BHEL – Investment case

- Company Overview – BHEL

- BHEL – PSU is India’s dominant producer of power & industrial machinery since 1964

- 200 GW+ installed capacity (70% power generation in India from BHEL Installed capacity in India)

- Key beneficiary – Aim to achieve 50% market share from non power segment (30% presently)

- Attractively placed for capacity addition of high growth sectors – Decarbonization, Green Hydrogen, Transportation, Aerospace & Defense with impetus on “Make in India” & “Atmanirbhar Bharat”

- Market Cap – INR 88k Crs, Revenue INR 24K Crs, P/B – 3.4x

- Order book – 1.2 lac Crs

- 503 patents filed in FY23 – Total IP – 5,443

- Selling shovels during a gold rush

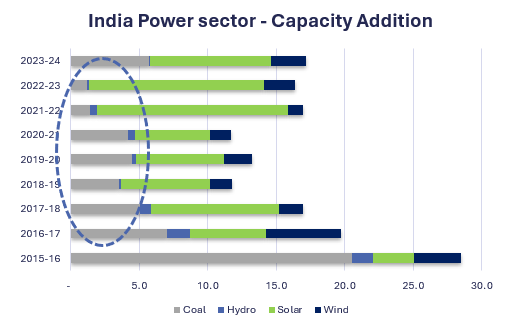

- Minimal Thermal capex investment for during 2017-24 period (<5 GW pa)

- Leading to deficit in 2024-27 period

- Focus on capacity addition – Thermal, Solar, Wind

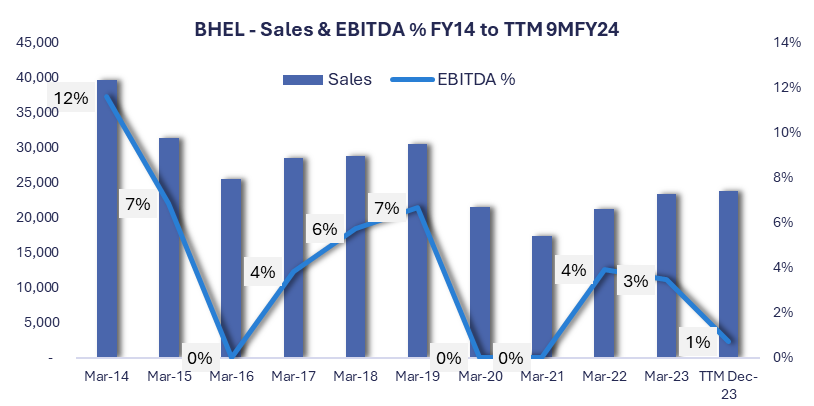

- At the bottom cycle from financials, upward cycle has begun

- Investment case

Good

- Uptick in thermal capacity addition due to strong electricity demand, uptick in spot market prices and no major capacity addition in next 3 years

- No major presence of Chinese / International BTG supplier – major beneficiary last time

- Strong order inflow from Central, State & Private sector utilities

- Improvement in order terms – commodity cost pass-through – learning from last upcycle

- Reduction in manpower – 50k to 30k

- 30% order book in non power sector & management focus on developing non power sector order book – Target 50%

- Decrease in competitive intensity will lead to better margins

Better

- Decarbonization opportunities – FGD, Green Hydrogen, Renewable generation

- Defense & Aerospace opportunities – Cryogenic component, Batteries and other components for Chandrayan -3, indigenization of imported parts

- Transport opportunities – Railways & Urban Transportation – 80 Vande Bharat trains Kavach etc.

Best

- Efficient capital management from shareholder perspective

- Improvement in efficiency at part with best global OEMs

- Improvement in execution capabilities

- Recovery and resolution of sticky receivables through mutual agreement, arbitration & other mechanisms

- Ability to make significant break-through in decarbonization and green hydrogen sectors

- Technical analysis

Price uptrend continuation with all time high volumes

- Risk

- Being an PSU, majority shareholder may influence business decision, capital allocation strategy

- Historically faced with sub par execution skills and delay in delivery, may not scale up due to such issues

- Profitability may be impacted, or receivables may not come through due to any reasons, as seen in last cycle

Disclaimer: Education purpose only, Not an Investment advice or recommendation.

| Subscribe To Our Free Newsletter |