Hi Guys I was thinking let’s re-evaluate the wind and set some realistic targets, my previous work is almost 1yrs old so I thought I’d update myself.

So to avoid confusion I will use “” quotes when I am directly quoting form a report so that we know what are my words and what are not.

What kind of wind installation can we expect in coming times

“”In the ambitious scenario, India instals 26.2 GW of onshore wind between 2023 and 2027, reaching 68.1 GW onshore wind capacity by 2027. It can be segmented into 23.4 GW coming from central and state tenders and 2.8 GW from the C&I sector. Of the 23.4GW volume, 12.5 GW is from existing pipelines and 10.9 GW from new tender awards.””

Now what Suzlon has said in one of the interview few days back is currently there are 12GW with OEM under execution out of which 3GW is C&I and 15GW of orders are yet to be awarded to OEM out of this 5GW is C&I

Now both suzlon and the report almost match but out of this 15GW to be given to OEM there is definitely going to be few drop outs and post july 2025 we would have a slow down as well. So I think it would be fair to assume that 22GW to 25GW is what we are looking btw CY24-27

Another very interesting point I would like to bring to your attention is our target was 140GW by 2030 but the Central Electricity Authority (CEA) indicates that cumulative installed capacity of 100 GW might only be achieved by 2030, This is like 56GW in next 7yrs so the most bullish case also show 8GW per year for next 7yrs.

I personally feel that this would not be achieved, we will further have a cut in our target going forward.

Another interesting point is currently we generate 1642 BU (billion units) of electricity this will go up to 2440 BU by 2030. So to keep an optimal generation capacity mix we need only 100 GW of wind components by 2030 in the mix. as per CEA

Why is the C&I segment still doing wind and what does GWEC think about it? Please note they are a big contributor in demand right now so any slowdown here would impact wind players.

“” Given the lower per unit economics of solar they have become the first choice of C&I segment. In 2022, ~300 MW of wind was installed in the C&I sector, significantly higher than ~100 MW in 2021, however, in the same period, 3.4 GW of solar was installed in 2022 and ~700 MW in 2021.””

“”Main reason for uptick of wind in C&I is saturation of C&I consumers with 20-30% power consumption coming from solar, expansion beyond which is difficult without storage or supportive banking regulations;Despite a huge potential, the market can swing between 200 MW to 700 MW in the coming 5 years, unless C&I consumers’ needs become more specific to wind generation needs””.

So guy storage cost coming down is a real problem, solar + storage would be the preference if they are cost competitive. Lets see some unit economics. These are old figures, current storage might be lower.

Another angle of what we should expect by 2027

““The Ministry of Power (MoP) has given an RPO target to DISCOMs of estimated 57.5 GW by 2027; 33.1 GW is already installed as of 2022 (Excludes 9GW of C&I installed), leading to a gap of 24.4 GW which needs to be fulfilled by 2027. State regulators have already set an RPO target of 19 GW, against which the state DISCOMS have committed to procure 17 GW from wind so far.””

Now on this we can add C&I + some more states will set their targets or increase because 24.4GW is the gap, We can assume 19-20GW from State discom and about 3GW to 5GW form C&I again we are close to the same number 23GW to 25GW between CY23-27

What is the current Run rate?

In CY23 we did about 2.8GW and this year expected to to 3.8GW (heard from some suzlon interview) now compare this to the above image you would notice that the current run rate is going at the base case assumprion.

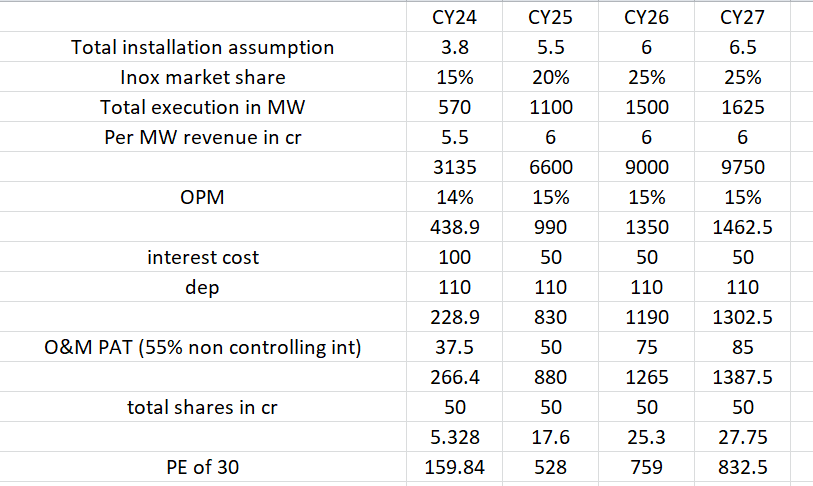

Now I would analyse Inox with the following numbers at india level CY24 3.8GW, CY25 5.5GW, CY26 6GW and CY27 6.5GW ,so 21.8GW btw CY24-27

There will be some confusion in CY/FY as CY has 2FY in it sorry for that

Guys above is purely mathematical and I might have done a lot of mistakes, I would appreciate if somebody could help

Since IWEL shareholders would get some 15.8 shares per share I have adjusted the total shares to 50cr

The O&M business generates 8-10 lakhs of revenue per MW currently they have 3200MW and they expect 50-55% EBITA and inox has 55% stake accordingly I have added the at PAT level (I can be wrong here)

I have taken a PE of 30 which is very high as per me.

Doc used GWEC-India-Outlook-Aug-2023-1.pdf & CEA report

@nandan_ganatra I say your tweet on inox being 9X FY26 on cash basis, would love to see the break up from your side

Disc- invested, but will look to trim

| Subscribe To Our Free Newsletter |