Disc: Biased and invested. not a buy or sell recommendation

Thesis

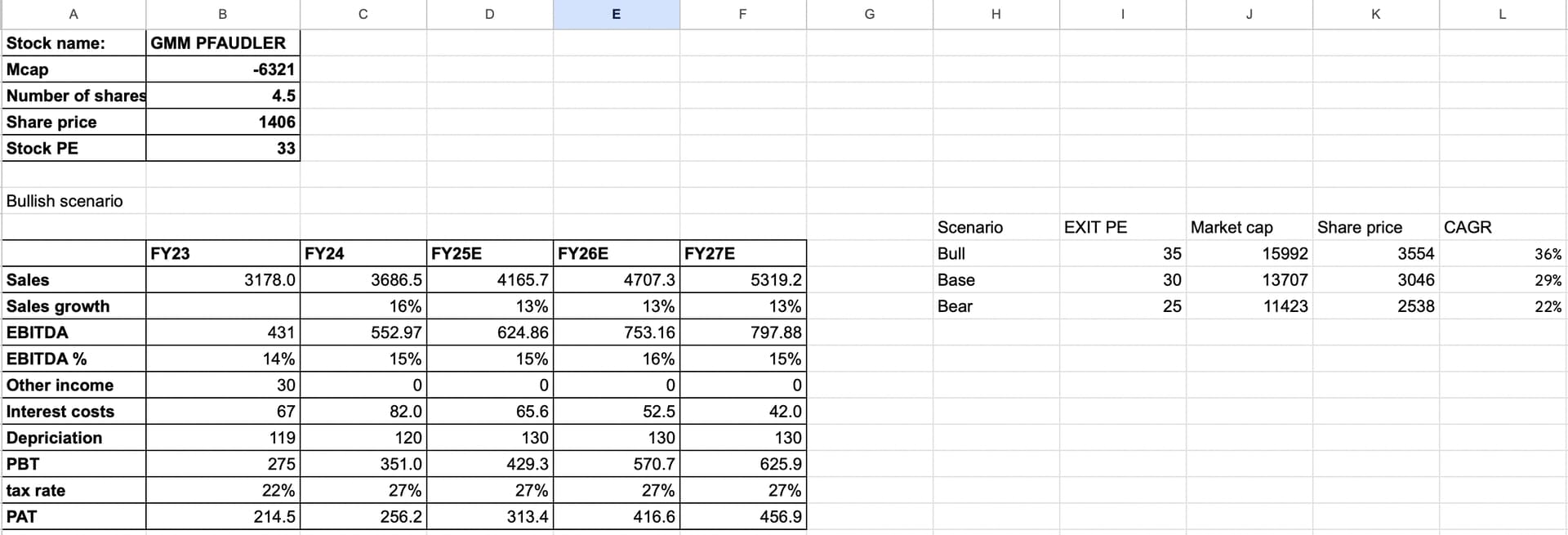

The business is on track to reach 3700 crore revenue by end of FY24 as the first half suggests(This was written before Q3 FY24 results, if one thinks 3700 might not be possible, we can assume 3600 as well)

They do expect a 13-15% revenue guidance and 18-20% improvement EBITDA. I am not concerned about revenue growth as chemical cycle should turn some day, I am fine waiting for it.

The promoters are already conservative but I still took the lower end from FY26 onwards

EBITDA margins too should improve as the share of services and high margin businesses like mixing increase.

I don’t expect them to go down unless chemical and pharma sector continue their slowdown or steel price rises rapidly

Which is a bit unlikely

I again went a little conservative and went to about 15-16% compared to the 14% last year

50% of EBITDA is free cash flow and hence, interest costs should go down, they expect to be completely debt free in 2-3 years but I only decreased it by 20% each year

64 crores is interest cost, 16 crores is related to forex so that might still stay.

Depreciation might increase a bit as capex will be required to meet these goals and they do plan to acquire mixing businesses

And 27% tax rate as the company stated

Possible antithesis

The business is largely dependant on Chemical and pharma sector. Any slow down in these businesses will mean that all proxy manufacturers fight for the same order book and hence margins get depressed, which is what has been happening in FY24.

Another issue is the impact of commodity price of Steel.

They have exposure to a lot of international markets, China and Germany are both showing signs of slowing down with chemical companies in Germany moving their manufacturing to other countries

However, they are well diversified and such issues could be offset by other countries.

Moreover, acquisitions in mixing businesses and other industries have a high profile margin, so even that picking up will offset these setbacks.

| Subscribe To Our Free Newsletter |