Q3FY24 Concall Highlights:

-

Orders Update: The company announced new orders and LOIs totalling approximately INR2,421 crores in Q3 . There was an order inflow of INR3,106 crores announced in the first half, our total order inflow, including LOIs in first few quarters of FY ’24 has now touched approximately INR 5,527 crores. With these new orders, our unexecuted order book as on 31st December 2023 has increased to approximately INR8,750 crores with nearly 87% of the order book comprising domestic EPC projects, which are executable over the next 12 to 18 months.

-

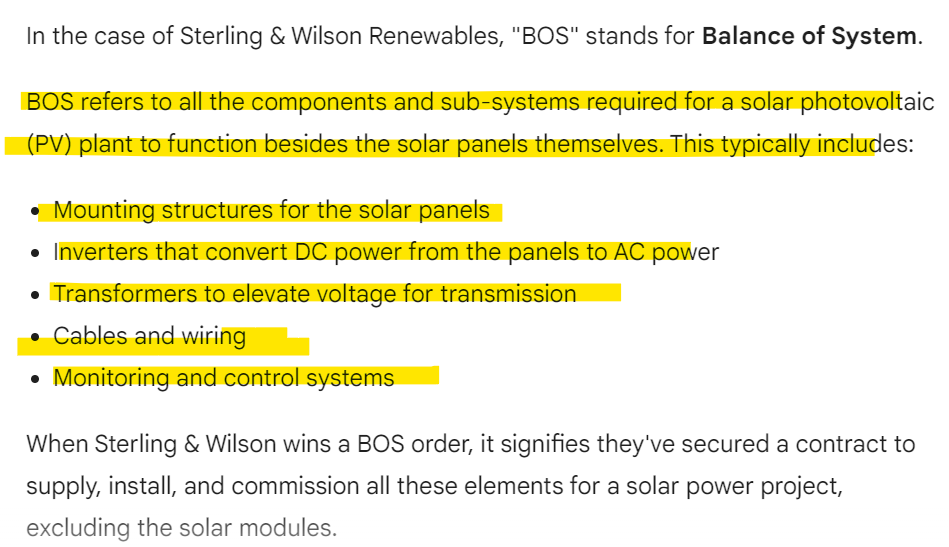

Its First large international EPC order in nearly 3 years is BOS order for a 221- megawatt DC project in Spain. Through this project, SWERL has achieved a key breakthrough in the European solar market: The scope of work includes design, engineering, supply, excluding PV modules and transformer, construction, erection, testing and commissioning. The total contract value, including 3 years operation & maintenance is approximately EUR 112 million. The order was bagged from ENI Plenitude. This is one of the major European utilities giants with a fast-growing presence in the renewable segment.

-

It has won a 220-megawatt DC floating solar project, which also happens to be one of the single-largest floating solar blocks awarded till date in the country. The scope of the project includes modules and EPC work and the project is located in the state of Jharkhand.

-

Through the relationship, it has bagged another project from Sembcorp India subsidiary for a 528-megawatt DC project in Rajasthan.

-

Bidding pipeline in Fy25: expecting almost 40 gigawatt of big pipeline to be bid out in the domestic market alone by FY ’25 with the major chunk anticipated to come from PSUs.

-

Opportunities in FY25: In the Middle East alone, They are seeing several gigawatt field projects taking shape across Saudi Arabia, UAE, Oman, et cetera, which should bid out in the next 12 months.We are hopeful of tapping into big opportunities of mega projects subject to them matching our risk profile with cautious approach.

-

Industry Outlook: There has been a significant decline in the price of modules in the last 12 months, with module price now falling to less than $0.13 per watt peak.

-

Better demand in EPC biz due to low cost of modules:

-

Revenues for Q3: It was lower sequentially due to the execution challenges we faced from tight working capital conditions seen during the course of the Q3.

-

Working Capital improvements due to below 3 reasons:

-

QIP proceeds of approximately INR1,500 crores in December.

-

Promoter indemnity inflows at the end of November.

-

And third, proceeds from a settlement with a vendor which was received in the middle of December.

-

Domestic EPC margins: Margins ins q3 were approximately 9.5% and stand at about 10.5% for 9 months FY ’24.

-

O&M segment margins were approximately 15% for this quarter due to certain one-off expenditures incurred post monsoon but it would be 25-30%.

-

Balance Sheet improvement: Cash & cash equivalents of approximately INR550 crores, and our net debt stood at INR27 crores and our net worth at INR982 crores.

-

The total repayments as at date, including those with earmarked fixed deposits is about INR1,800.

-

our projects continue to operate in a negative working capital cycle.

-

Bids in process and in pipeline: There is a significant bid pipeline of 6 gigawatts as we have said that orders remain – order booking remains lumpy based on various quarters.some of the tenders that have been already submitted, which we are awaiting for reverse auction and a lot of bids are yet to be submitted in this quarter, with quite a few we are expecting to conclude within this quarter.

-

So, with respect to the Nigeria project, we are expecting it to get concluded soon, discussions are – at a very high level are still going on, and we expect to get it concluded soon.

-

Capabilities: we are already working on hybrid projects involving batteries. So in various geographies, we are bidding for those projects and in-house capability exists for standalone battery projects or battery projects coupled with solar.

-

Green Hydrogen outlook: major projects are yet to take off the ground, major action, whatever is happening is right now electrolyser manufacturing space. So whenever the substantial projects start hitting the market, so we’ll address that accordingly

-

We can expect traction with respect to standalone battery projects and the pure solar projects, both in Australia and New Zealand markets.

-

Net debt of 377 crores left as it had paid out INR1,600 crores out of 2,178 crores, and we had prepaid another INR125 crores in January.

-

Litigation in process: It relates to an issue on the customer with which we had a surety bond assurance. And what is the situation on that because we could enforce that surety bond. Resolutions in favor would result in cash from them.

-

TAM: So the total bid pipeline we expect in the next 5 quarters is more than 40 gigawatts.

-

Pledge by the principal shareholders, which is essentially, Shapoorji Pallonji and there is a long term loan against it.

-

Revenue for EPC company: So the standard way to recognize revenue for an EPC contract is percentage completion as the project progresses.

-

Timeline to execute the orders: 12-18 months for 8700 crores order.

-

Operating leverage would be in play with increase in revenues.

-

The company is still cashing out somewhere between INR850 crores to INR875 cr. and 400-450 crores is something that could crystallize by this September.

-

All of these projects are negative working capital. They are all cash positive.

-

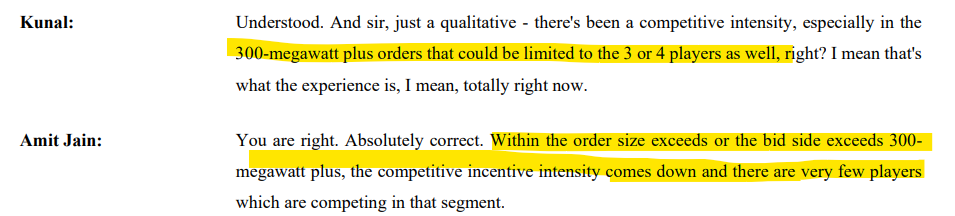

Competitive Intensity over 300 mW+ is very less as there are only 3-4 players in this space and SWSolar and L&T are the ones:

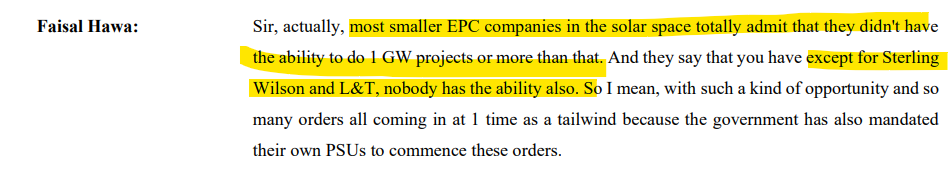

- L&T and SwSolar are the only player to do EPC with 1GW ability:

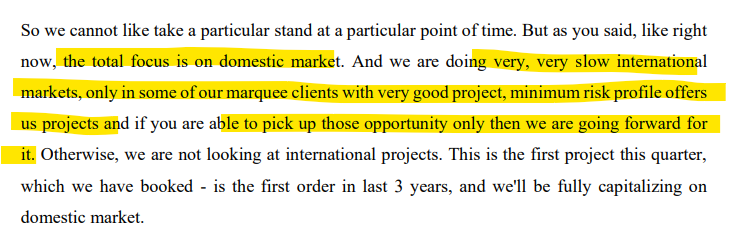

- Being choosy while picking international EPC orders to minimise risk which happened due to covid :

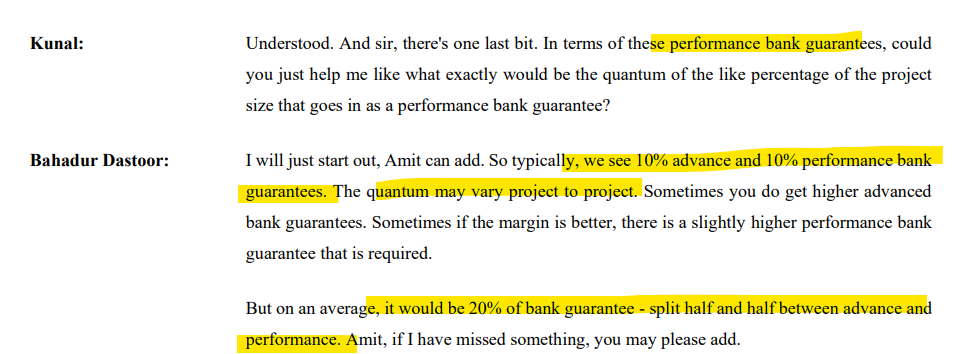

- Bank guarantee compared to project size:

Disclaimer: tracking, only for educational purpose

| Subscribe To Our Free Newsletter |