Q3 FY24 Update:

The discussion has been dormant. So kicking this off.

Chemical Sector:

The chemical sector across India has been suffering due to a downturn in the industry. The demand slump caused by inventory destocking, the Red Sea crisis, higher inflation worldwide and Europe’s issues added to the list of problems.

During this downturn, many chemical companies have taken the opportunity to scale up their operations and undergo Capex. Going through different chemical company reports, I can sense that the sector headwinds are almost over and demand recovery is foreseeable in FY25, as evidenced by larger diversified companies like Aarti Industries in their concall.

Company Q3 FY24 Update:

The effect of the recovery is yet to be seen in the quarterly reports. Sales figures are still on a downtrend with QoQ and YoY regrowth of -21% and -27% respectively. However, margins (OPM & NPM) are expanding. Overall, a dull quarter on the top line and flattish on the operating level and bottom line.

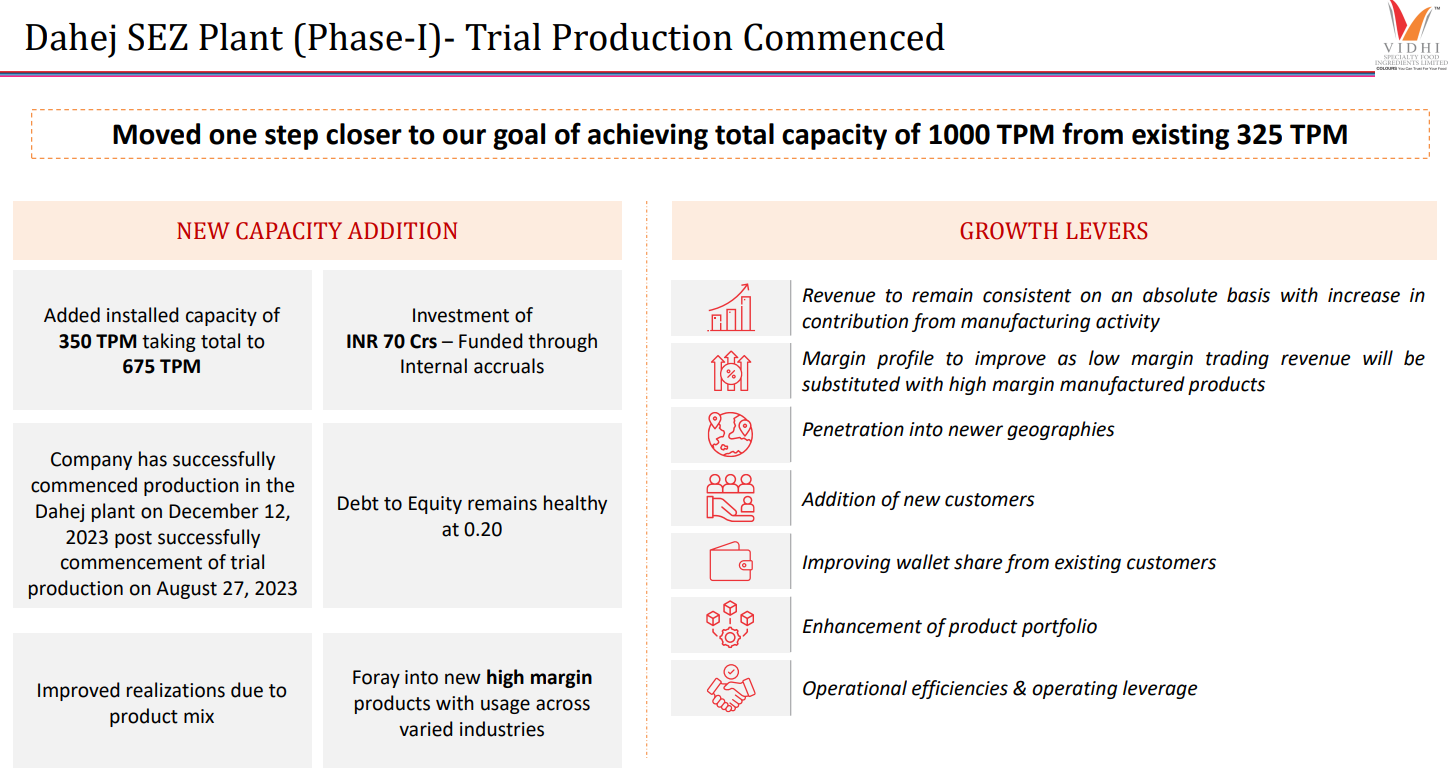

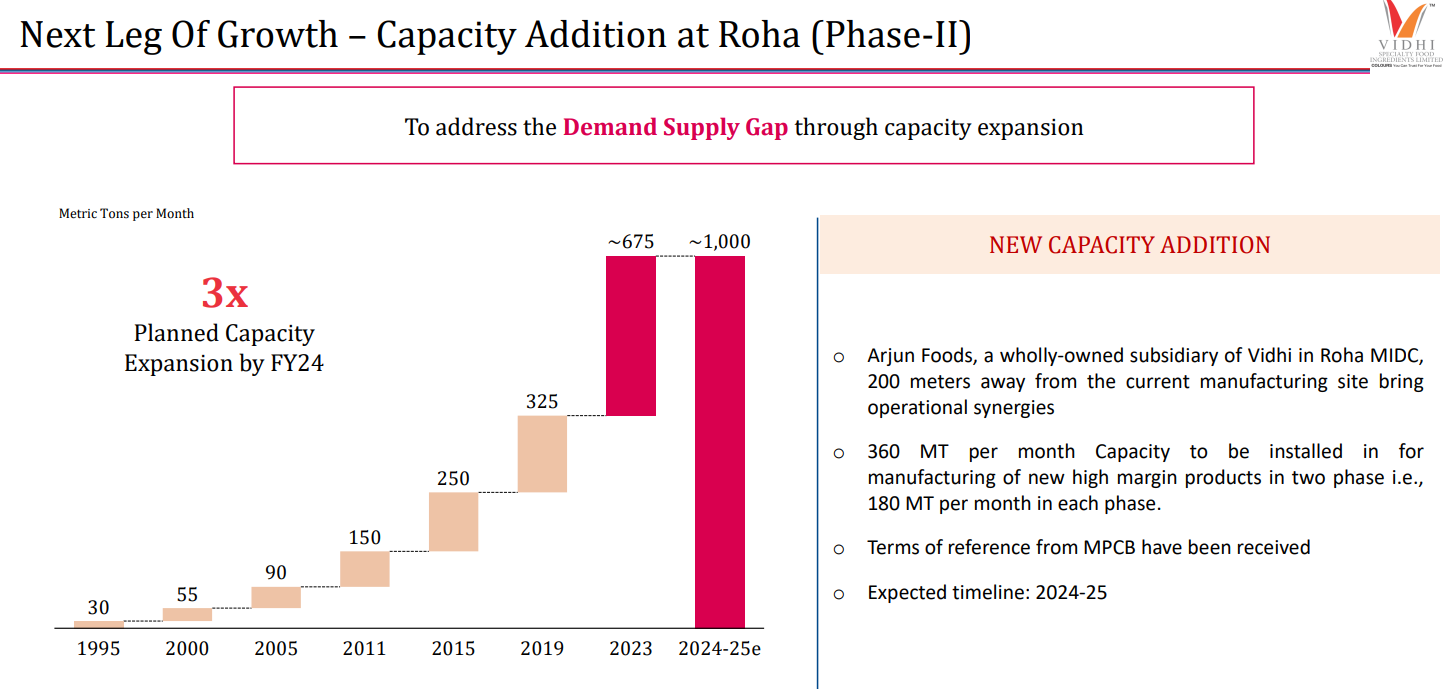

Growth Drivers: Expansion

Despite most chemical sectors facing deep cuts in their stock price, Vidhi has consolidated since Oct 21(Q2 FY22). This is most likely because of the future growth that the company is investing in.

The 1st Phase of the Capex has come online and should contribute to sales in the coming quarters.

The Global Food Colour Market (2021-2026) is expected to grow at a CAGR of 4.7% and the emerging food colour market is growing faster at 6%. Incremental demand to be expected Y-o-Y basis in the global food colour industry at 1500-1700 Crs.

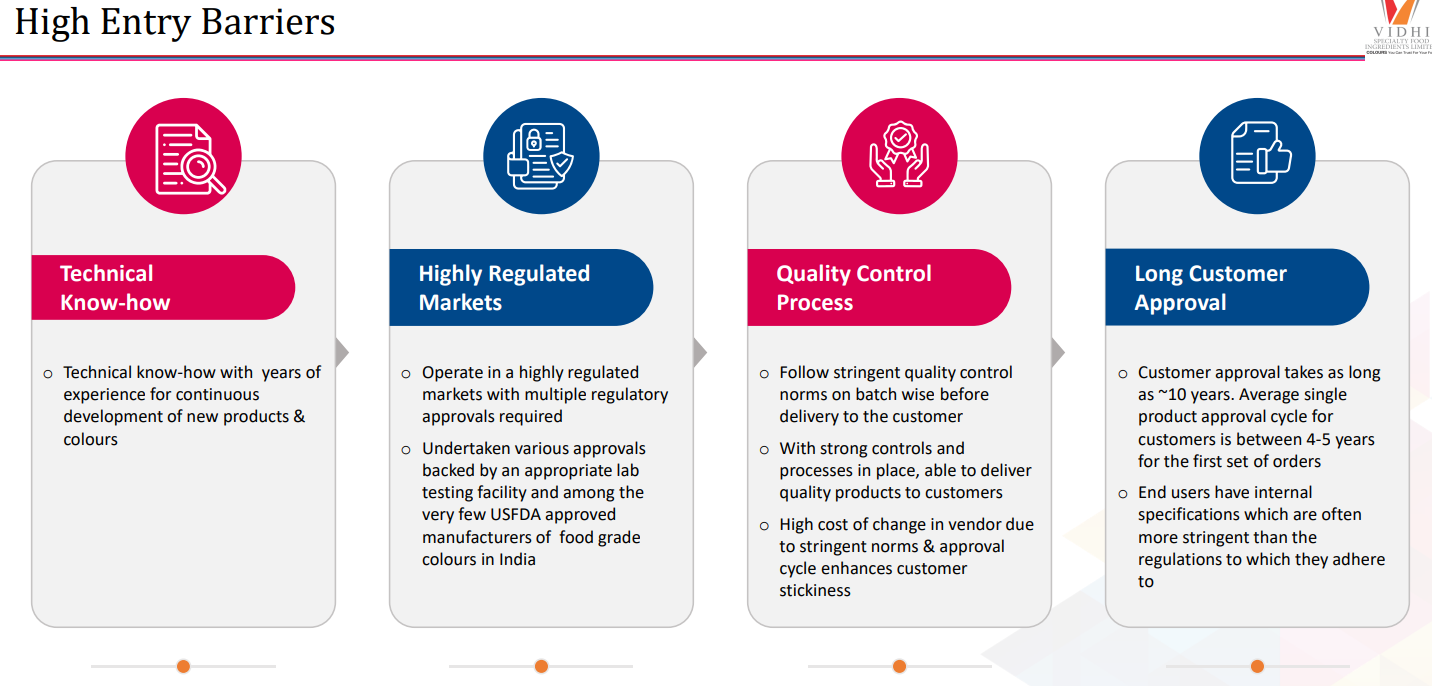

There’s limited competition with a few players: Camlin Fine and a few others who derive a small % of revenues from this business. There are high entry barriers in the food colour industry due to stringent compliance and approval timelines. It’s the 2nd Largest food colour manufacturer in Asia, with an existing Capacity of over 3,500 MT p.a. with ~8,500 MT p.a. under expansion.

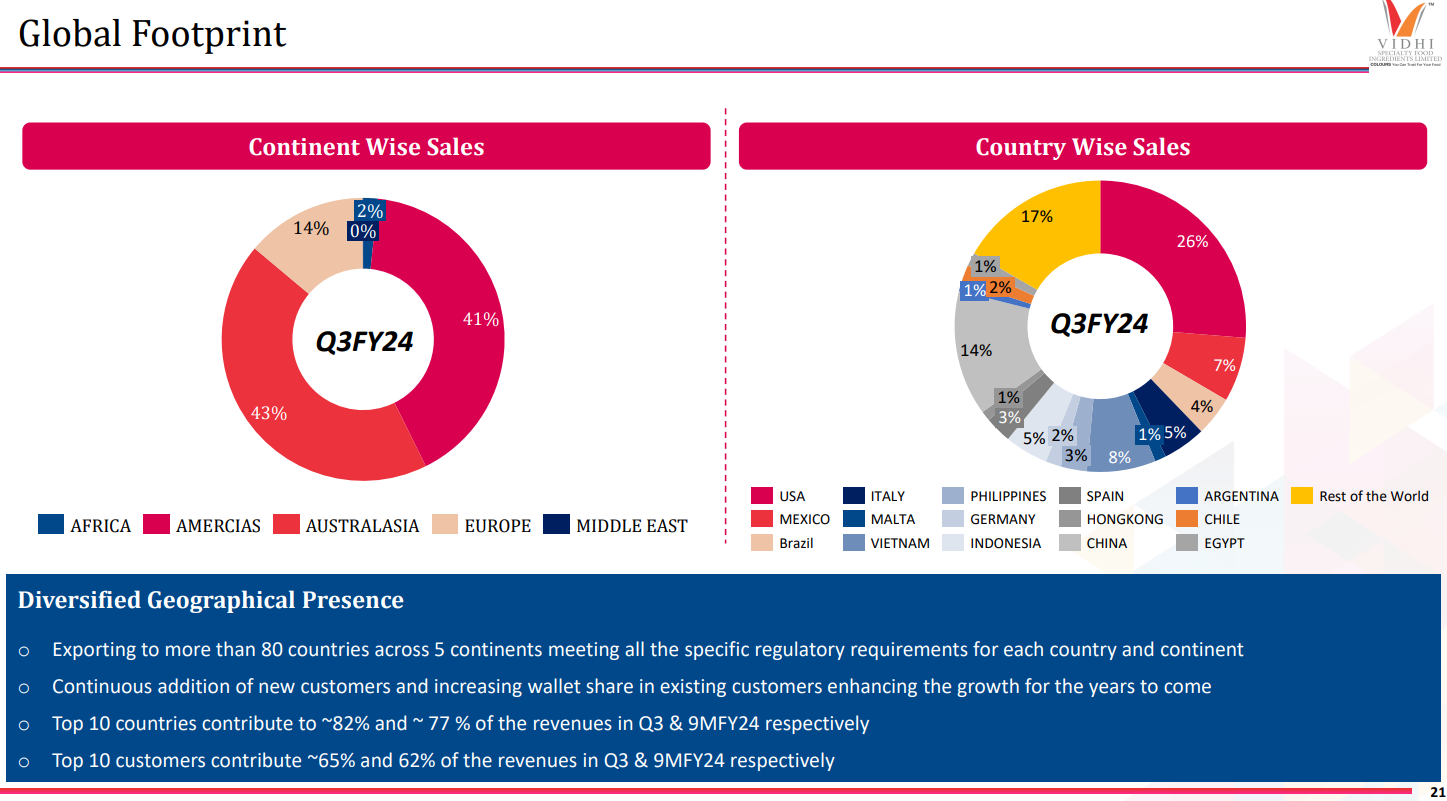

The company sales are 5% domestic & 95% export. Well diversified across geographies & client base and has a smaller portion of the portfolio exposed to Europe.

Expectations:

With no CWIP present on the balance sheet as of (March 2024, Q3 FY24), all capex of phase 1 has been operationalised. Assuming a Net Fixed Asset Turn(NFAT) of 8 (5 yr Avg) on 121 Crs of NFA gives me a sales jump of ~3x. A conservative 12% NPM gives a ~3.3x jump in earnings (PAT).

If valuations(P/B) rerate on the higher side returns will be more lucrative.

The stock has been sideways for a long time with good growth triggers for the upside.

Disc: Please do your own Research. Not a Buy/Sell recommendation. Have taken conservative figures for the calculation, so upside surprise has a higher probability.

| Subscribe To Our Free Newsletter |