I will summarize here, but I will share my thesis and financial model as well.

My bet was on the hotel sector, as the demand is increasing while supply will take a few years to catch up. This will lead to operating leverage and excess cash. My bet is that SAMHI will not only become profitable, but also deleverage its balance sheet as sectoral tailwinds are the ideal time to strengthen themselves.

My detailed reasoning

Thesis

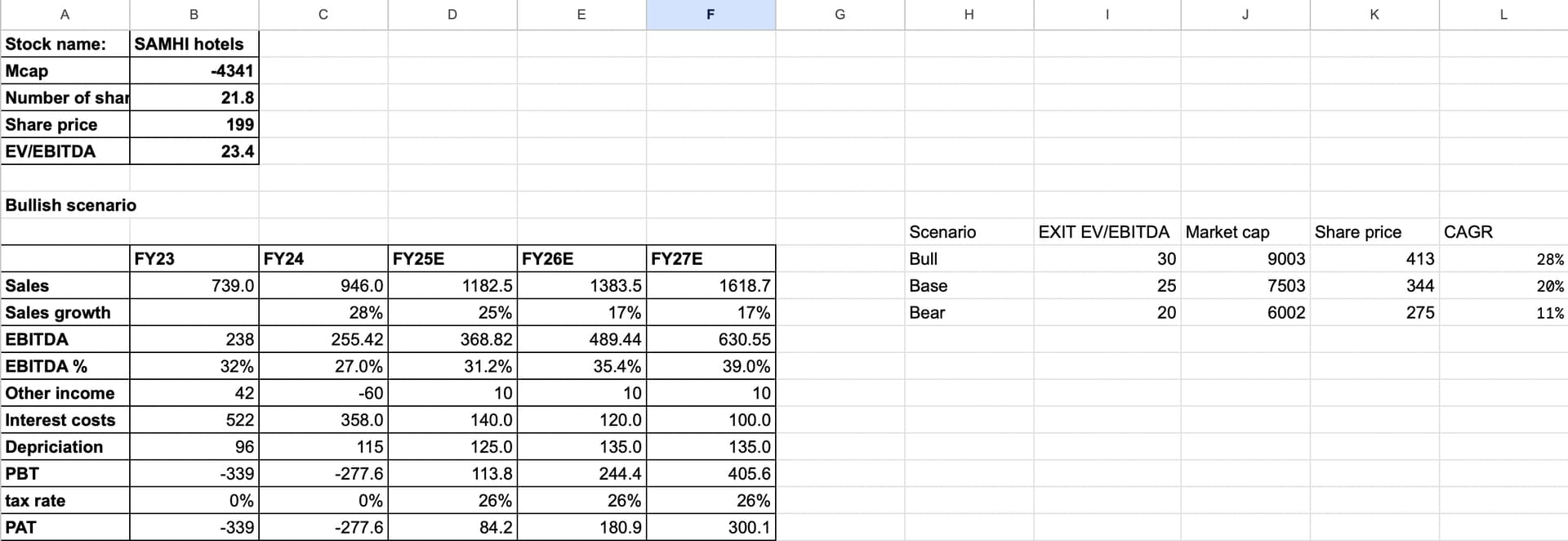

Sales growth

FY25 will see addition of around 10-12% more keys which are being added or will get ready from renovation. Moreover, we can expect a RevPAR in double digits, although we are seeing RevPARs in high teen or in the twenties, I don’t know if that can sustain and hence a growth rate of around 13% has been assumed until FY27E

The decline in growth rate from FY26 and FY27 is because not a lot of keys are being added, and we can only expect the newly renovated ones to start(around 900 are under renovation)

EBITDA

The business aims to increase the margins to around 38-40%. Moreover, they shared a chart in one of their presentations that talks of types of costs. 20% was variable and after looking at it, I thought of an additional 20% being semi variable in nature. Despite the fact that semi variable won’t rise as much as revenue, I assumed 60% of the additional revenue each year trickling down to EBITDA.

That is how the model has been made!

Other income

It shouldn’t be negative the next few years because the current year had a one off event and the company took the worst possible scenario and wrote off 70 crores.

Depreciation

It shouldn’t really increase because no keys are being added, only existing portfolio is getting renovated

Interest costs

for FY25, the debt is assumed as 3.7x their EBITDA which is their target. The cost of capital for the business is around 10% and hence the interest cost. Although the management hasn’t guided towards interest cost reduction or anything for FY26 and FY27, the free cash generation does make me believe that a bit of reduction might happen. I have taken a moderate reduction in interest costs post FY25

| Subscribe To Our Free Newsletter |