Pricol

Sector: Auto Ancillary

- Pricol is a manufacturer of automotive components for the Indian as well as international markets.

- It manufactures auto components for two/three/four wheelers, commercial vehicles, tractors, off-road vehicles and Industrial tooling segments across the global market.

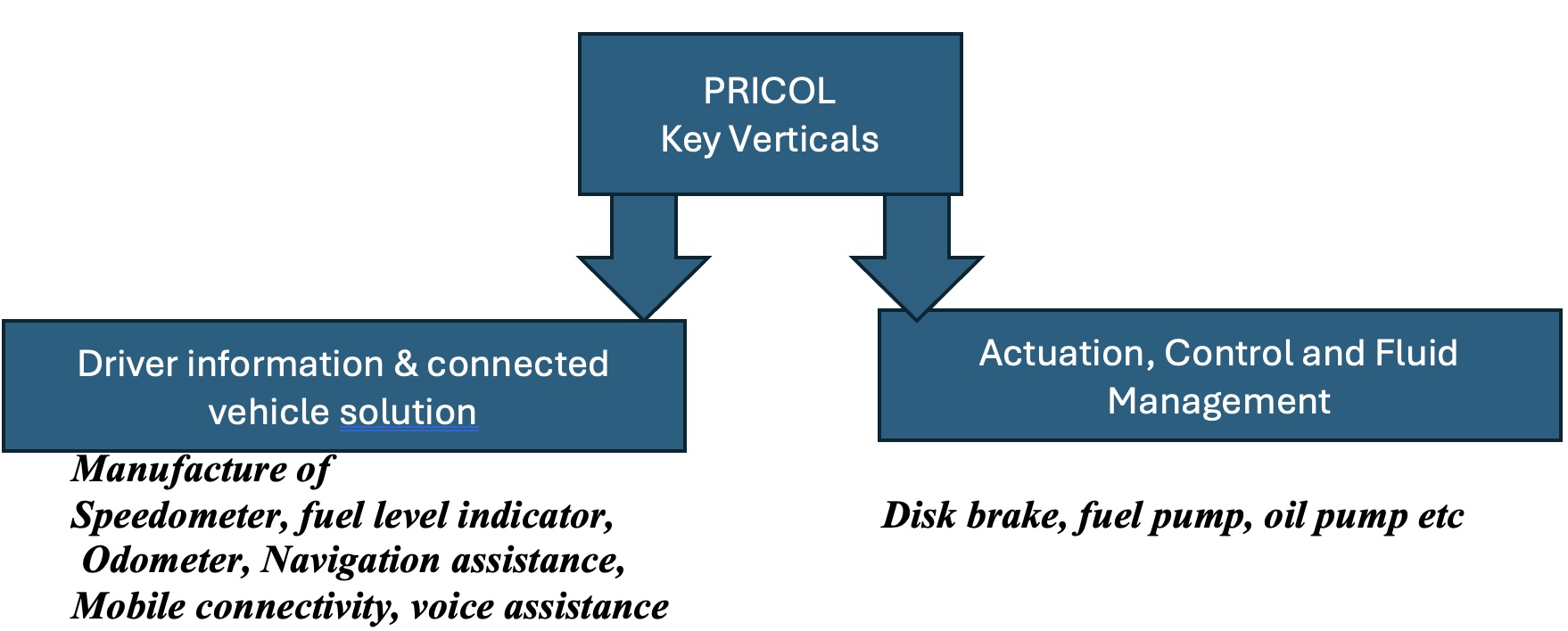

- Driver Information Systems, Telematics and Pumps & Mechanical products are the key revenue earners for the company

- across India and in International Markets (45+countries) with 2000+ product variant

- Pricol ranks as the second-largest manufacturer globally for instrument clusters designed for 2/3 wheeler applications. It holds a substantial market share of 50%/ 70%/ 50%/ 90%/7% in the 2 wheeler/ commercial vehicles/ tractors/ off-road vehicle segments/ passenger vehicles respectively, establishing itself as a key player in the industry.

- Pricol launched new EV-ready products like Heads Up Display (HUD), E-cockpit, Disc Brake, Round TFT Instrument Cluster, TFT Smart Clusters, Electric Coolant Pump, etc. at the Auto Expo 2023

- The company operates 9 manufacturing facilities across India and 1 in Indonesia. Its plants are located in Coimbatore, Chennai, Pune, New Delhi & Pantnagar (Uttarakhand)

- Company has 2 technology centres

- Has entered into 5 strategic partnerships

LCD->TFT

- Pricol has manufacturing capabilities for producing ~30,000-40,000 clusters per day on an average. It stands as a major supplier of telematics solutions within the Off-Road Vehicle (ORV) and tractor segments. It has successfully designed and manufactured more than 3,00,000 telematics till date.

Driver Information System (DIS) is used to indicate the instantaneous changing parameters in the vehicle such as speed, engine RPM, engine temperature, fuel level, fuel economy, service reminder, phone connect, navigation assist and various warning indicators at vehicle level.

Strategic Partnerships:

-

In Feb 2022, The Co. entered into a strategic technology partnership with Sibros Technologies Inc., a California-based co. providing Over-the-Air (OTA) connected vehicle software systems for OEMs worldwide, to deliver deep-connected vehicle solutions in the Indian and ASEAN markets.

- In FY23, Pricol Telematics Control Unit (TCU) with SIBROS Software was installed & successfully running in 2 Wheeler, ORV & CV vehicles on the domestic and international customer side

- The telematics market in India is estimated to be USD 1.3 billion in 2023 and is projected to reach USD 2.7 billion by 2028, with a CAGR of 15.5%

-

In 2023 Pricol Ltd announced a partnership with China-based Heilongjiang Tianyouwei Electronics for Driver Information System (DIS), including e-cockpit, heads up display, for vehicle segments.

- Pricol is currently involved in the development of an E-Cockpit in collaboration with a major customer. The start of production (SOP) is anticipated in FY26.

-

In 2021, Pricol Limited, came into a strategic partnership with Candera, a leading Human-Machine Interface (HMI) tool provider and development partner for worldwide automotive and industrial customers. This technology partnership with Candera will bring global HMI solutions into Pricol’s range of Next Generation Connected Driver Information System (DIS) products serving across all vehicle segments.

-

In 2022, Pricol in partnership with PSG Institutions has launched a Center of Excellence (CoE) to develop high efficiency micro motors and Robotics and artificial Intelligence based processes and equipment.

-

In 2022, Pricol has entered into a partnership with BMS PowerSafe, a part of Startec Group, to manufacture and sell Battery Management System (BMS) for Indian Market. BMS PowerSafe is recognized as the top 3 pure players of BMS suppliers in Europe.

- In this partnership, Pricol will be licensing the product and process technology of BMS from Partner company and will be manufacturing complete BMS in-house locally in India. This partnership has opened up a new arena for Pricol to add a pure play EV product in our portfolio.

- As of now, no orders have been secured for BMS. Foray into BMS is an effort to strengthen EV-related offerings.

Capex:

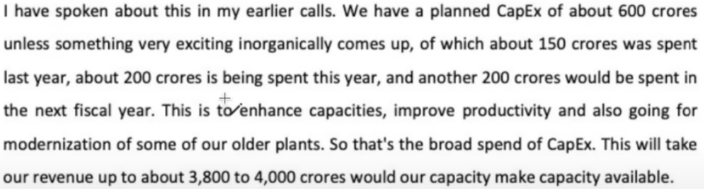

Pricol has a planned capex activity for Rs. 600 crore from fiscal 2023 to fiscal 2025 to enhance capacity( from Internal accurals), mainly of new products, which are part of the productivity linked incentive (PLI) scheme and also for routine modernization and refurbishment of lines.

- During fiscal 2024, company is expected to spend ~Rs. 140 crore for a new plant in Pune and ~Rs.50 crore for maintenance capex and so far ~Rs.80 crore was spent during the current fiscal.

- Capex for next fiscal is ~Rs. 120 crore, while ~Rs.200 crore will be reserved for any potential inorganic expansions

- With steady accruals and control over working capital and capex being funded through internal accruals, debt levels are expected to remain low, leading to healthy debt metrics over the medium term.

Concall Highlight

Revenue Breakup

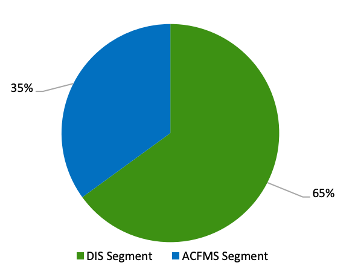

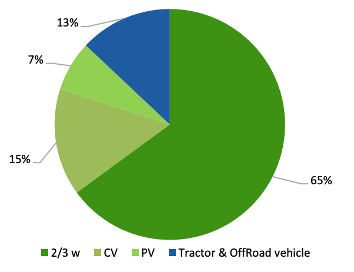

• 65-70% from driver information systems and connected vehicle solutions(DISCVS). 30-35% from actuation, control and fluid management systems(ACFMS).

DISCVS

• ~60% from 2 wheelers, ~35% from commercial and offroad vehicle, balance from passenger vehicle

Market Growth

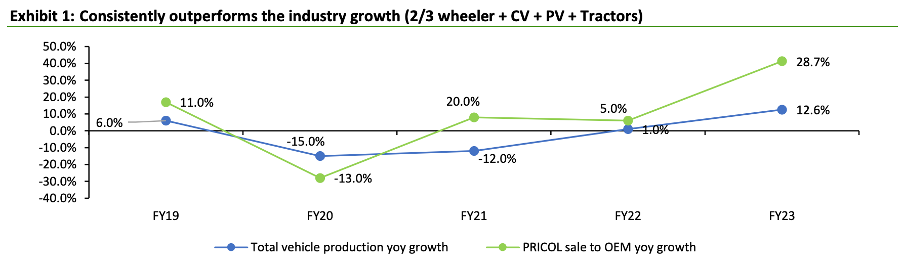

Driver Information System (DIS) segment to grow at a CAGR of 27% over FY23-26E

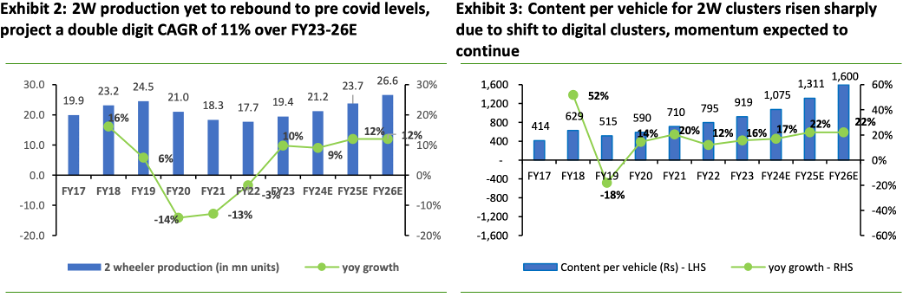

- Premiumization: Transition from mechanical to digital clusters. Further, the share of TFT clusters in the digital clusters to improve from 10% now to 20% by FY26E.

- 2W production surpassing the pre-covid levels and growing at CAGR of 11% over FY23-26E.

- Faster electric vehicles penetration in 2 wheeler and passanger vehicles segment.

- Growing presence in the passenger vehicles space.

Actuation Control Fluid Management System segment to grow at a CAGR of 12% over FY23-26E

Fundamentals

Market cap = 4,746cr (>1000 cr)

PE = 36.8 < 33.26 industry PE)

PEG = 1.07 (should be < 1)

ROCE = 20.1

ROE = 18.3

D/E = 0.12 ( should be < 1)

CMP/BV = 5.99 ( should be < 1)

CAGR sales growth 3 yrs = 16%

CAGR profit growth 3 yrs = 47%

EV/EBITDA = 18.17 (which is > 10)

Operating margins = 12%

Pricol’s net debt/equity level has always stayed low – below 1x – due to its efficient cash flow generation and timely repayment of debt.

• The rise in debt in FY20 was mainly due to high capex in the previous 2 years followed by low cash flow generation (semiconductor shortage issues). However, this was repaid quickly starting next year.

• CAPEX funded by internal accurals

Total reserves increased = YES

Total borrowings decreased = YES

Total fixed assets increased = YES

Cash flow from Operations in Last 3 years (Positive + sequential growth ) = YES

Net Cash flow for last 3 years (Positive + sequential growth) = YES

Debtor days – reduced from 56 to 50

Inventory days – reduced from 81 to 72

Days payable – reduced from 92 to 75

Cash conversion cycle – reduced from 45 to 47

Working capital days – slight decrease from 24 to 23

Financial risk profile is healthy with low debt levels and nil debt funded capex plans over medium term

FII holding – 6.50%

DII holding – 6.92%

FII shareholding increased in Dec month by 2.54%

DII shareholding increased in June month by 1.33%

Public Holding- 17.78 % is private entity out of 48%

Investment Rationale

- Premiumization – Rising content per vehicle, more in 2W and PV industry

- Instrument Cluster is a critical component of an automobile showcasing various real time information with respect to vehicle running parameters. Pricol is one of the industry leaders in this space with ~50% market share in the 2-W category, ~80% in CV’s, ~50% in tractor space, ~90% in off-highway segment.

- Cost of driver information system changed from 300 rs to 1200 rs and can change to 2500 rs in next 3 years

- Pricol realises ~70% of its sales from this segment.

- Pricol realises healthy ~30% of its topline from actuation and fluid control space including fuel pumps which have both automotive as well as industrial usage.

- Fuel pumps run the EV risk at Pricol and constitute ~5-6% of its sales, the company however is mitigating this risk by introduction of new products such as electric coolant pumps (used in Electric Vehicles)

- ACFMS segment to drive exports and improve EV exposure:

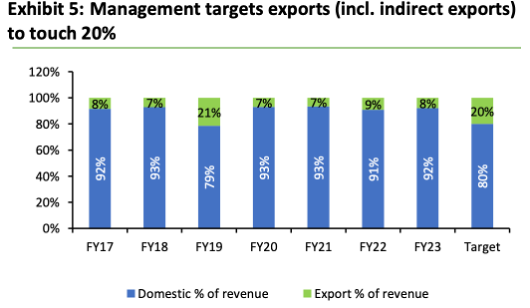

- ACFMS segment contributes 90% of total exports. While the company targets 20% exports as against ~8% currently, the current traction from customers such as Caterpillar, Polaris, KTM, Ducati, Harley Davidson, and BMW, should maintain export at 10-12% of total revenues in the near term.

- Caterpillar is a key export account for Pricol, and it is anticipated substantial growth in the next 2 to 3 years

- Pricol has ventured into the personal passenger vehicle segment to facilitate significant exports for the next generation of oil pumps to one of the largest manufacturers in Europe.

- Has a 20% export target in long term , should be able to sustain 10-12%

- Rebound in 2W production to continue in FY25 and FY26

- Sales breakdown for TFT: 8 out of 10 two-wheelers supplied by Pricol, four-wheeler presence in TFT is limited

- MoUs signed with BMS PowerSafe, Sibros, and TYW for future collaborations and revenue generation by FY26

- Opportunities in new segments/product – Battery management system , Ecockpit display, telematics , disc brakes, coolant pumps ,HMI interface to be rolled out in FY25Q4, FY26

- Expecting revenue growth from new products like battery management system and disc brakes starting from FY’26

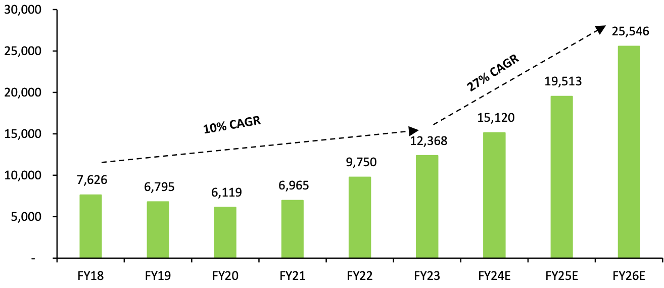

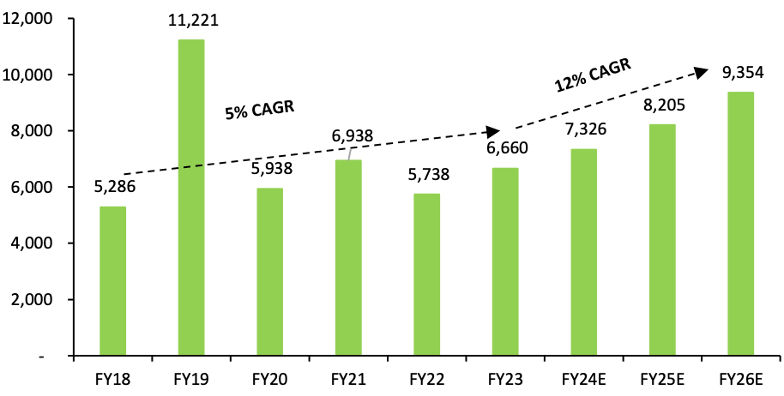

- Guidance of 4000 crore by FY26, Currently sales is 2000+ crore

- 3600 organic growth, 400 inorganic growth

- Note: This is a conservative growth

- Already have confirmed LOI with visibility of 3600 crore

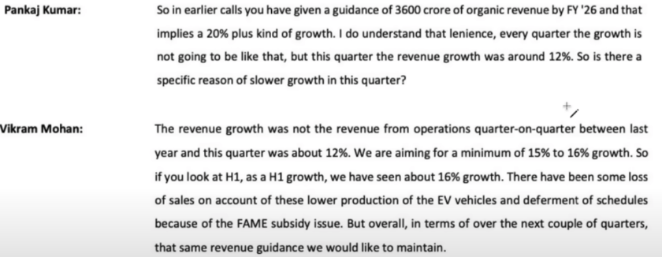

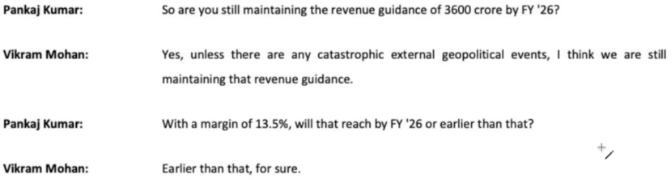

Q2 concall

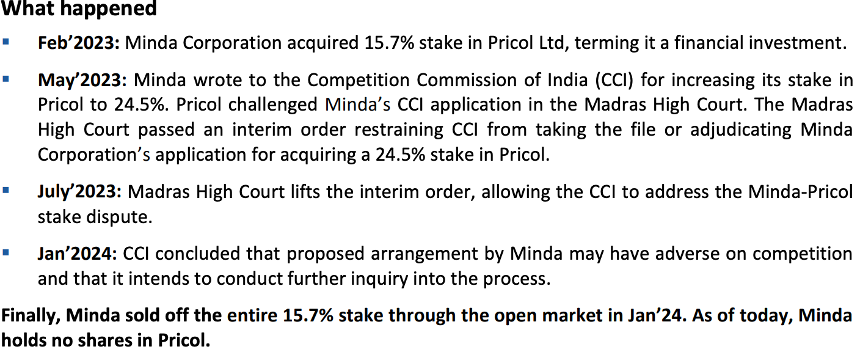

- Minda Corp

Minda’s investment in its competitor Pricolserves as a testament to Pricol’sleadership and technological prowess in the industry.

-

PLI scheme:

-

With an earmarked budget of $3.5 billion (or Rs 25,938 crore) for the automotive sector, is designed to offer financial incentives of up to 18%, fostering the growth of domestic manufacturing in Advanced Automotive Technology (AAT) products and encouraging investments throughout the automotive manufacturing value chain.

-

Pricol has been approved by the Ministry of Heavy Industries (MHI) for participation in the Component Champion Incentive scheme. Within the ambit of this PLI initiative, a total of 95 applicants have received approval, with 20 recognized as Champion OEM and 75 as Component Champion.

-

Await further clarification regarding qualifying products, capex and timeline for the same. Will be using CAPEX for same

-

-

Addition of customers and products – diversification to non-automotive business. As part of a strategic move to reduce reliance on the cyclical automotive sector, Pricol is actively exploring entry into the industrial instrumentation segment

-

The management has indicated an estimated capital allocation of Rs 2bn for a potential acquisition, signalling the company’s readiness to invest in strategic targets if identified.

-

While the management has not announced any acquisition yet, this would reduce the dependence on the cyclical automotive sector and bring uptick to the margins along with robust revenues, considering the strong technological expertise and R&D capabilities that Pricol possesses.

-

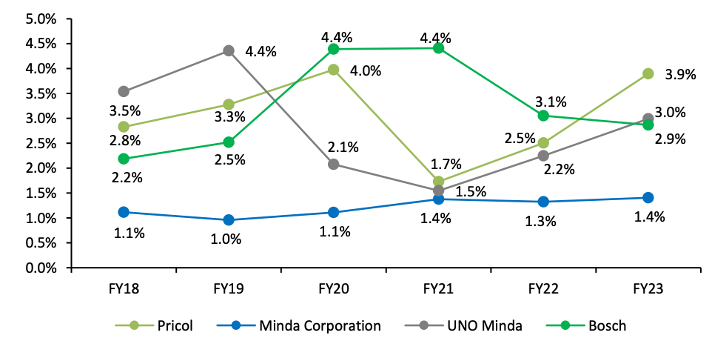

Pricol’s R&D expense as a % of standalone revenues stands tall versus competitors like Minda Corporation & UNO Minda, and is comparable with Bosch. Going forward, we expect R&D as a % of sales to remain in the range of 4-4.5%, showcasing Pricol’s commitment to fostering innovation for growth across all product development functions.

-

The introduction of BS-VI emission standards starting April 2020 spurred the trend from mechanical to digital instrument clusters, which are technologically advanced and command a higher content per vehicle. Pricol was quick to embrace BS-VI standards and secured numerous new business across various segments, leading to ~40% of the overall revenue for FY2020-21 contributed by these new business acquisitions.

-

R&D expense as a % of standalone revenue stands at 3.9% as on FY23

• Pricol’s business was facing multiple headwinds in the form of increase in freight cost due to the Red Sea issue and integrated circuit (IC) shortages

- Amidst a gradual improvement in the supply situation, IC prices continue to remain high. Pricol has supply arrangements in place with multiple IC suppliers. Pricol is actively engaged in negotiations with suppliers for price reduction, while ongoing discussions with customers are being conducted regarding compensation of the premium prices.

- Easing freight cost and semiconductor availability over next 2-years.

Key Risks

- Slow adoption of EV/Auto Sector: Further delay in ramp-up of charging infrastructure, high capital cost and dwindling incentives for EV adoption may slow down domestic growth.

- FAME 2 Subsidies To End on 31 March; EV Prices Likely To Increase Drastically

- Prices of some of the electric scooters and motorcycles are likely to go up by close to 25 per cent, which makes these products quite expensive compared to ICE two-wheelers.

- If there’s no more subsidy support from the government, there will be a drop in overall sales of EVs due to the increased price tag.

This drop in sales could go on for a few months, till the brands find a way to package their EVs to make it more attractive

- Delay in spending the committed capex and ramping up the capacities commissioned: Delay in spending of the Rs6bn capex and ramping up the capacities represents a key risk to the topline and bottomline.

- Disruption in supply chain and semiconductor issue: Disruption of supply chain represents a risk to the topline. Continuance of premium pricing of IC chips and elevated freight costs are a risk to margins. Note:

Raw materials is about 70% of companies expense - Delay in new product launches and discontinuation of models by the OEMs: Delay in new product launches like electric coolant pumps, electrical oil pumps, BMS, disc brakes, ecockpit, heads up display and telematics represents a key risk. Further, discontinuation of models by OEMs will hamper the business.

- Slowdown in premiumization: Slowdown in premiumisation would mean downside risk to our content per vehicle estimates, in turn slowing down the overall revenue growth.

- Doesn’t look like something happening in near future.

- High import dependence rendering profitability vulnerable to adverse forex movements: Pricol presently imports about 45-50% of its raw materials as compared to ~40% imports earlier, which was primarily driven by increased imports in the TFT segment. Out of the same, ~65-70% of the same are from China while other import sources include South Korea and Taiwan. All imports are routed through its subsidiary in Singapore, Pricol Asia Pte Ltd.

- The high import content in its raw material mix and limited hedging activity by the company exposes the company’s profitability to foreign currency fluctuations and freight costs, especially during volatile periods globally.

- The management alluded to the fact that ACFMS segment includes an exposure of Rs1300mn (~6.5% of FY23 revenues) to 2W ICE engines offerings that is at a risk of being obsolete due to the increasing penetration of EVs over the next 5-7 years.

The management’s strategy to counter risk presented by EV penetration is:- To focus more on supply of value-added offerings to off-road vehicles, construction equipment, heavy-duty engines which are not expected to be disrupted by EVs.

- Foray into EV-specific products like electric coolant pumps, electric oil pumps and BMS.

- Further, Pricol is working towards the development of disc brakes for EV 2 wheelers. Electric coolant pumps are currently under dispatch for customers like Tata Motors and Ashok Leyland.

My outlook for Pricol

- Management has set a target of 4000 crore by FY26 , There is a consistent growth in sale and company is growing its client and product list which looks like target is feasible

- Letter Of Intent of 3600 crore

- Company has had recently got into several strategic partnership – which will lead into new product line such as BMS, driver pump, Ecockpit display and these will get revenue by FY26

- Company is spending 600 crore CAPEX in next 3.5 yeas and will be using the same for achieving the 4000 crore target, which is funded by internal accurals

- 400 crore capex being used to increase capacity to ~4000-4200 cr which will be used to generate 3600 crore at 85% utilization rate and 200 cr by inorganic growth

- Margin expected to grow in coming quarters to approx-14% from 12%

- Premiumization is growing and Segment growing at fast rate for DIS and ACMS and pricol is industry leader in DIS.

- Many of Pricol products are propulsion agnostic works both on EV and Petrol/Diesel vehicles

- FII and DI’s have raised significant stake in the December quarteR.

- Pricol was earlier into mechanical instrument cluster which would sell aroun300-400rs , this is dying fast and the current driver information system costs are 1200-1500 and expected to make transition of 2500 rs over next 3 years.

- Pricol is working with almost 22 small and big EV vehicle makers nationwide.

Stock has rallied in past 6 months by 16%, Has very attractive fundamentals , can be bought at 370’s range , should cross 450-470 in next 1 year , approximate upside of 30%.

Short term impact of FAME policy on EV sector may slightly impact the stock**

Disclaimer: Not Holding the stock

| Subscribe To Our Free Newsletter |