The opportunity looks interesting with the management aiming to achieve INR 130Cr EBITDA in FY ’25. With 190 Cr of Debt and INR 720 Cr Market Cap, that makes the valuation reasonably attractive at ~7.5x FY ’25 EBITDA. However, there are a few questions I had, if anyone has had a chance to look at these :

-

Is the Orchid Hotel, Mumbai owned by the promoter entity Plaza Hotels Pvt Ltd (PHPL)? The company presentation says it is an ‘owned’ hotel but Plaza Hotels’ annual report says that it has been given for management and operation to KHIL and is owned by PHPL.

-

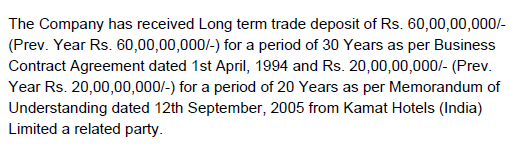

INR 80Cr of long-term trade deposits have been given by KHIL to PHPL interest-free. INR 60Cr was given for a period of 30 years in 1994 and INR 20 Cr was given for a period of 20 years in 2005. They should be up for renewal in 2024-25, if there has been any update on this.

-

KHIL paid INR 3.6 Cr of royalty expense to Plaza Hotels Pvt Ltd in FY ’23, for the leasehold land. How are these payments determined? Are they based on a % of revenue or are these fixed payments each year?

-

22 Cr loan (from the NCDs raised in Jan ’23) was given to Plaza Hotels Pvt Ltd by KHIL. KHIL received an interest of INR 80L on this in FY ’23. It is unclear why the loan was given and what is the rate of interest being paid to KHIL by promoter entity (PHPL).

- Contingent liabilities: As per clause 45.3 of FY ’23 AR, there are INR 60 Cr of contingent liabilities relating to a tax demand which have not been provided for. Couldn’t find much details about the tax demand.

I’ve also posed these questions to the IR. Awaiting their response, but it will be helpful if anyone has already spent time on this diligence.

| Subscribe To Our Free Newsletter |