Q4FY24 and FY24 results observations:

Standalone Q4FY24 YoY:

- Other Income doubled due to one-time transaction gain: 7,340 Cr from stake sale in subsidiary HDFC Credila Financial Services Ltd

- Operating expenses include one-time staff ex-gratia provision of 1,500 Cr.

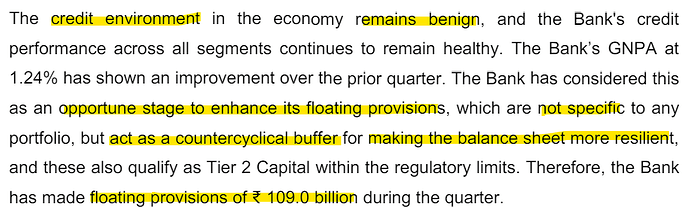

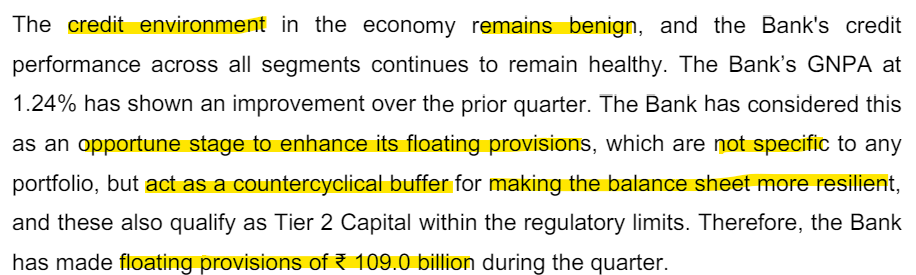

- On creation of the floating provision of 10,900 Cr in Q4FY24.

- Tax expense was (749) Cr due to Tax credit of 4,400 Cr

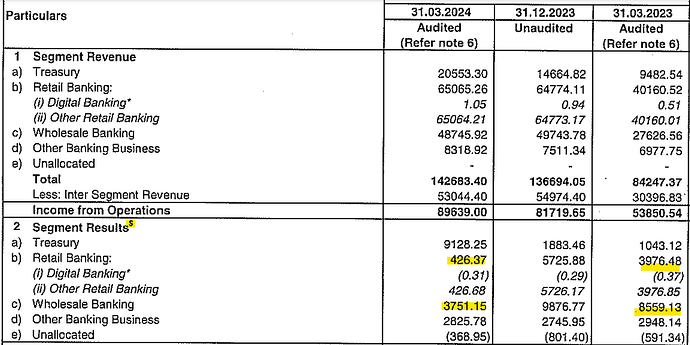

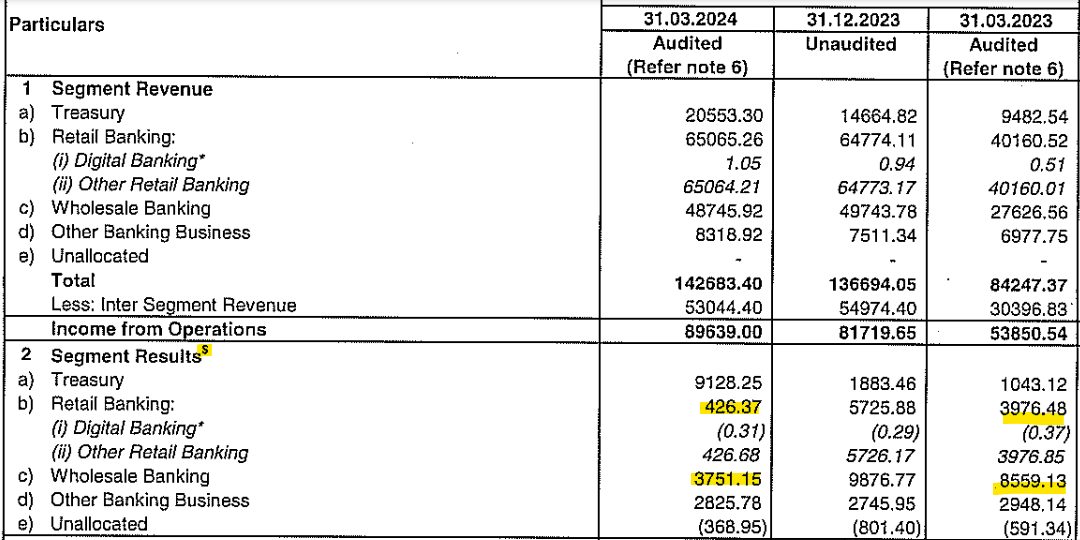

- Segment breakup:

-

-

-

- Deposits increase benefitted from March quarter seasonality. Do not extrapolate as Q1 is always slow historically.

Overall:

- HDFC Limited merged with HDFC Bank effective July 1, 2023. Prior period numbers are not comparable.

- LDR will stay elevated than the past benchmarks for a couple of years. Need to keep reserves to repay the obligations of the eHDFC’s Bond that mature as per their maturity pattern

- No anchor on NIM. Will not chase growth for sake of growth and will neither go down the risk ladder or price ladder. Profitability is extremely important and drop-off in volume is ok, Deploy basis what gets mobilzed. Stable margin is the focus with a positive bias over the next 2~3 Yrs.NIM improvement should be a function of how we substitute the high cost bonds that come up for maturity over a period of time with deposits.It will take time to happen in a gradual manner. Till then (over a period of 2~3 Yrs) stability of metrics (ROA, NIM) remains the focus. Once high cost bonds are exhausted, the bank will have liquidity and ability to unleash growth with profitability coming back to the core level.

Nutshell:

Still settling down. Better growth and profitability seems possible after 2~3 Yrs as high cost borrowing maturity will start to happen from FY25 onwards.How much YoY? Upcoming AR might help.

| Subscribe To Our Free Newsletter |