Q3-FY 24 Con call notes and some other notes

Although a major portion of the notes is from the Q3 call, I have added some more references to understand things better, for example, Deferred Tax asset or Andheri land.

General

-

Added 93 Branches in the last 12 months

-

Productivity of branches in 1 to 2-year vintage is 2X 6-12 months vintage

-

Target Openex to Asset ratio of 3.5 to 4.0%

-

Today, its Opex to asset ratio is 5.6 (5.8 last quarter)

-

Wholesale AUM (excluding non-yielding assets, SR, Land Receivable assets, DHFL Book) 11,197 cr. Aiming to bring this down to zero in next few quarters

-

Wholesale SR reduced due to cash realisation of 909 cr since Q1-24

-

Shriram’s life (14.9% stake) and general insurance (13.3% stake) business is on the book at 1709 cr

-

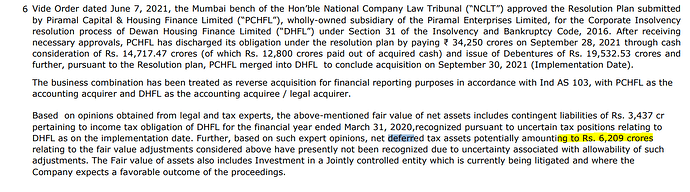

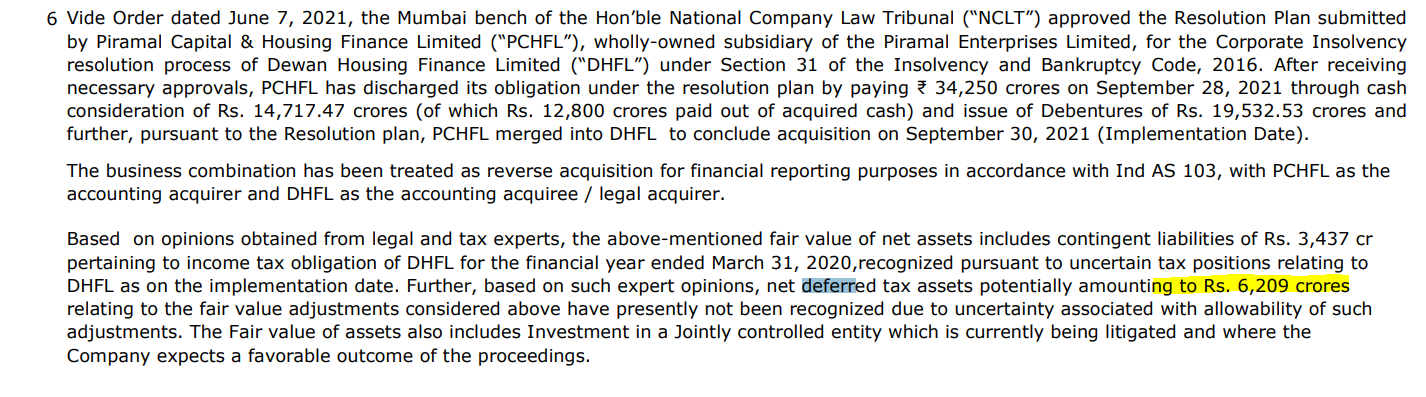

Deferred Tax Asset timeline in Q4 with tax authority. We should hear in the Q4 result. As per this link it was 6209 cr in June 2022.

-

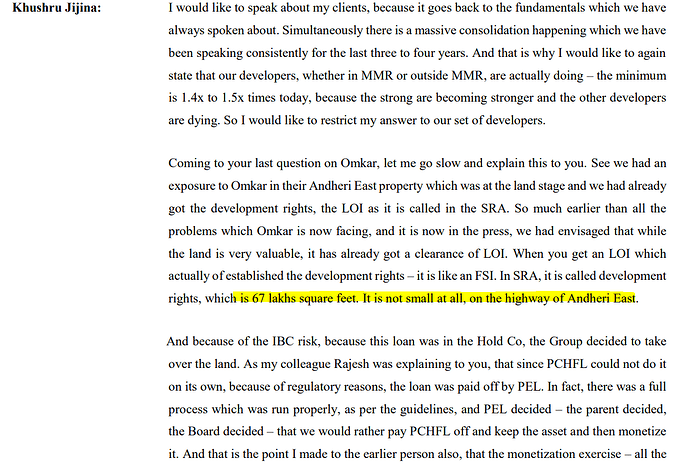

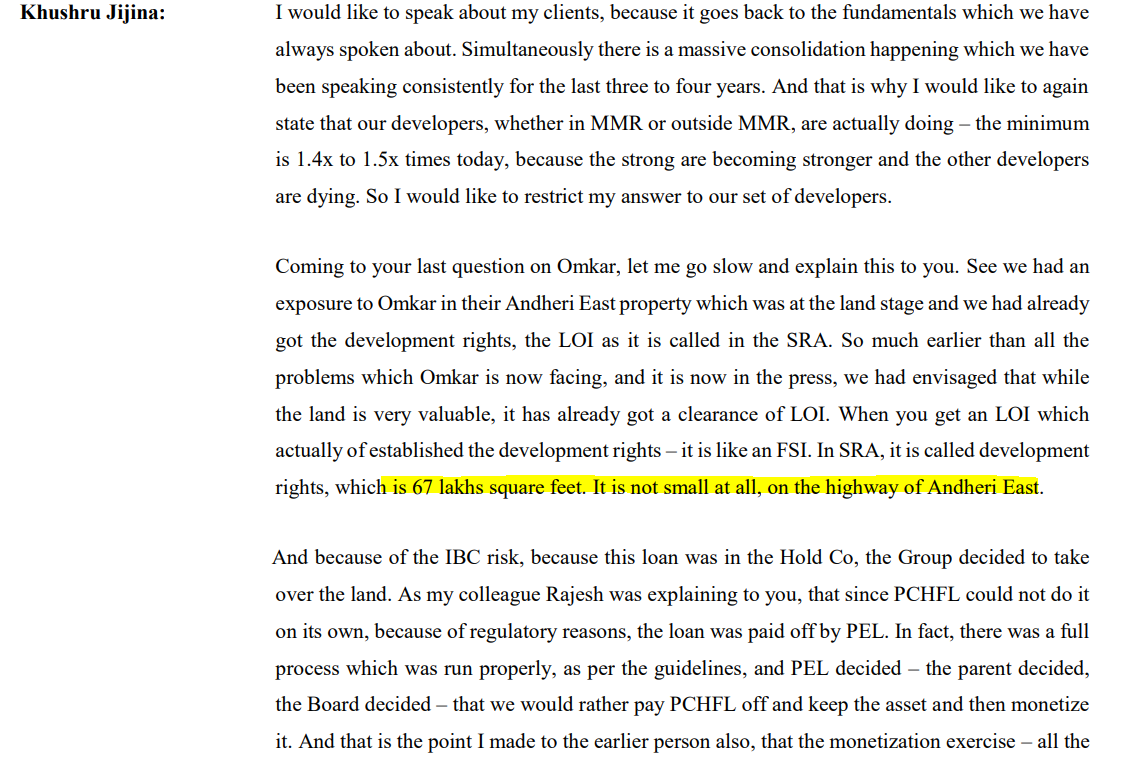

Andheri East Land- 67 lakh square feet on Andheri East Highway. Work in progress for monetisation. It is around 1300 cr on the book as ‘Investment property’. Below snapshot from old con call for reference.

Road to 3% ROA (by FY28 as per Investor Day PPT)

- There things that need to happen

- OpenX need to come down from the current level (5.6%) to around 3%

- Yield plus fees need to go up

- A moderation in the cost of borrowing.

If these things happen, ROA will improve even if credit costs remain in the same range (1.5%)

AIF

- It was formed in 2020 and comprised 35 loans. Of this, 22 loans exited and 13 remaining. Proceeds of this 22 have been used to bring down AIF

- All 13 loans are residential real estate projects. One project is backed by an undeveloped or early-stage land parcel

- earlier, it was 8000 cr. Now it is 3500 cr

- Confident of recovering pretty much everything.

- As per CNBC interview, most of it shall be recovered in the next 6/8 quarter (major shall be recovered in the first 5/6 quarter).

Unsecured Loan

- Total is 10,000 cr. But less than Rs 50,000 loan book is 600 cr( there is a serious strain in Rs 50k and below loan book overall)

- This part of the book is a flywheel kind of business. PEL is originating a bunch of customers, but only a small part of it will be going to become large ticket customers in future

Fintech business

- Done at 14/15% IRR. 90% of this business is protected through FLDG(First Loss Default Guarantee), which means PEL is not taking any credit costs.

- Essentially, it is a 14% IRR business with no opex and no credit cost, so hence, it is profitable.

- Currently, it is done through partnership, but looking forward to doing it internally

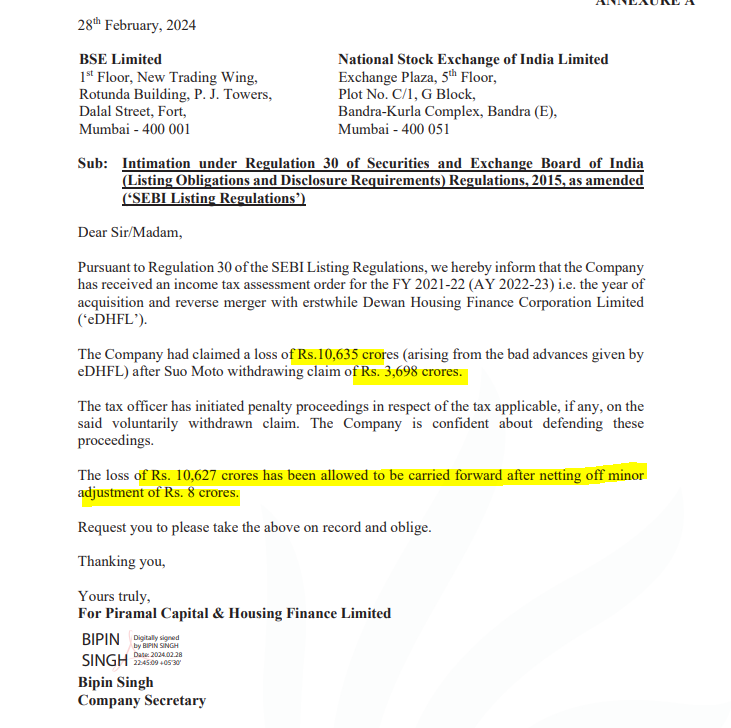

PEL Just reported that they are allowed to carry forward losses of Rs 10627 cr. Not sure it this is same as Deferred Tax asset referred above.

Note: Invested

| Subscribe To Our Free Newsletter |