Positives:-

-

Aarti Industries Promoter – Chandrakant Vallabhaji Gogri has the major stake in the company. He invested to turnaround the company.

-

Expectations of turnaround look good with the majority exposure in Middle East and India – both high growth economies.

UAE – UAE seven states at Dubai, Sharjah, Abu Dhabi, Ajman, Ras AlKhaimah; then we have GCC Qatar, Bahrain, Oman; and certain 1 or 2 customers in Pakistan; then some 3 customers in Africa right now we have.

India -We are mostly right now 75% to 80% in the western India and particularly Mumbai, Pune, and a little part of that Vapi, Daman, Valsad, and Surat. -

Strong Player in its segment.

-

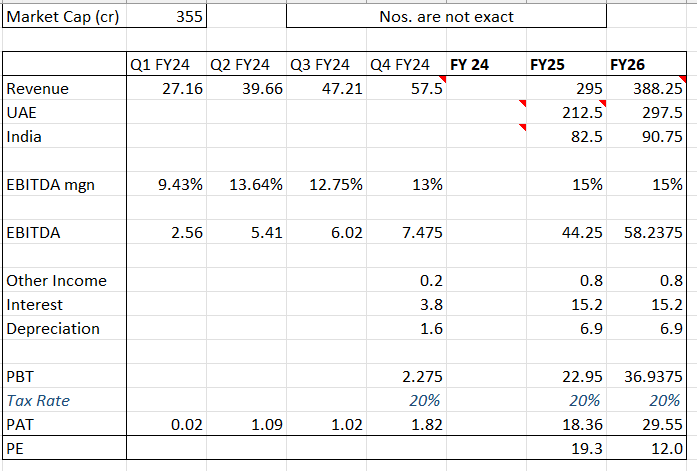

Outlook as per the company –

“I will just give you the forward projections for the Q4. Consolidated, we will be around Rs. 55 crores to Rs. 60 crores for the Q4. And for financial year FY25, India operations will be around Rs. 80 crores to Rs. 85 crores and Dubai will be around Rs. 200 crores to Rs. 225 crores. “

It is confident of increasing revenue well beyond FY25 at a similar pace. (can expect 40% to be conservative.)

Risks:-

- Cash flow issues due to working capital increases, bad creditors and debt servicing.

- Inability to crack the middle east market on which the company is counting on.

| Subscribe To Our Free Newsletter |