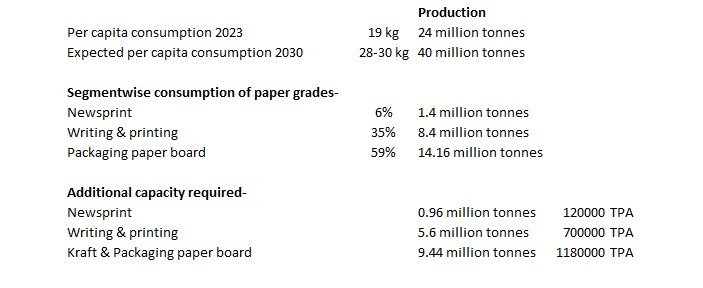

Paper Industry demand scenario-

Industry is expected to grow at ~6% so a back of the envelope calculation suggests that industry needs to add 2 million tons every year to catch up with the expected demand.

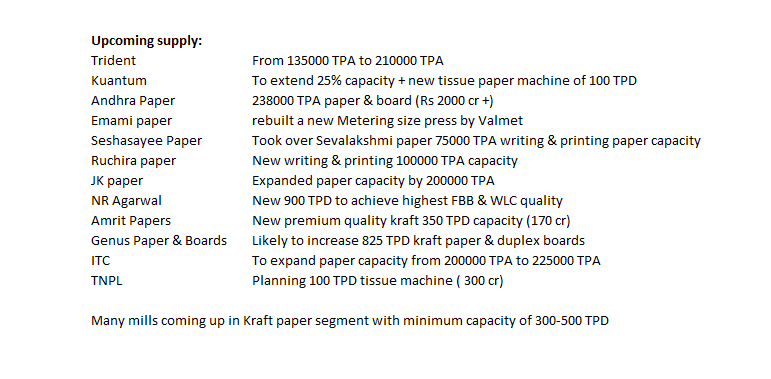

Supply Scenario- Major new capacity additions are as follows :

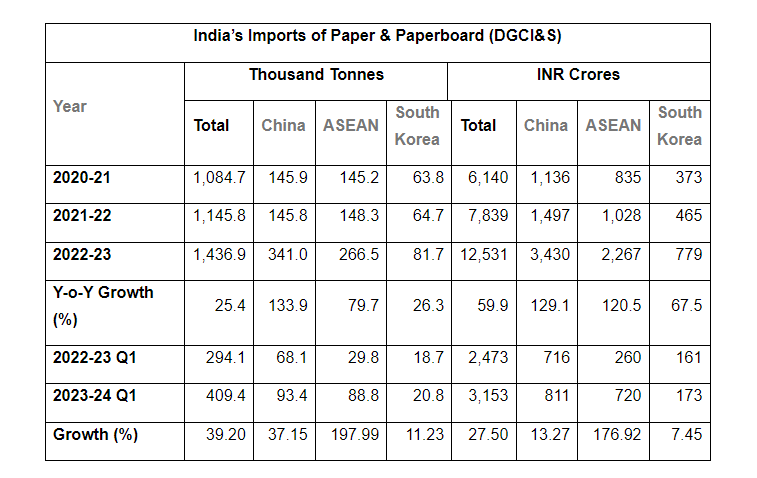

So the demand supply gap exists but its being addressed through imports which are on the rise since the removal of ADD. Indian imports of paper & paperboard have jumped 47% in FY23, the highest jump being in imports of uncoated writing & printing paper at 102%, followed by coated paper & paperboard at 51%. In the previous year, overall jump in paper & paperboard was ~25%.

In November 2021, the Directorate General of Trade Remedies (DGTR), recommended the continuation of then existing anti-dumping duty on imports of uncoated copier paper for a further period of 2 years. But the Ministry of Finance decided not to impose the anti-dumping duty and there is a logical reason for that. Paper is the most recycled commodity. When we import 1 ton of finished paper, it provides 5-7 times fibre for recycling, which in turn saves the foreign exchange on imports of waste paper. However, in the case of exports, every ton of export of finished paper, indirectly exports 5-7 tons of fibre also. The country has to thus make a higher foreign exchange payout for importing 5-7 tons of waste paper in lieu of every ton of exports of finished paper.

Over last few years, there has been a rising trend in imports and a declining trend in exports, thanks to the slowdown in China and massive paper capacity additions by Brazil, Uruguay & GCC. We don’t know when the demand for export will revive.

Other than that, one of the largest paper-making giants, Asia Pulp and Paper (APP), is going to set up the largest capacity in India (1.2 million TPA).

So to conclude, although India has been a net exporting country, going forward, it appears that exports are contracting due to excess global supply while imports are increasing due to higher demand in domestic market (provided govt doesn’t intervene). JK Paper undoubtedly remains the best bet in the entire sector but there has to be a trigger (say ADD on imports). What’s the trigger here? In my view, any moderate increase in demand due to NEP or single use plastic ban will be met by increase in imports if not interrupted.

Views are welcome, especially opposing views. I am sure I am missing a lot of things here. Happy to be educated. ![]()

| Subscribe To Our Free Newsletter |