2 pharma experts talk about Wockhardt. Listen from 53.45:

https://x.com/unseenvalue/status/1769060267634180304?s=20

The point made by Mr. Aditya Khemka:

“Wockhardt announced that they have met some clinical endpoint. You study the trial design and compare it with other drugs. If I am a pharma company, I have the ability to design the trial in a manner that it is geared to show successful results. Are those results acceptable to the regulator? Probably not. If I am a disciplined pharma company, I will design the trial which is geared to fail and then if my drug succeeds, regulator will never say no to it because my design itself was very tough.”

I think he is wrong on many aspects. Trial design is developed in consultation with regulators. These designs have to follow international guidelines. And the trials do have discriminatory power to reveal under performing drug. The guidelines are such that a bad drug will show up irrespective of how you design it.

Many examples in the recent past – Tebipenem and Eravacycline failed, Cefiderocol failed in CREDIBLE CR!!! (Orchid has received sublicense to manufacture this drug for LMIC)

And Aditya sir makes it worse by not naming which drug he is talking about. WCK 4873 (Nafithromycin) has completed phase 3 and this was not a global trial. WCK 5222 is still in phase 3. We will look at the trial design of both.

WCK 5222:

THE TRIAL DESIGN WAS SUGGESTED BY US FDA!!!

Both India and US trials are public. Link to global Phase 3 trial of WCK 5222:

https://clinicaltrials.gov/study/NCT04979806?a=7

“A Phase 3, Randomized, Double-blind, Multicenter, Comparative Study to Determine the Efficacy and Safety of Cefepime-zidebactam vs. Meropenem in the Treatment of Complicated Urinary Tract Infection or Acute Pyelonephritis in Adults”

Why Meropenem is the comparator drug?

As per regulators, a new drug has to be compared with standard of care. Meropenem is the SOC for cUTI.

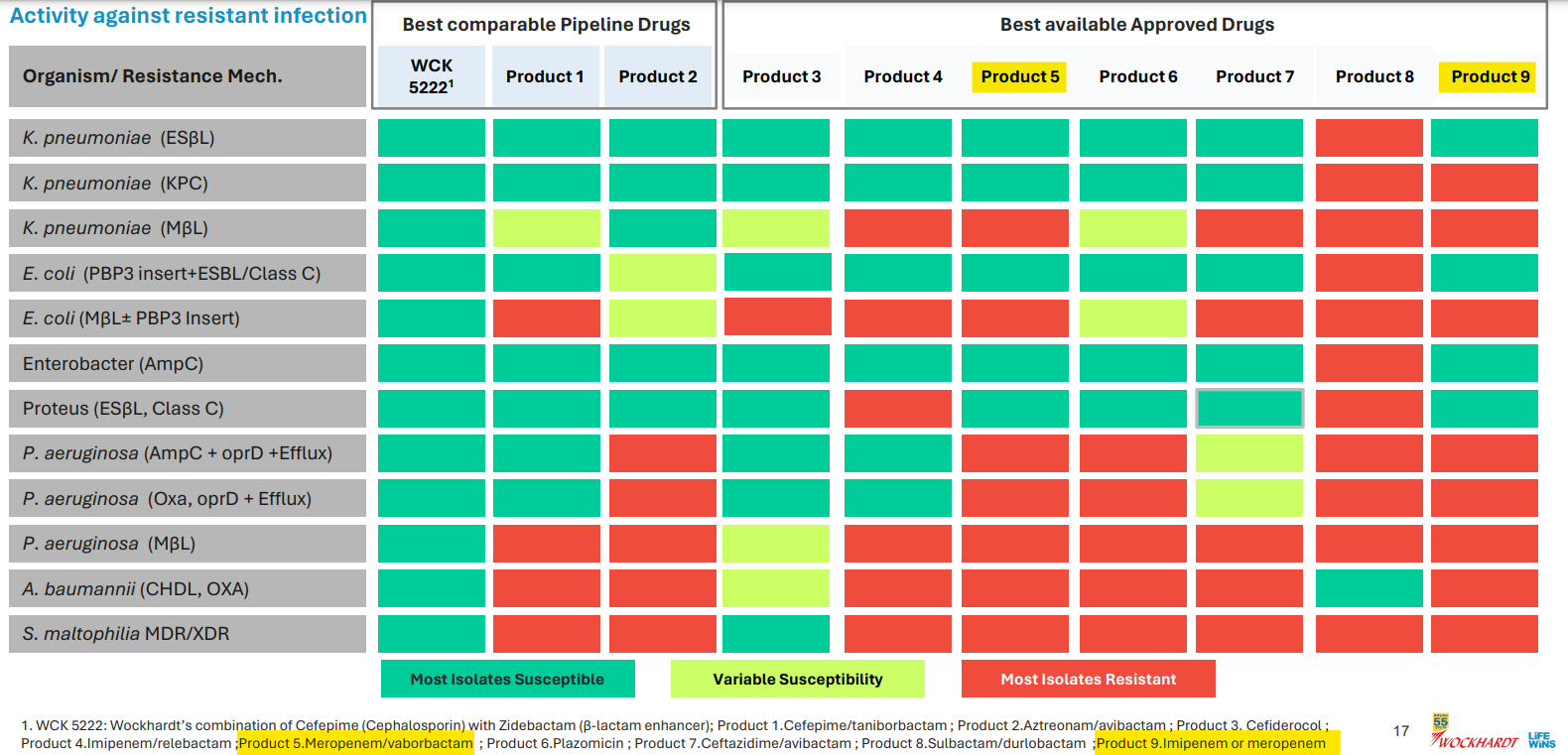

A slide from Wockhardt’s presentation lists the peers of WCK 5222 and Meropenem in isolation (Product 9) or in combination with Vaborbactam (Product 5) is a standard of care for some 4-5 high priority pathogens identified by WHO:

Orchid’s Enmetazobactam was tested against PipTaz but I feel both these drugs are inferior to WCK 5222 as they are narrow spectrum and will be used only in certain indications like ESBL:

Forget WCK 5222, I think Enmetazobactam and PipTaz are inferior to even Meropenem. Don’t know why Allecra made the strategic error in comparator selection. May be they only had preclinical data for Enmetazobactam in comparison to PipTaz which was presented to FDA. Ideally they should have used Meropenem as the comparator. Why do I say this? For carbapenem resistance pathogens, the line of action is:

1st line – PipTaz

2nd line – Meropenem

Last resort – Colistin

Colistin is toxic. So much that researchers are asked not to report Colistin as effective. So any new drug should compare itself with the 2nd line Meropenem. Otherwise, they can’t position as a drug comparable to any carbapenem. So it will have impact on uptake or peak revenues.

Why cUTI?

Any drug has to undergo 2 trials usually for the same indication. But US FDA was convinced of the safety of cefepime and zidebactam and allowed a single trial for phase 3 with half the number of patients (500 odd). US FDA wanted to expedite the process as the drug is for unmet need. One of the discussion points from the meeting with US FDA was that to expedite the availability of WCK 5222, initially, asked Wockhardt to take approval in cUTI. The main advantage of cUTI which no other indication offers is one can readily asses the microbiological cure of an antibiotic in a large number of patients which is not possible with pneumonia or blood stream. Any drug it is important to show that there is microbiological cure and clinical cure. Clinical cure can be assessed in all kinds of indication because the parameters are well understood by doctors. But clinical cure also can be subjective. To bring objectivity, US FDA wanted the trials in an indication where you can get strong data on microbiological cure. Microbiological cure is measured by pathogen isolation rate and it should be high in any indication. In blood stream, only 20% isolation is possible. In pneumonia, it is 30-40%. In UTI, the isolation rate is highest at nearly 80%. So it is easy to isolate the pathogen from urine sample than a blood sample.

Not just WCK 5222, many drugs in the last few years have been tested in cUTI.

Orchid’s Enmetazobactam was also tested in cUTI indication:

Ceftazidime Avibactam (which Gufic sells and Orchid makes) was approved in 2014 or 2015 for cUTI but is being used in the US for blood stream infections and pneumonia even though there was no clinical data available.

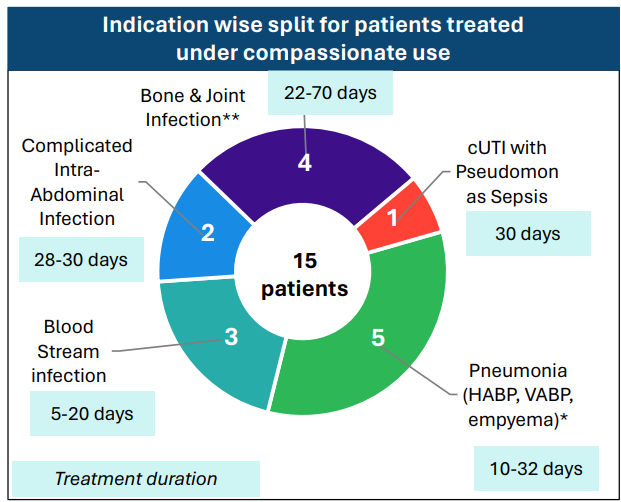

Even WCK 5222, in the 15 compassionate uses so far, was used for cUTI, Blood Stream, Intra-Abdominal, Pneumonia and the difficult to treat bone & joint infections:

So a drug will be used based on the spectrum and resistance coverage and WCK 5222 seems to have the widest spectrum of all drugs both available and in pipeline.

Wockhardt will anyway have another trial in pneumonia too for WCK 5222 which will happen post the fund raise maybe.

WCK 4873:

Why Moxifloxacin?

For Community Acquired Pneumonia indications, the line of action is:

Oral Cephalosporins are 1st line

Combination with Azithromycin or Erythromycin – 2nd line

Moxifloxacin or Levofloxacin – last line

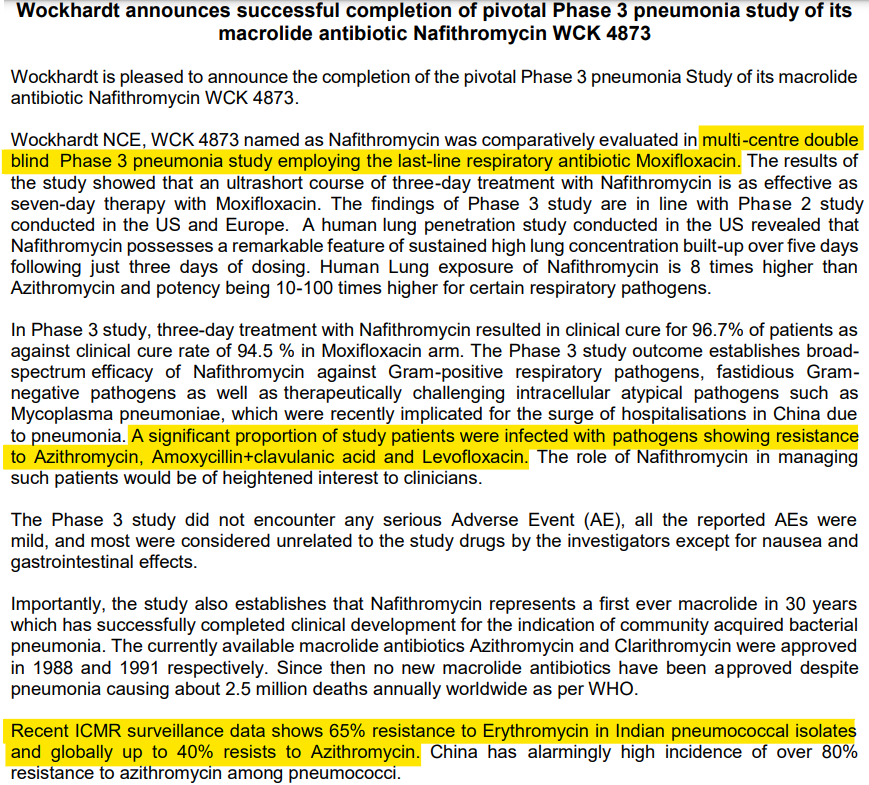

According to the press release from Wockhardt, pathogens were already showing resistance to Azithromycin, Amoxycillin+clavulanic acid and Levofloxacin.

Efficacy wise Moxifloxacin is the standard of care. It’s the go-to last resort drug, when nothing works. So using Azithromycin or Erythromycin as comparator would have been unethical.

Anyway, this phase 3 was not a global trial. Wockhardt did this so they could launch in ROW. For regulated markets, Wockhardt will do a global phase 3 trial for Nafithromycin.

Wockhardt did the best stress test of WCK 5222 and WCK 4873 by testing against the best options currently available – Meropenem and Moxifloxacin respectively. I dont understand why Mr. Aditya felt otherwise. Would love to get an explanation from him as to how the trial design should have been.

Sajal sir spoke about the past of Wockhardt which is available in public domain. Mr. Habil Khorakiwala talks about all these issues in his book –

https://amzn.eu/d/9EroHh9

In another video, he talks about – “Return on capital must be calculated, adjusting for the time-adjusted cost of capital (opportunity cost)”

https://x.com/unseenvalue/status/1767911729965486425?s=20

There are 2 levels of IRR:

- IRR of Wockhardt’s R&D investment – this will be in deep negative currently and should improve depending on how successful WCK 5222 and other NCEs are in future.

- IRR of Wockhardt’s investor – depends on when you bought the stock.

I have already explained in this post as to why the past doesn’t matter for an investor who has bought recently. If you bought in 2004, it matters. But we are in 2024. Market had written off all the R&D investments and was not assigning any value to the NCEs in pipeline when I bought.

I don’t understand why these experts dont go through the research papers or talk to doctors to understand the magic of WCK 5222 and Wockhardt’s R&D potential. Sajal sir does mention about Orchid and Wockhardt’s R&D team having the same origin. But I believe Wockhardt’s R&D team is superior because what Orchid developed – Enmetazobactam – is in a way a cousin of an older drug Tazobactam and hence a BLI Inhibitor in terms of action. What Wockhardt has developed – WCK 5222 – is a NOVEL drug as it exhibits unique BLE enhancer action. Novel ![]()

| Subscribe To Our Free Newsletter |