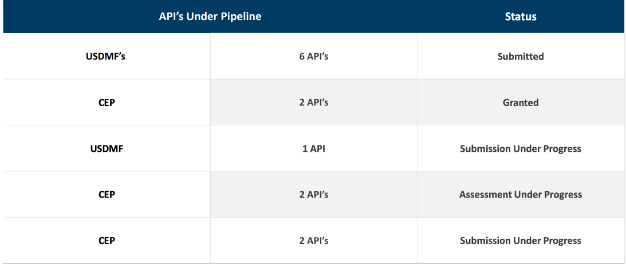

Niche product portfolio and robust launch pipeline

-

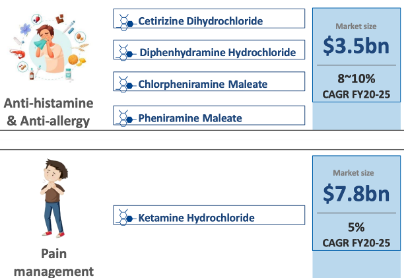

SLL has a niche product basket of 38 APIs with presence in therapeutic areas of Analgesics, Anti-histamine, vitamins, anti-asthmatics, anti-allergic and anti-malarial.

-

Company has tied up with Kalinga Institute of Technology for development of GelHeal and Quickblue Oral Kit.

Quickblue is an oral cancer detection kit which is cost-effective and efficient. Through Quickblue the company expects to create a 1%-2% market share in a USD 21.5 bn global cancer market

Quickblue kit to be commercially available in the next 3 years.

competitor is selling at INR32,000. trying to give it at a very cheaper price to common man , export is major target. -

Company has signed a memorandum of understanding with US-based Plasma Nutrition, which specialises in innovative consumer products, for manufacturing Ingredient Optimized Protein (ioProtein).

will get the sole rights for manufacturing and marketing ioProtein in India.

the trial batches and the samples have been supplied to all the large distributors of whey protein across India.

evaluating opportunity for exports also of this particular product in Southeast Asian market.

next quarter, will at least be having 20 to 30 metric tons of trial quantities from all the major distributors in India

Next financial year, it will commercialize about 100 metric tons. Let’s say quarter 2 of FY’25 is where we will see some significant volumes coming in.

next 2-3 years, anticipate that will be able to go to about 800-900 metric tons.

Robust manufacturing facilities

- Global agencies approved facility: USFDA, EUGMP, EDQM, NMPA, ANVISA(Brazilian), KFDA(Korea), PMDA(Japnese), TGA(Australia), COFEPRIS(Mexico), Taiwan FDA, Health Canada, CDSCO

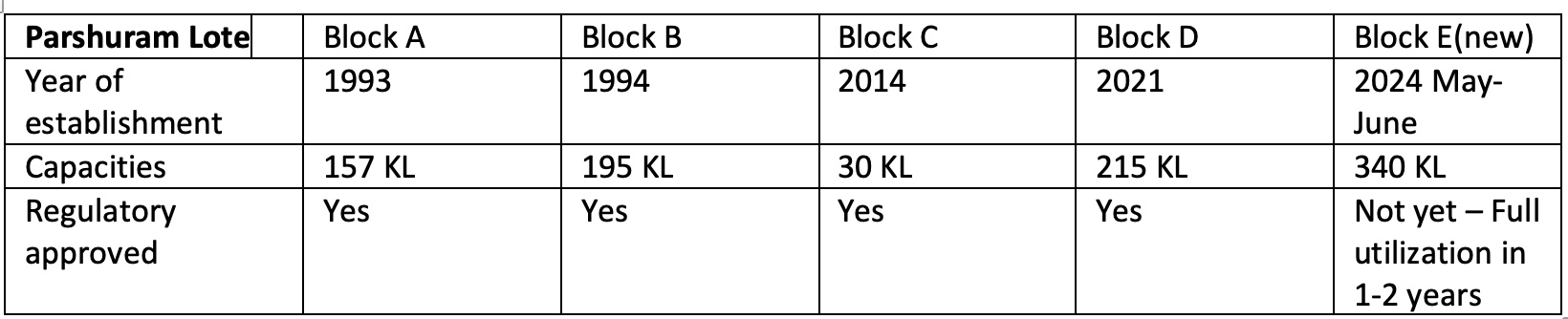

- SLL has a total reactor capacity of ~550 KL/day with capacity expansion of 340 KL/day in the Parshuram Lote manufacturing block being commercialized by 4QFY24.

- The company is also on track to set up another pilot manufacturing plant and R&D facility in Ambernath by 1QFY25 which is set to increase capacity by ~70 KL/day.

- capex program at Ambernath site with an estimated aggregate capital outlay of INR 60 crore over the next 3 years

- With these projects the total capacity will increase from 597 KL to 960 KL by early Q1 FY25

- Company also setting up a bottling line in Ambernath for about 5 million bottles a year.

- In FY22, FY23 and 1HFY24 the company has incurred capex of around Rs 94.9 cr, Rs 107.8 cr and Rs ~50 cr respectively.

- The capex is majorly diverted towards capacity expansion to cater to growing product demand.

The capacity utilization rate as of 2QFY24 is 73%.

Strong focus on R&D

- New R&D facility Has one research lab in its Parshuram Lote facility with another lab in Ambernath to be operational by Q4FY24- Q1FY25.

- These centres will help to develop identified APIs which will complement existing product profile. Ambernath would be around 70 to 100 KL depending again on the kind of product mix, it is multiproduct facility.

- SLL’s R&D efforts are mainly focused across the value chain of API process development and consistent efforts towards

developing new products

improving existing products and drug delivery systems and

expanding product applications. - In FY21, FY22 and FY23 the company spent 3.9%/6.8%/4.8% of its revenue on R&D (includes capital and revenue expenditure).

Market Reach:

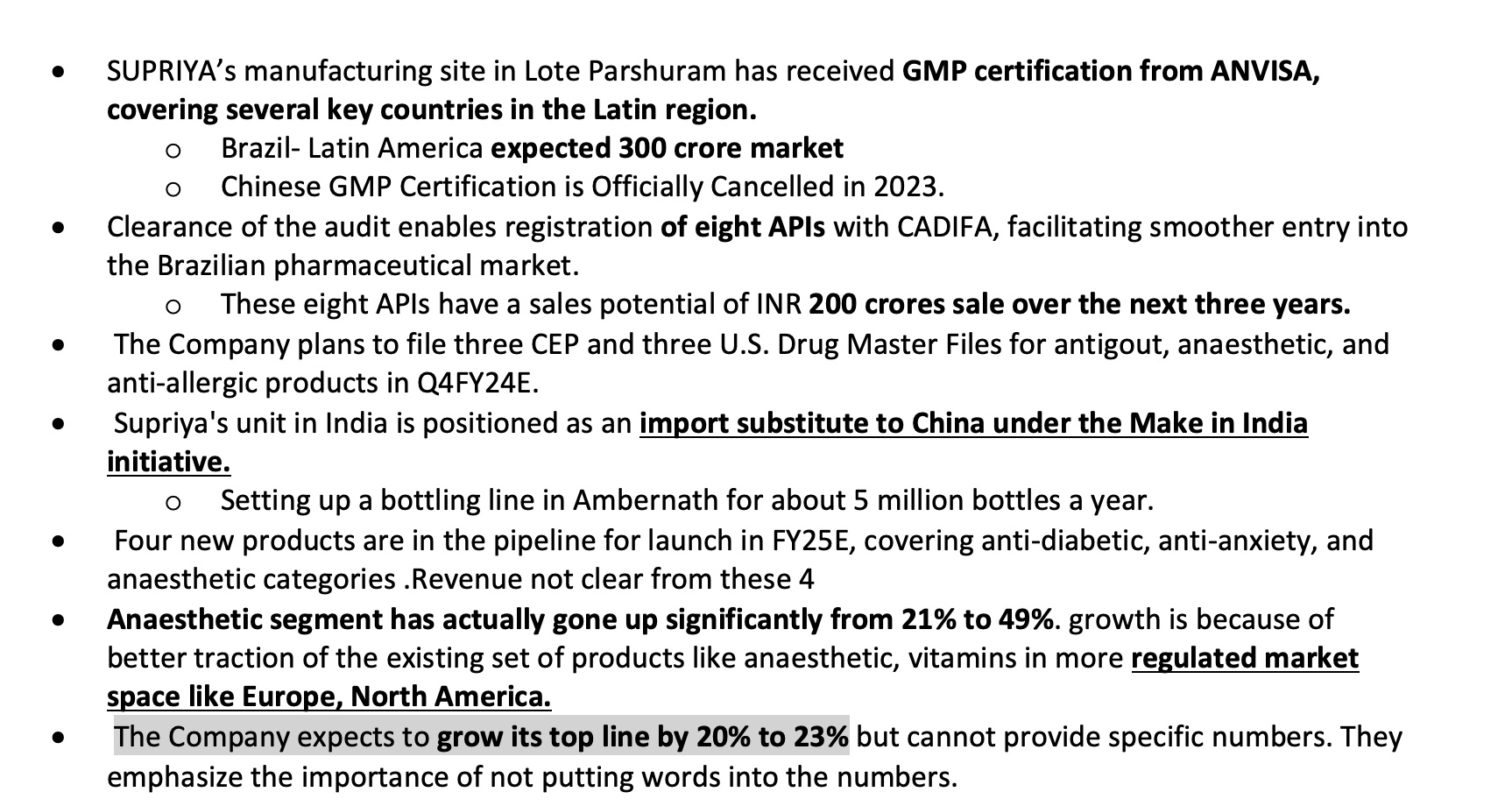

- Expanding the controlled drugs portfolio with identified APIs in the development pipeline.

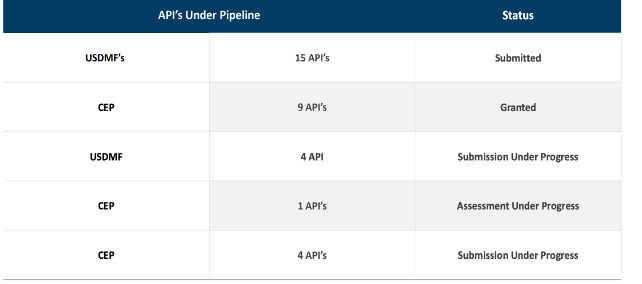

- Evaluating product portfolio expansion in anti-diabetic and CNS segments.

- Strengthening presence in existing markets through a dedicated sales team and regulatory team registrations.

- Actively pursuing business expansion in North America, Japan, Australia, and New Zealand.

India is emerging as key player in CDMO segment

- Global pharmaceutical players are continuously witnessing cost pressures and looking for ways to shorten time to market.

Thus, the industry is looking for established CDMO partners, particularly in Asian markets such as India and China - India is a preferred destination for the procurement of active pharmaceutical ingredients (APIs), especially in regulated markets, compared with China

Initiated discussion with various companies ranging from big pharma to innovator companies to work as a partner for supplying products as per their needs - In Nov 2023, announced 10-year CMO contract with a leading European company – DSM Firmenich is expected to generate peak revenue of INR 40 crores/year starting from FY27.

received first commercial order from DSM Firmenich in FY24Q3 - Company has set up a bottling line of around 5 million bottles a year. On the finished formulation front, this product is extremely large. It is the most widely used anaesthetic globally.

current market value of the product is around USD300 million. And it is growing very, very strongly. It is expected to grow at a 4.4% CAGR year on year. - Expects this business to contribute ₹100-120 crore to the revenue in the next two-three years.

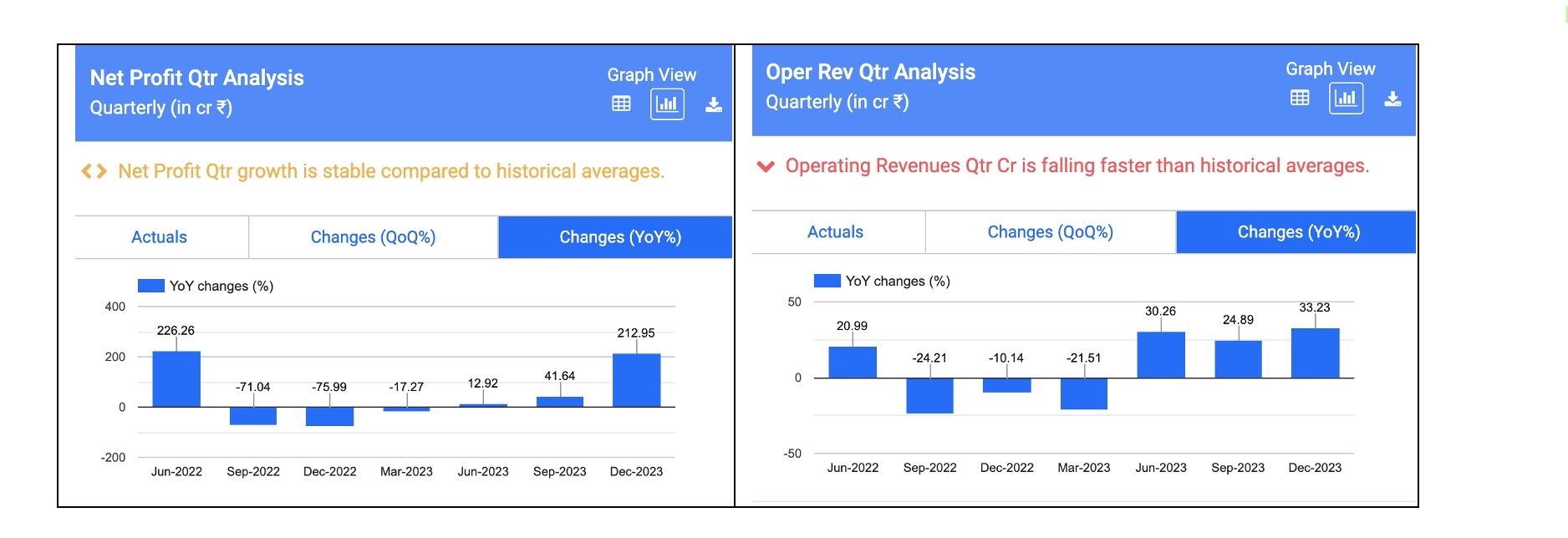

What went wrong in FY23?

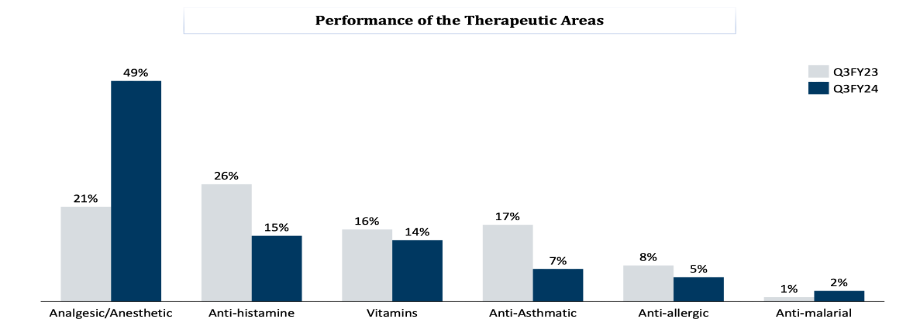

After strong set of numbers in FY22, Supriya reported dismal numbers in FY23. Revenue declined 13% while EBITDA/PAT declined by 39%/41% in FY23.

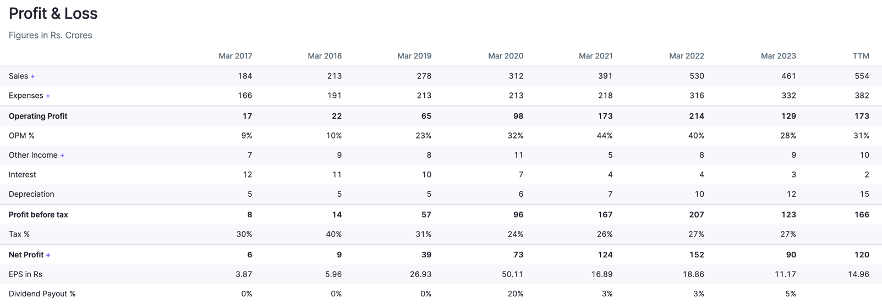

The fall in revenue was on account of low demand from the Chinese market for its key therapy i.e. Anti-histamine. Considering that China was the company’s largest export destination, marked by value-added exports, the impact translated into a decline in margins in FY23

Due to the COVID in China, usage of hand sanitisers and masks increased and people staying indoors; thereby the demand for its antihistamine range significantly dropped.

Management had highlighted that improvement will be gradual and it will take another 2-3 quarters for the situation to normalise.

Due to Covid cases inside China in FY23, a key material supplying country, raising the threat of interrupted production.

-

The company proactively stocked raw material inventory, protecting its manufacturing schedule.

-

Mitigation: The company entered in relationships with key material suppliers in India, moderating the dependence on a global supply chain.

Further, to mitigate this impact, Supriya is expanding regulatory market presence, optimizing manufacturing capacity, and diversifying product offerings and geographic reach.

Company initiated registration for other therapies such as Decongestion, Anti-hypertensive, Anti-Asthmatic, Vitamins and Antiallergic.

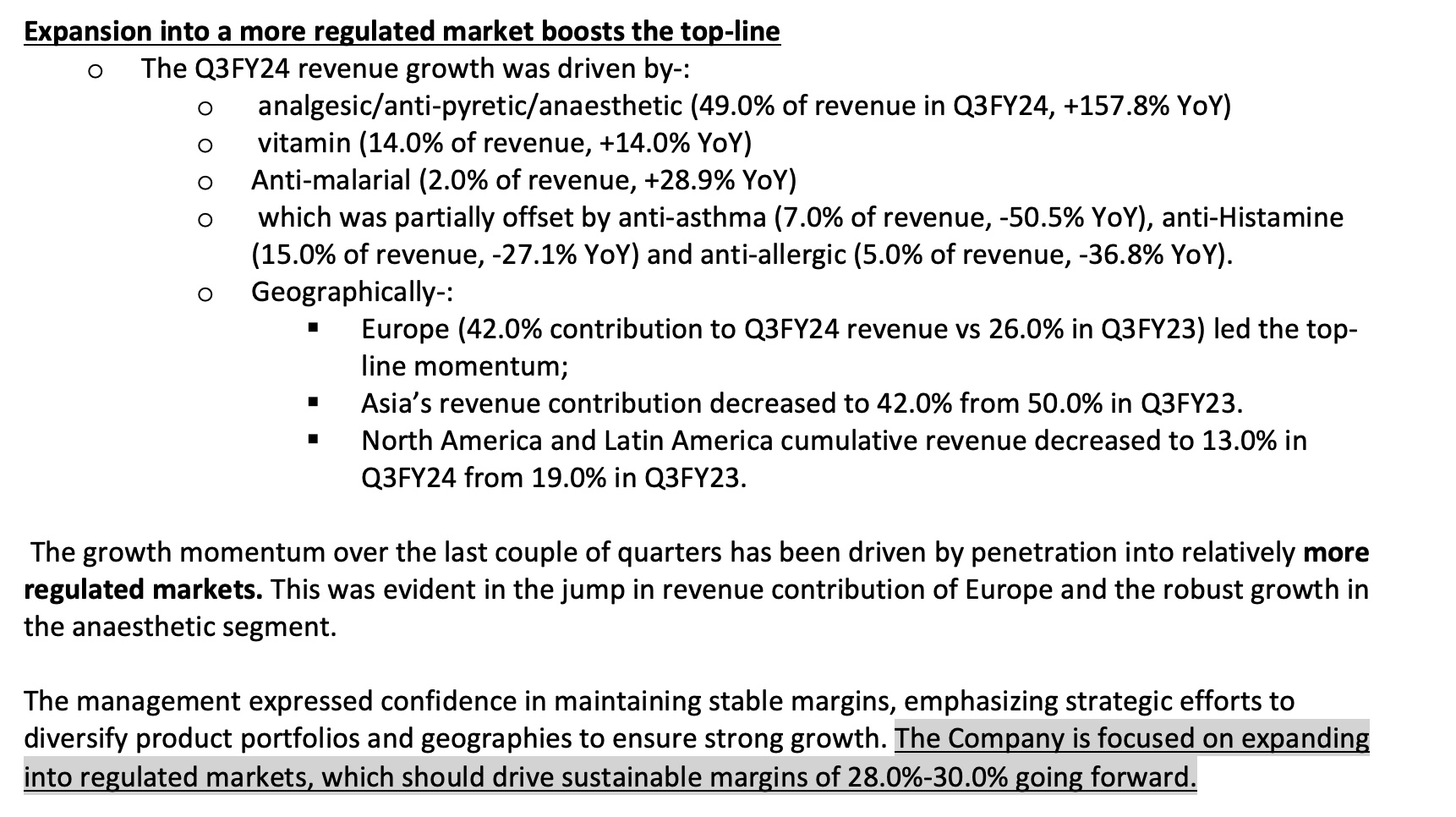

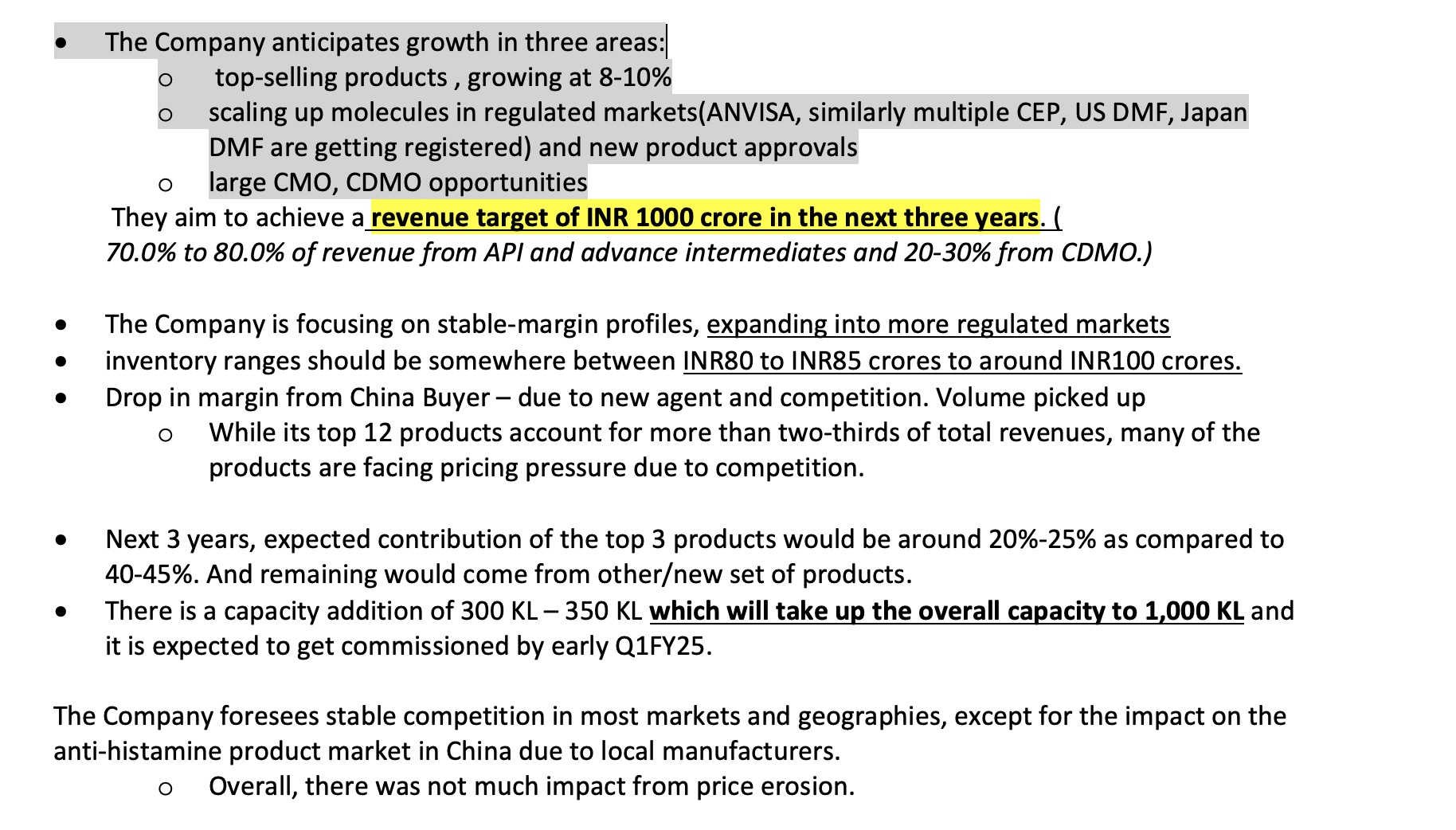

Result Highlights for Q3FY24:

Key Concal Highlights:

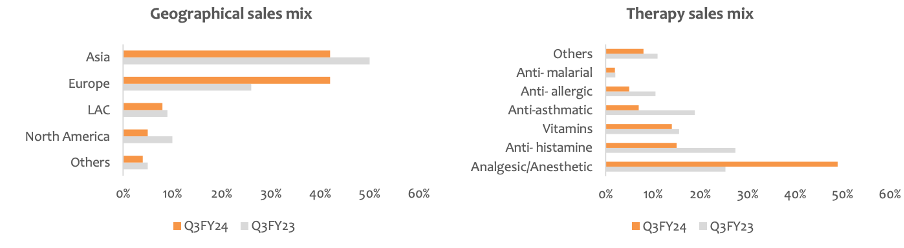

Product/Sales Mix – YoY comparison

FY22Q4:

FY23Q4

FY24Q3

Fundamentals

2022- 2023 was due to covid and recovery from issue with supplying to China , recovered by diversifying – geography , product range and getting a new broker for China buyers

Now recovered to IPO levels in 2021

Capex Spend

Company is using – internal accurals and 200 crore capital due to initial IP

Holding

Positives

Negatives

Industry Growth

• In 2024, Analgesics market revenue in India is INR US$1.12bn, an annual growth rate of 8.46% (CAGR 2024-28) is expected

• Anaesthesia Drugs market is to grow at a CAGR of 3.47% between 2021- 28. As of 2021, the market for anesthesia Drugs market size reached USD 7 Billion.

• Global Antihistamine product market was valued at US$ 263.9 billion in 2022 ,expected to expand at a CAGR of 8.6% and reach a valuation of ~US$ 647.7 billion by 2033.

• Global vitamins market is expected to be $6.7 billion in 2023 and more than $8.9 billion by the end of 2028, with a CAGR ~6.0% from 2023-28.

• Global small molecule CMO/CDMO market is around US$ 74,998.1 Million in 2024 , to exhibit a CAGR ~ 5.2% over the period 2024-34.

Pharma Growth

• Global pharmaceuticals market was valued at USD 1.4 trillion in 2021 and is expected to reach USD 2.06 trillion by 2028, growing at CAGR of 5.70% during 2022- 28.

• In 2023, North America is to account for 45.33% of the global market share. Asia-Pacific is expected to remain the second largest market with 24.07%, followed by the European market (20.24%), Latin America (7.53%) and Middle East and Africa (MEA) (2.96%).

The increase in the number of senior citizens who are prone to catching illness as well rising cases of illnesses such as diabetes and cancer is expected to contribute to this growth

Global API industry Growth

• The worldwide active pharmaceutical ingredients market was pegged at 222.4 billion in 2022 and estimated to grow at a CAGR of 5.90% from 2023 to 2030.

This growth is attributed to factors such as growing cases of cardiovascular diseases and cancer, conducive government policies for API production as well as changes in geopolitical situations

Indian API industry Growth

• By 2029, the global generic API markets are expected to grow at ~6%, whereas the Indian market is expected to have a CAGR of 13.7% from 2023-29.

• The Union Budget 2023 enhanced the fund allocation by 12x from H100 cr for 2022-23 to H1,250 cr for FY24 including drugs and medical devices

Over the last couple of years, the Indian API industry has received USD 4-5 billion investment, which also include venture capital

Leadership

**Dr Satish Wagh**

Established in the year 1987, Supriya Lifescience Ltd. is the largest producer of anti-histamines, anaesthetics & anti-asthmatics in the world and has put Maharashtra and India on the world map in the pharmaceutical sector. Dr. Satish Wagh is the Founder & CMD of the company. Additionally he was also the chairman of CHEMEXCIL for 22 years. He was also listed in ‘Forbes powerful Performers 2021’ and ‘Economic Times Most Influential Leaders of 2022’

Risk

Revenue concentration risk:

• Company faces product concentration risk as top-5 products contribute major portion of their revenue. Any delay in development and commercialization of newer products could impact future growth prospects of the company.

o Adding new products and in the process of implementing additional manufacturing facilities, effectively reducing the risk associated with location concentration

Foreign exchange fluctuations may impact the company as more than 80% of revenue come from exports sales.

• Company’s inability to effectively utilize its manufacturing capacities could have an adverse effect on the business.

Competitor Risk

• The presence of multiple prominent pharmaceutical firms enhances competition within the pharmaceutical sector.

• chooses products which are mature and where demand is not likely to taper off soon.

• This presents a difficulty for the Company to improve its market share and overall profitability.

• The Company’s extensive operational capacity, backward integration, and regulatory influence have enabled it to demonstrate an expanding order book from regulated markets

Customer concentration risk

• 48% of revenue from Top-10 customers, and the potential loss of one or more of these clients, their weakened financial outlook, or a decrease in their demand for our products could negatively impact our business outcomes. T

Company is experiencing positive momentum in its Contract Manufacturing Organization (CMO) and Contract Development and Manufacturing Organization (CDMO)

Market risk:

• The development and commercialization processes of new products is resource-intensive and time consuming

consistently create and introduce new products

IT risk:

• Pharmaceutical sector undergoes rapid transformations due to technological progress and scientific breakthroughs.

Company is engaged in establishing 2 additional manufacturing units while also enhancing its current infrastructure, emphasizing the integration of cutting-edge automation technology.

Credit risk:

• Handles credit risk through procedures like credit approvals, the establishment of credit ceilings, and ongoing assessment of the creditworthiness of customers

For export transactions, every sale is safeguarded by ECGC, while domestic sales benefit from trade credit coverage.

Regulatory risk:

• Failure to adhere to the regulations stipulated by governmental bodies and regulatory agencies can have adverse effects on the Company’s business, financial outcomes, and operations

• markets such as the USA and Europe where its products are sold, the Company’s manufacturing facilities and products must receive approval from regulatory authorities before distribution agents

• many of these approvals necessitate periodic renewal

Only Family in Board Leadership

- If Company doesn’t effectively utilize its manufacturing capacities it could have an adverse effect on the business.

Things that is not yet clear( Needs to be understood More):

- Inventory Turnover Ratio: 1.94 – Average-okish, previously during 2022 was very high as 4.5+

sales maybe slightly weak and product demand might be waning. This could result in excess inventory on the warehouse shelves and wasted space and resources. - Would be good to get company’s export data and see how the change in export trend is for company

My outlook for Supriya Lifescience

Reasonable valuation

• At current price, the stock trades at FY24E/FY25E consolidated PE of 21.2x/17.5x respectively. The company’s current capacity is ~550 KL/day which would be doubled in the next financial year to ~1070 KL/day adding topline growth of 20%-25% CAGR between FY23 to FY25.

o Company guidance – strong double digit revenue growth along with margin in the band of 30-32% in the next 2 years.

• Company intends to enter the pain management, anti-anxiety and anti-diabetic segments , vitamins and protein powders- sustainable growth opportunities.

• Company was able to continue the growth momentum by penetrating into regulated markets such as Europe where the revenue contribution has significantly increased.

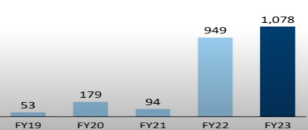

• With consistent growth of 25% , company should be reaching revenue of 1000 crore over 3 years.

o Prediction(Subject to Risk and Market): FY24E Revenue(current) – 550+ , FY25E- 660+, FY26E -800+ , FY27E-1000+

• This should result over slow growth in stock and stock price growing from 350 to 700+ in next 3 years, yearly price growth average of 20-30%

Recommended Buy -Needs to be revisited on FY24q4

Sources : Trendlyne, Screener, company website, News Articles, Company presentations, Earning calls, HDFC securities report, and ofcourse Google

| Subscribe To Our Free Newsletter |