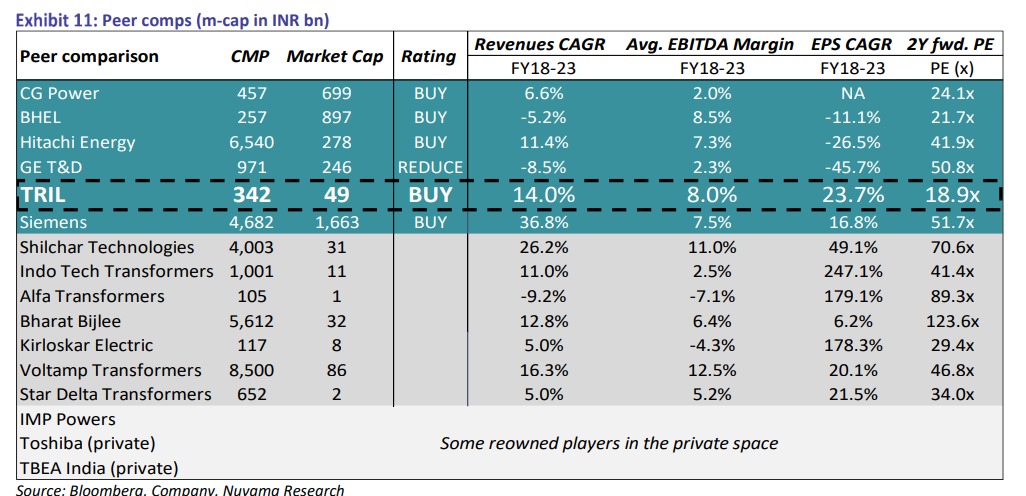

Page 5 is quiet funny,especially where Nuvama has given projections for the names out of their coverage. According to the analyst: Shilchar’s earnings are going to halve or fall even more,BBL’s earnings are going to fall by 75%,Star delta’s earnings are going to fall by 50-60% over the next 2 years and so on! All this while TRIL is going to have breakneck growth mostly due to low base of FY24(owing to various company specific issues)

Analyst seems to have extrapolated the revenue CAGR of Fy18-23 for all these names and extrapolated the exact margins. Thus,11% in Shilchar’s case,2.5% in Indo tech’s case,5% for Star,etc. seem to have been extrapolated. I doubt anyone would be so ill-informed to think that only one company(TRIL) with no particular niche is going to make 14-15% EBITDA while the rest are not going to have any margin expansion. The current numbers are already way better than extrapolated in the report. Other than Shilchar that derives major revenues from exports & thus makes margins head & shoulders above the rest,the sector is mostly homogenous & it’s not possible that only one company is going to benefit from power demand in the country & globally. Moreover,the pref & 500 cr QIP will lead to further dilution in TRIL’s case.In the meantime,no other transformer company has come to the markets to raise money.Even the ailing Alfa that turned around only this year has not raised money…so far atleast.

But other than somehow proving that TRIL is the cheapest name in the sector,the report was good.

Disc.: Not invested in TRIL…views maybe biased.

| Subscribe To Our Free Newsletter |