Diamond power case study, they got the rp approved on 20 jun, 2022.

-

COC received and discussed the resolution plans on 13.11.2019, wherein the COC rejected both plans and passed a resolution to liquidate the Corporate Debtor.

- Patience is key in this style, one will get limited ideas here, where again it would take a long time for things to pan out. In the last few months following this space, i have only found 2 investable ideas here whereas i would be following close to 20-30 cases, waiting for them to pan out.

- No point in jumping on the news of resolution plans coming in, one needs to wait for NCLT approval at the least.

-

On 26.03.2018 the C.B.I. registered an FIR, against the MD and Joint MD of the Corporate Debtor, because it was noticed that a consortium of eleven Banks were cheated to the tune of Rs. 2654.40 Crores

- One of the biggest alpha comes out in following change, it can be seen how big of a change it could be if and when the mgmt changed, try to invert and think in all possible outcomes.

-

There was only one resolution applicant

- although i prefer if there are multiple RAs, it shows the value of that asset and thus the desire for it

- Although i also prefer a one time upfront payment clearing all dues (preferably without debt), the RA here had planned to pay 431cr deferred over 5yrs. Again its a debatable topic and varies from owner to owner as to how he prefers to use his funds, maybe we can perfect this as we understand multiple cases.

-

501cr for the whole cirp process and 300cr for capex and wc were to be paid by the RA

- Capex and wc funds are important to track as to understand how the operations will grow and be funded post-acquisition.

-

As per the approved resolution Plan there shall be no delisting of the scrip

- this is mentioned in every NCLT approval doc and needs to be checked

-

Resolution Plan submitted by GSEC Limited in consortium with Rakesh Shah

- Working on the acquirers one would have easily seen they do not have any background in this industry. This is a huge negative at first glance, but one needs to patiently keep following updates.

- And then these acquirers brought in an extremely strong and experienced professional mgmt to helm the operations

- A strong team helming the operations is a must and needs to be watched, its the top thesis pointer in this sort of a turnaround

- Its also important to understand that most of the times the old mgmt of the debtor continues at the helm as hired help for some time to smoothen out the start/integration, and thus non technocrat promoters may not matter much.

- the whole point here is to individually judge the capabilities of both, the acquirer and the business being acquired, and then calculate the risk to reward.

- sometimes there is nothing wrong in the underlying business its just that they are capital starved and once they get access to capital everything goes back to normal and the firm grows, thus i would like to again put emphasis on judging the acquirer and the business individually.

- Looking at the historical nos one could have seen what the company used to make pre 2015, and then understand where things went wrong for them. We can see what sort of asset expansion took place post 15, which was funded through debt, execution of their plan went haywire. I prefer such entities where there were huge numbers and brands before but due the errors/wrong steps/execution issues from the mgmt side crushes the entity’s health, thereby giving a huge opportunity to the informed.

-

According to the rp, share capital of the company shall stand reduced and extinguished to the extent of 99% such that shareholders holding less than 100 shares will not get any shares and their shares will be extinguished in full.

- This needs to be watched on, and from what i have understood till now is if one is to enter the scrip, it is to be post reduction only

-

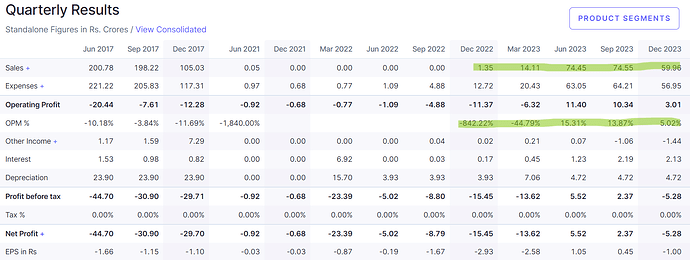

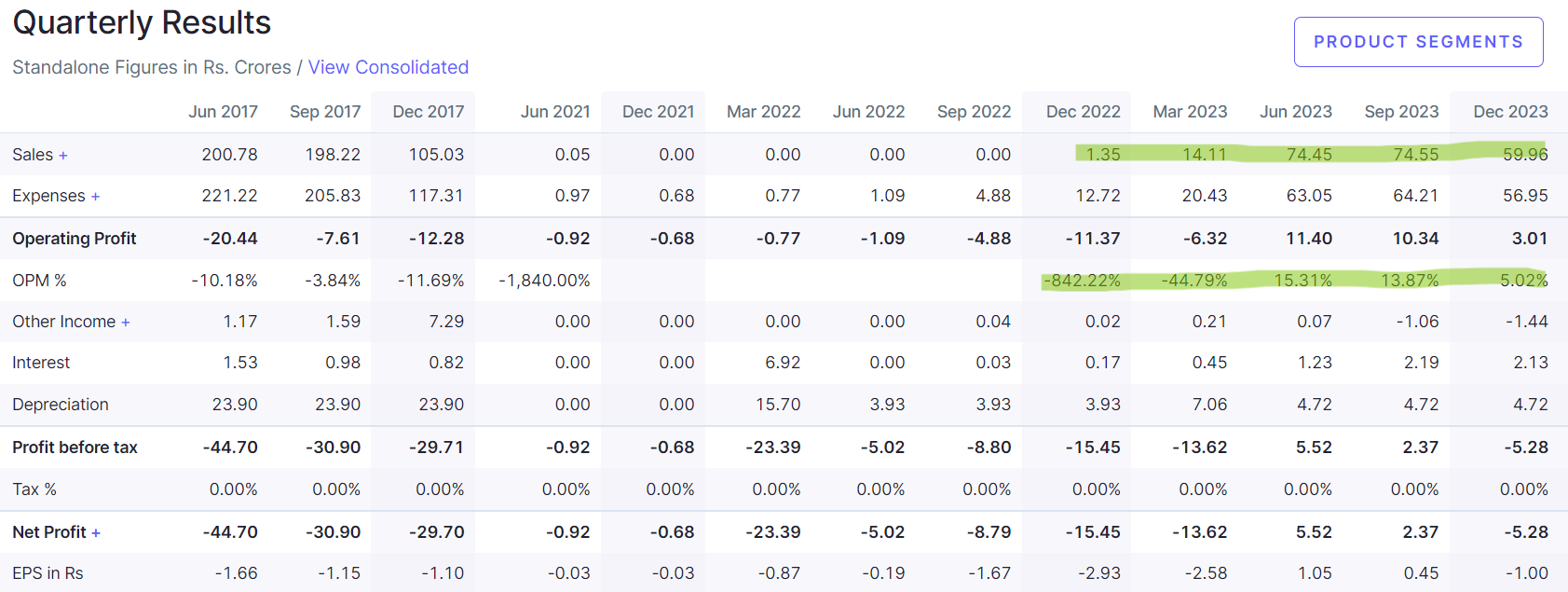

Numbers started improving from December quarter itself, attach the quarterly img

- Says a lot about the business and also in this case its acquirers.

- Says a lot about the business and also in this case its acquirers.

-

Hired Price Water house Cooper LLP (PwC) as Internal Auditor, one of the well known names

- These small things indicate the intent of the mgmt and needs to take up a significant space in the overall thesis

-

Within 4 mts of acquisition, they began commercial production at the inoperative plant

- few entities move very slow post mgmt change, minute data needs to be watched to understand mgmt aggression and overall plan, will share another case study which is currently playing out where the execution is pretty slow while the new mgmt has huge huge capabilities.

-

Orders started flowing in from april 2023, again proving the plans of the new mgmt.

To conclude, i would have added a significant part of my initial position as soon as the capital reduction was done, seeing the caliber of the professional mgmt (hired) alone, post that seeing the improvement in numbers i would have doubled the initial position, and then lastly kept on adding on the smaller updates like hiring PwC.

This is all in hindsight, but thats the whole point of it, to understand how to play these things.

The price move is a whole different thing and may have been due to several reasons and is sort of a one off, but the above points were key and them playing out solidifies ones thesis otherwise

Yes the current valuations may seem expensive but thats what ‘’change’’ does, looking for change leads to a lot of alpha, now thats a whole different thing that half of this alpha maybe due to unnecessary reasons but who are we to judge where that alpha comes from. PLAY THE ODDS AS THEY COME.

Not an investment suggestion.

| Subscribe To Our Free Newsletter |