ABB is a technology leader in electrification and automation, enabling a more sustainable and resource-efficient future. The company’s solutions connect engineering know-how and software to optimize how things are manufactured, moved, powered and operated.

Some of my assumptions are

-

Auto ancillary capex will remain high for next year as we are seeing a lot of supply chain shifts out of China, plus the demand in Indian markets are picking up drastically.

-

EMS capex will also remain high ( we import 5% of global EMS production and manufacture only 3% )

-

Infra / railways already have the tailwind

-

Renewables and datacenter capex is going on as usual. Renewables apparently take 7-8 times more electrical components compared to coal /gas based plants

I think ABB is best suited to benefit from some of the tailwinds ( but I am not able to gauge the upside. Chart was strong during the sell off days in march 2024 ). Their presence is across the segment and is winning orders in the datacenter, railways and electronics automation space. The float is also very low.

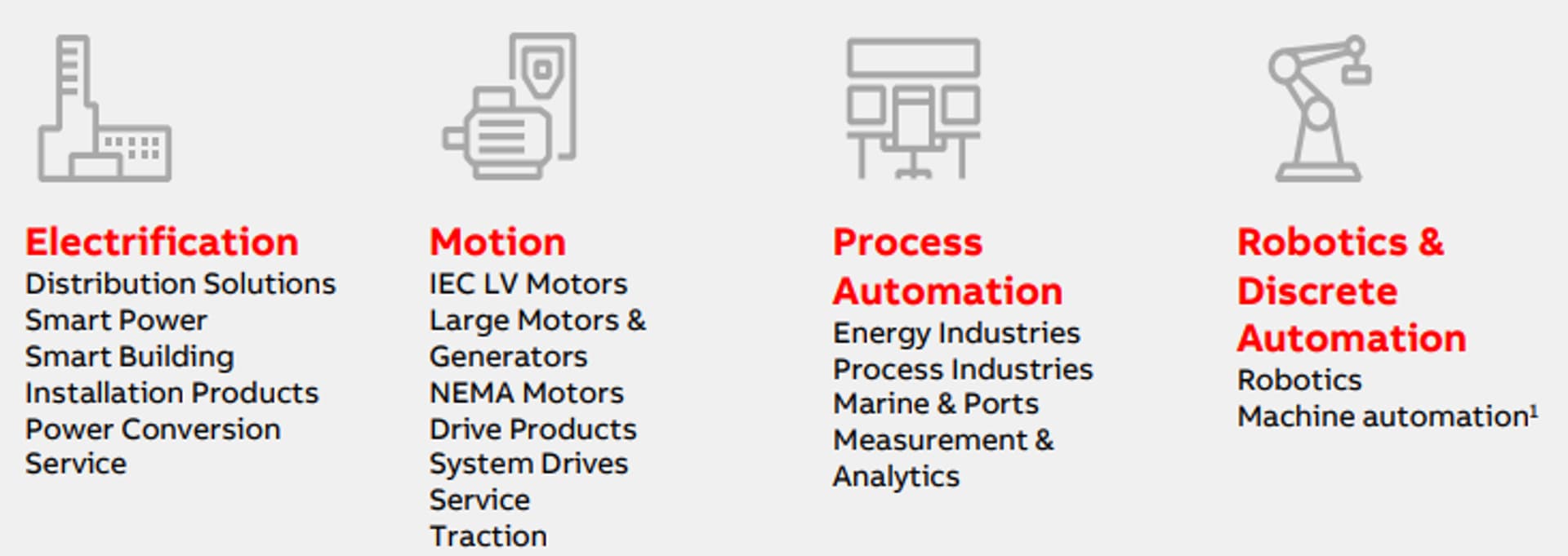

The 4 main verticals of the industry.

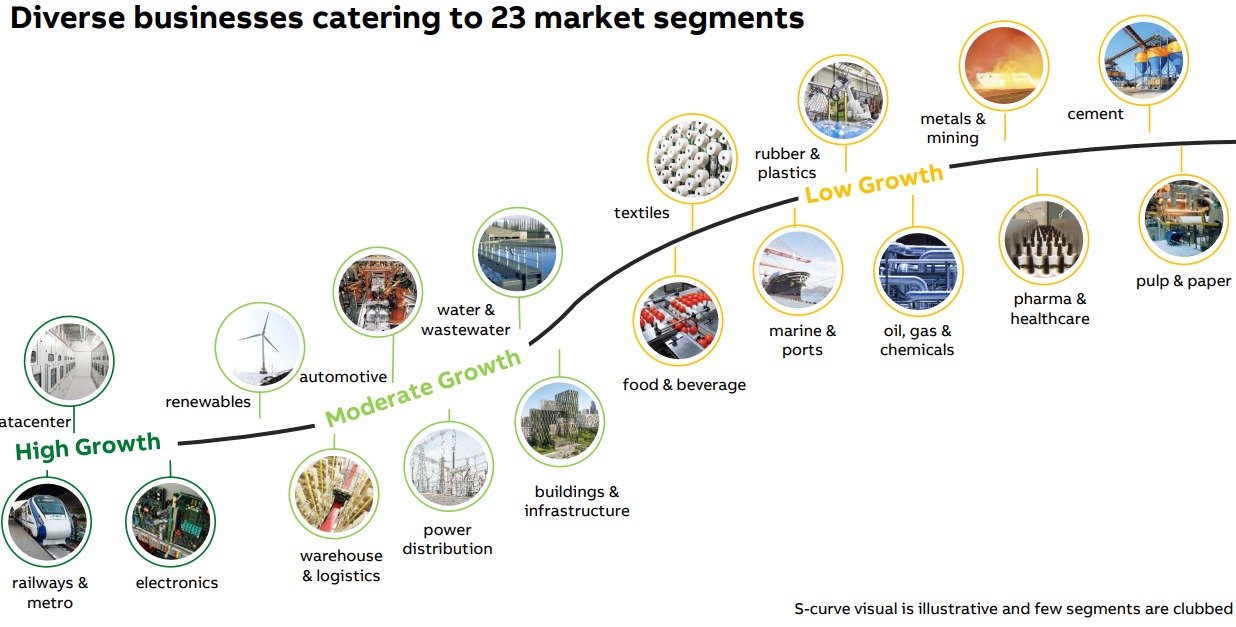

as per management 50% of the new orders are from the high growth segments, Moderate growth segments have lumpy orders and Low growth segments if order comes can be very large as they belong to heavy capex industry.

ABB benefits from India’s large shift to renewables which is probably a decadal tailwind.

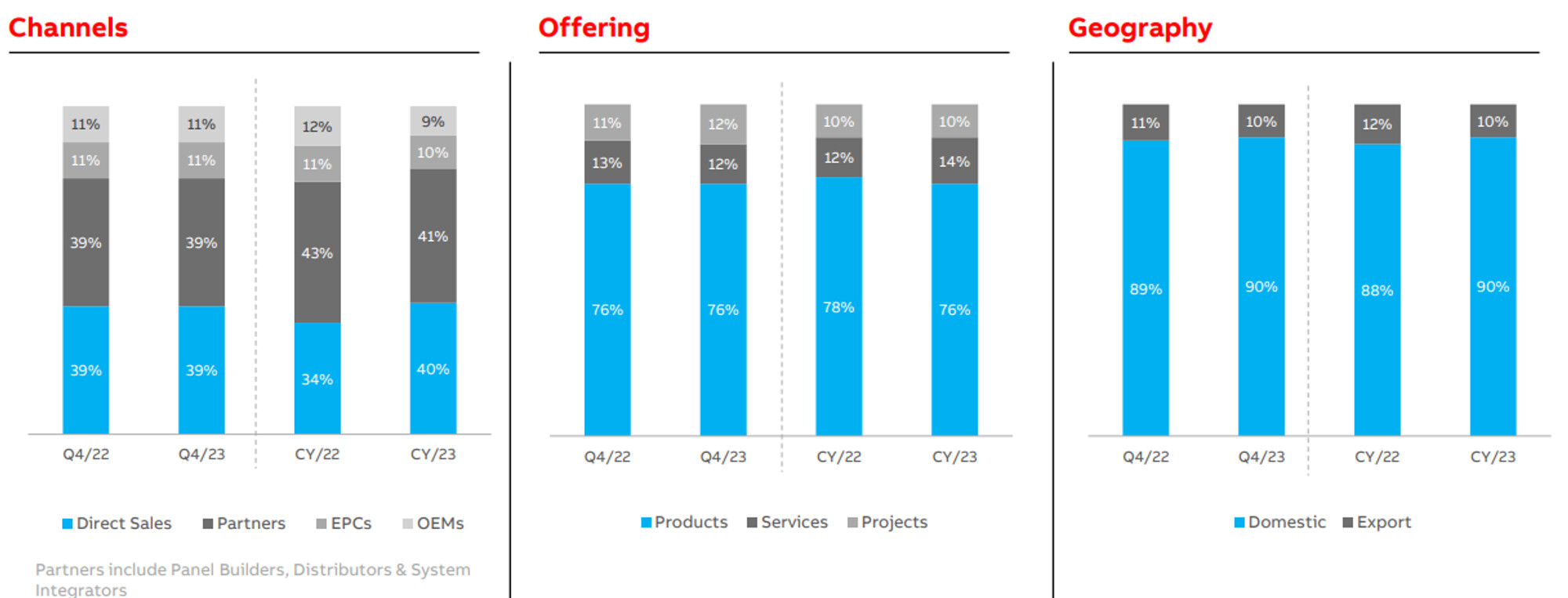

Their revenue comes from projects, services and products, product orders are executed within 6 to 9 months and project orders can get executed anywhere between 12-18 months. As the execution of large orderbooks go, the demand for services might increase as a % of the overall revenue. Also exports as a % might also pick up as ABB India becomes more competitive vs global peers and the demand for grid rewiring / renewables pick up across the globe. However these will take anywhere between 3-5 years in my view.

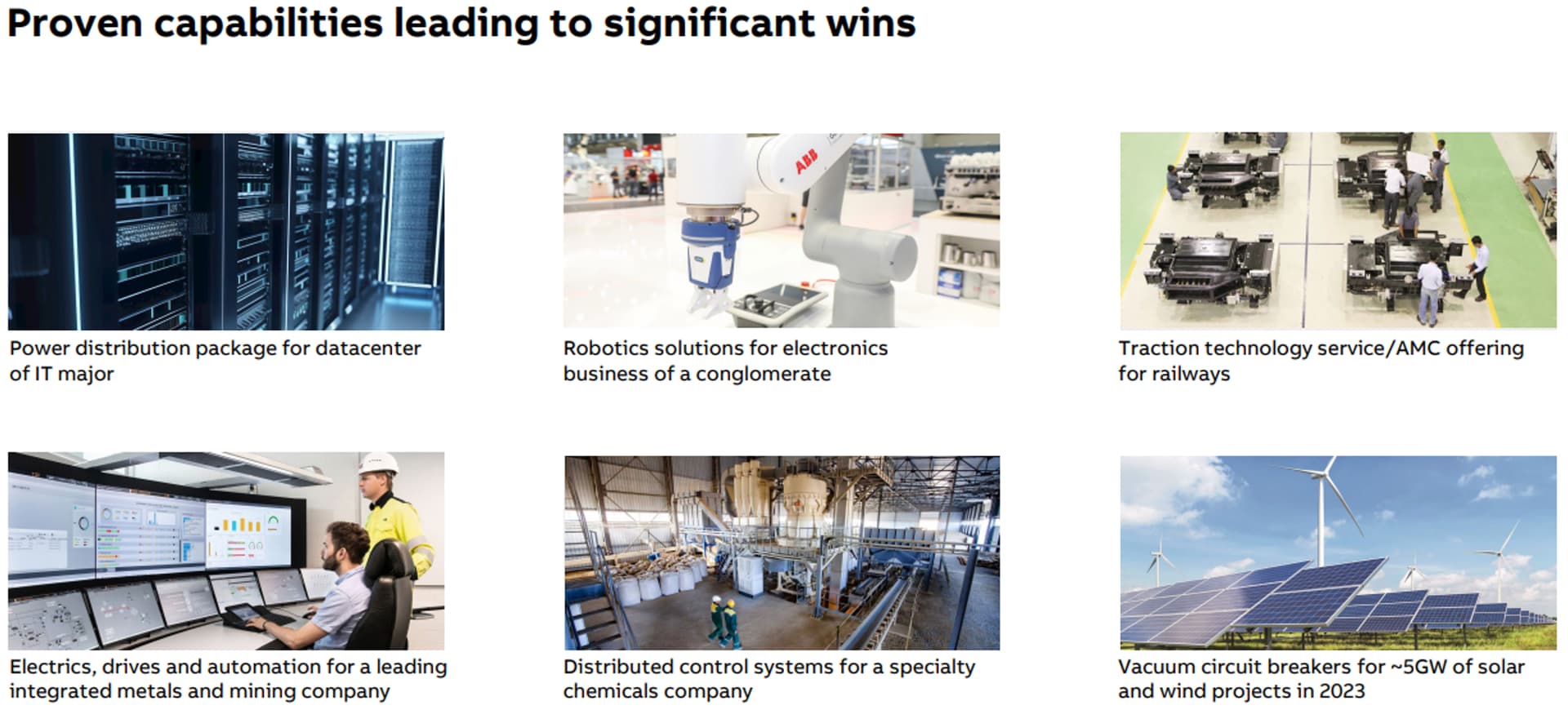

This is one of my most favorite slide form their presentation where they show their products in high growth sunshine sectors such as datacenters and EMS manufacturing companies. We will see them get significant orders from these industries soon.

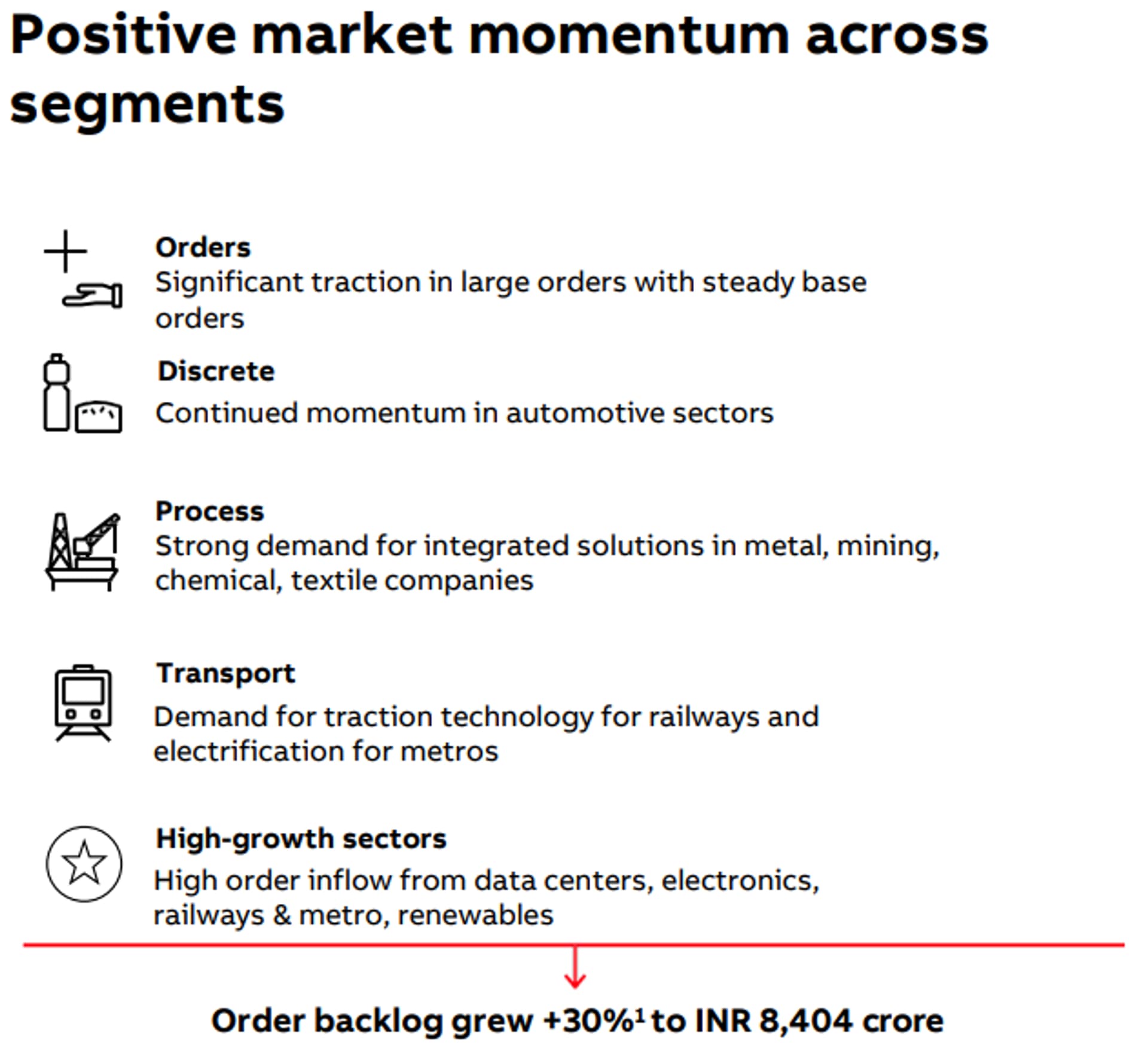

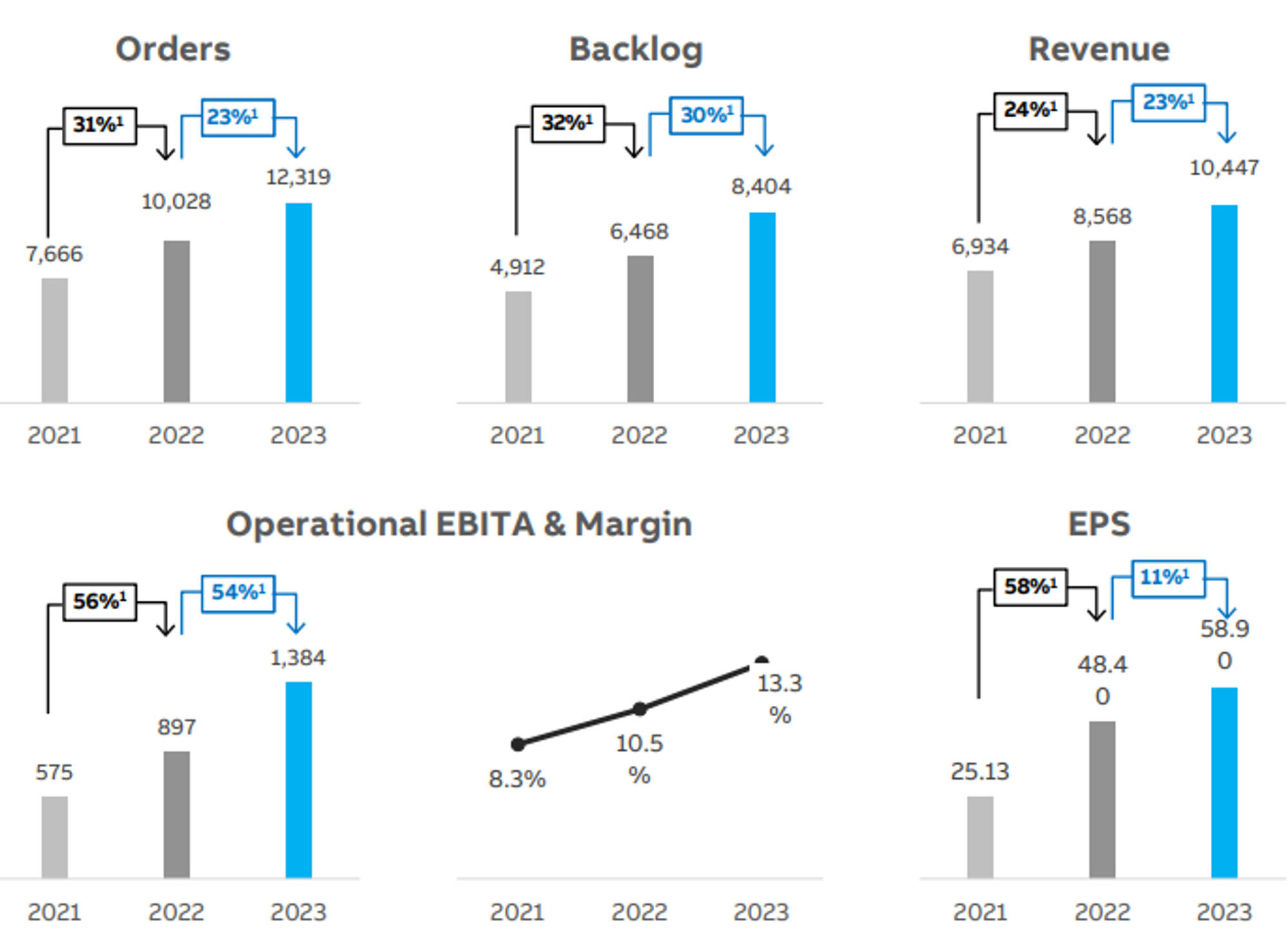

I think this slide shows their Order book and the backlog, expecting that orders too keep coming for FY 25 , as it takes them 12-18 months to execute their projects and 6-9 months to execute their products., I see their revenue almost doubling by FY25-26. A second optionality may occur if large orders come from the low growth but high capex intensive businesses like cements / mining etc. we will see a substantial jump.

Disclaimer – No holding in the stock, studying it.

| Subscribe To Our Free Newsletter |