Hi guys ,

Current situation

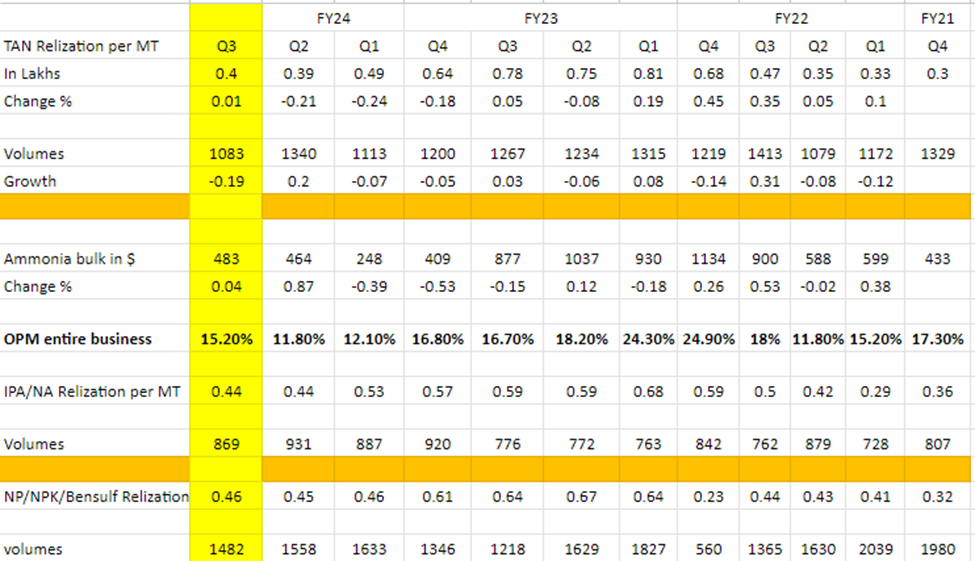

- From this table I just came up with this theory earlier that ammonia is a leading indicator of TAN realization with 1 quarter lag. Like Q3FY22 AM up by 53% from Q2 and in Q4FY22 TAN up by 45%. Now see this for the rest of the table.

What I am not able to understand is in Q2FY24 AM was up by 87% but in Q3FY24 TAN realization was same. (May be dumping effect)

So what management says already Russia was dumping in India + what they used to export to Brazil that is also being dumped in India because demand in Brazil is low.

QoQ the sales are down by approx. 600cr= 120cr of chemical and 410 of less fertilized trading + fertilizer margins also impacted (totally unexpected after last quarter volume trends) + this quarter we again had 34cr of stabilization loss. I was looking at a 150-200cr PAT for Q3 which was achievable if we did not have these 2 surprises. Totally unexpected!

QoQ fertilizer segment result from 42cr PAT to 76lakh loss. Figure in lakh

Next quarter

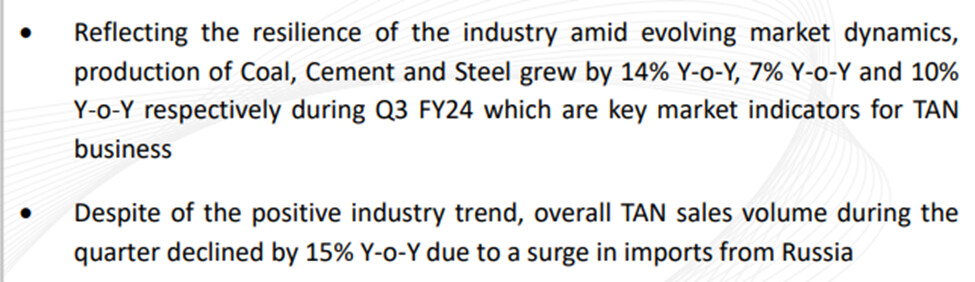

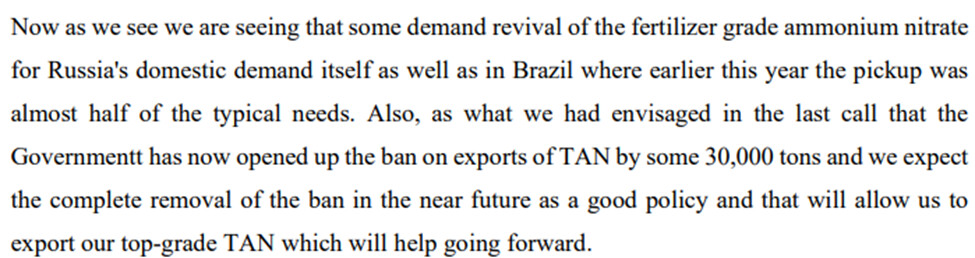

- TAN export is going to start + management is expecting Russia dumping to slowdown as their demand is picking(need to find a way to verify this) but this is going to be very less like 6% of overall capacity any more lift would be beneficial

- Fertilizer segment

Now with 10% PBT margins cap, approx. 6.5% to 7% PAT margins is what they can do going forward, this year fertilizer segment was a disaster. Last FY approx. 5000cr sales were done from fertilizer and until now 3000cr has been done. So assuming 4000cr of sales 260cr to 280cr from this segment is possible going forward

- Ammonia

So they are waiting for the eligibility certificate for the state government incentives, so this is I think the 9% GST wavier on sale price, so if they get it then they can realize all the benefit in Q4 or Q1FY25 for all the production since august.

Current economics are such that Cost of production 470$ (20$ drop qoq) and current ammonia price is 362$ + all benefits = 510$ so 40$ = 150cr about 40cr for Q4. They said plant has stabilized, so maybe next quarter we can see the benefit incase ammonia does not fall further

Lets say they do 6000cr in entire chemicals segment taking a margin of 20% (pretax, pre-interest) that would be 1200cr PBIT, approx. 400cr interest so PAT can be 600cr (this is just math, I have done it for the sake of it to have a number in front of me, plz correct if I went wrong anywhere)

For current 9FY24 months 800cr is PBIT for chemical segment I have taken the same above

All in all 600cr + 260cr + 110cr = 970cr is the PAT we can expect at current run rate for FY25 (purely mathematical)

Negatives for lower PAT is more surprise on fertilizer segment , ammonia price falling, continued Russia dumping, interest cost increasing.

Positives for higher PAT is Ammonia price stable/increasing, export ban complete lifting, anti-dumping duty, interest cost decreasing, debt decreasing from ammonia cash flow.

New contract done

New gas price from 1jan 2026. What is going to be the price, management gave some clue in previous concall.

360$ of GAS cost and taking current price of 360$ (long term average is 400 to 450) the savings is approx. 150$, taking 90% utilization = 570cr (this should be higher)

If we take avg ammonia price 450$ then the benefit can be 920cr and this is base case because we are taking avg ammonia prices

This is 2yrs and 8months away to begin with and 3yrs 8months away to realize the benefit

Now guys based on the assumptions above looks like it is a 1000cr business at current run rate but the business is so dynamic we don’t know which segment can eat way our bottle line . Now we need to understand what growth it offers on top line for next 2 to 3yrs and based on that what PE/valuations it deserves, this would give us a rough idea of upside and then we can take our call weather it is a good investment or not. (If somebody can do this exercise that would be helpful) i would do this sometime later and share my view

I would advise to consider their 2capex and TAN as a solution, entering into solar grade when doing the above exercise.

Thank you and sorry for the delay

| Subscribe To Our Free Newsletter |