Having laid out my investment approach in the 1st post, let me argue the case for the 1st stock in my portfolio (in alphabetical order).

Abbott India Ltd

At the outset you will point out that it violates pt.5 – Avoiding Unaligned Owners – MNCs (especially when they have an unlisted entity). In the case of AIL however, the evidence suggests that the consequences of this arrangment have not harmed minority shareholders (yet.)

The unlisted business does not step on the toes of the listed entity in terms of cannibalization of products, markets or management bandwidth.

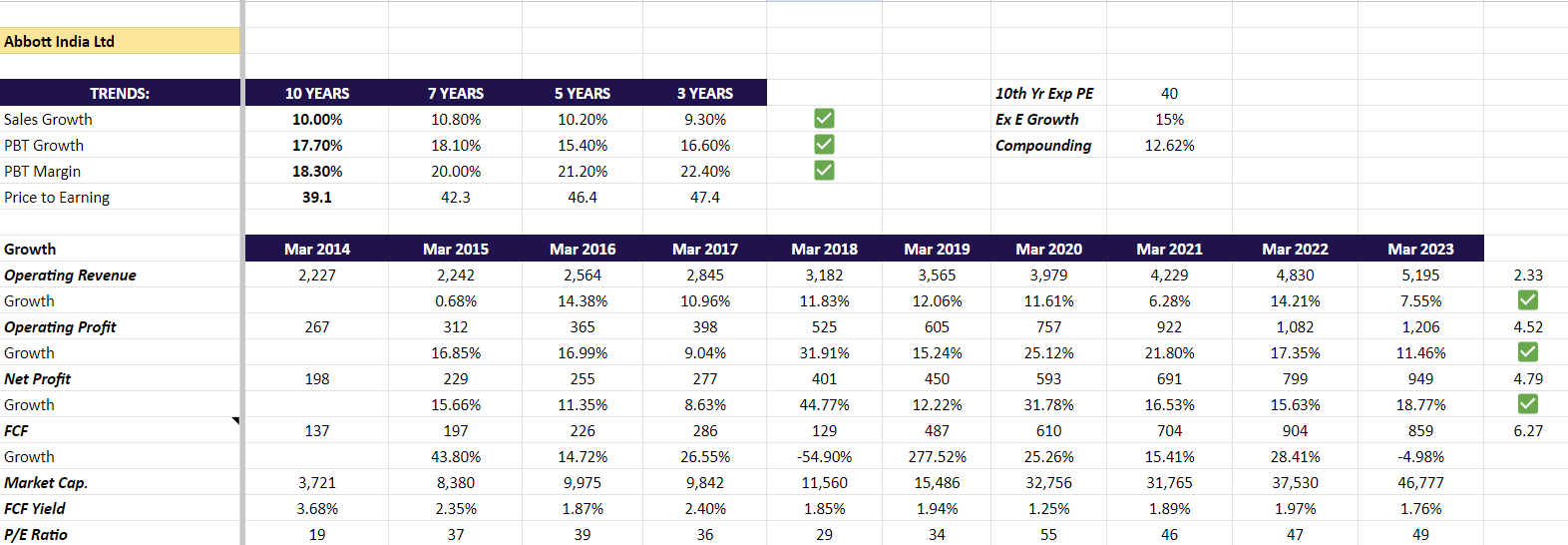

Quantitative Analysis

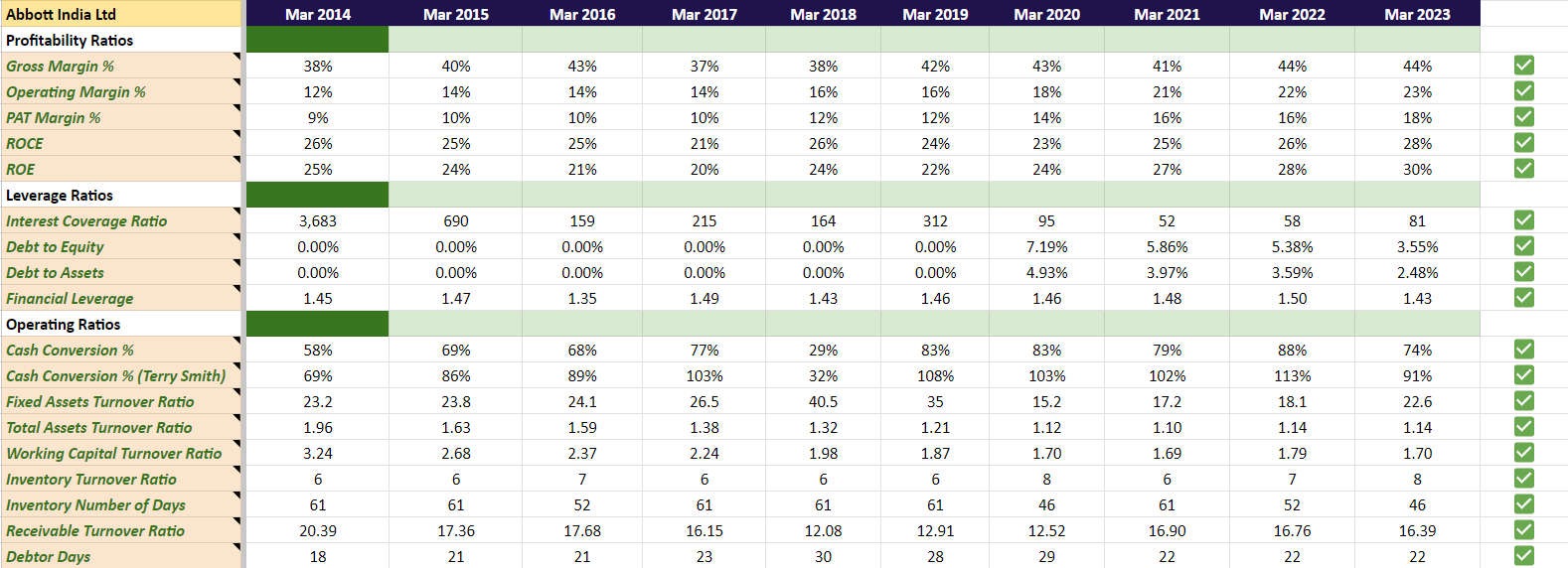

Ratios – Profitability, Leverage, Operations

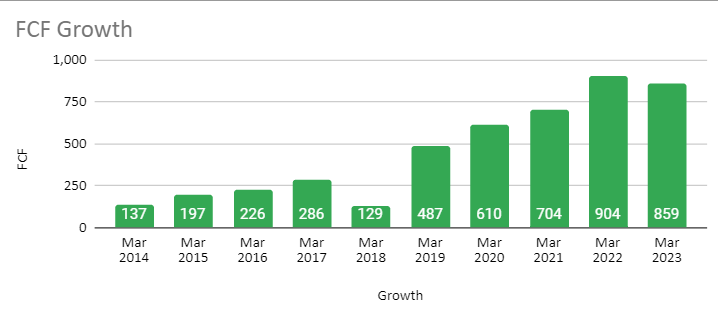

Free Cashflows

I can infer from the numbers above that –

- AIL has maintained high ROCEs consistently in the past 10 years

- It has also grown operating revenues consistently in the past 10 years

- Healthy and improving gross, operating and PAT margins – Profitability Check

- Leverage is not an issue – Leverage Check

- Healthy Fixed Asset + WC + Inventory + Receivable turnovers in the past 10 years Ops Check

- Resulting in a growing stack of FCFs YOY

Qualitative Analysis (Go from answering easy to hard questions – helps save effort in the process of elimination – via negativa)

Management Quality

- Does the management have a track record of good governance and clean accounting?

Yes. There have been no corporate governance issues in AIL in it’s history and has clean accounting.

- Do the owners of the company have connections to political parties?

No, they stay out of the limelight.

- Does the company have a strong track record of efficient capital allocation?

Yes, they have maintained high ROCEs in the past. The large part of the net income has been dividended out to shareholders in the last 3 years as it can’t be absorbed into the business.

- Do the promoters have a track record of remaining focused on their core operations?

Yes. They have not invested in unrelated businesses.

Industry Attractiveness & Company Positioning

High historical long term ROIC – WACC spread in the industry. It allows dominant players to earn and keep a profit.

- Is the company’s business heavily dependent on government regulation?

AIL’s business can be affected if a majority of the product protfolio in included in the NLEM which is price capped. Currently, almost 26% of AIL’s business by value comes from NLEM products, the rest is from non-NLEM. There is scope to increase prices inline with WPI even within the NLEM list.

- How many competitors are present in the industry and how strong is the competitive intensity?

If the molecule has had a LOE, then a lot of players will jump into the fray and drive down market share and profitability – {Duphaston}. However, if there is an active patent for the molecule, there is exclusivity and high margins + monopolistic market share. There are plenty of competitors present in the industry, however, there are 2 – 3 players which dominate each molecule in terms of market share.

- What is the overall size of the industry and its growth potential?

India’s domestic pharmaceuticals market (IPM) is estimated at 2,21,922 Crores in 2023 and the market is expected to grow at a CAGR of 8.8% between 2022-2027 reaching 3,08,329 Crores by 2027. It will be driven by economic growth, increasing penetration of health insurance and increased private sector investment. AIL can positively maintain a topline inline with industry growth CAGR +1 or 2%. AIL has demonstratred a ~ 10% operating revenue growth YOY for the past 10 years.

- Is the company in an industry where the proportion of value addition is high?

Yes, there is value addition in terms of product efficacy, administration of the drug, packaging, innovative SKUs (pill, gels, liquids), availability online and offline, and doctor trust and recommendation. All this is determined by AIL and is under the ambit of AIL. Value addition is high (except for the Novo Nordisk portfolio)

- What is the capital intensity and capital efficiency of the industry?

Once the licensing rights are obtained, AIL’s business requires low capital reinvestment (<5% of capital employed) and is able to convert around 80-95% of net income to free cash flow. AIL typically earns 80-90% of incoming cash from business operations and balance from interest income (Exceptions are seen in the FY where there is a major sale of business assets or loan repaid by subsidiaries). Its average cash conversion ratio (net CFO/net income ratio) over the last ten years is 85%. It holds a large reserve of term deposits to maintain liquidity and finance its working capital. Over the last 10 years, Abbott India has reduced costs, improved gross, operating and net margins, decreased cash conversion cycle by 85% and maintained ROCE>30% and ROE > 20 % without resorting to external debt. It has maintained leadership position in most of the categories it operated in the last decade.

- Is the industry’s business dependent on India’s broader economic cycle?

Abbott India Ltd’s business may be influenced by India’s broader economic cycle to some extent.

Its dependence is moderated by factors such as the essential nature of healthcare products, government policies which are always going to be pro-healthcare spending, and positive demographics. The therapy sectors chosen by Abbott India generally require long term medication to manage the symptoms of the disease.

- Does the business generate excess returns for shareholders?

Yes. ROCE is 2x COC for decades. This results in free cash flow growth and excess returns for shareholders.

Sir John Kay’s IBAS framework

- What is the company’s track record on innovation?

AIL focuses on new launches, which is fairly consistent (+100 launches and line extensions in the last 10 years). Target for the next five years ~75 launches. They try to extend the lifecycle of each megabrand molecule through innovations like introducing a gel, topical lotion, spray as well different SKUs depending on use cases. They also have a strategy of looking at molecules which will experience LOE in their relevant sectors – women’s health, GI, CNS, Metabolics, Vaccines, Etc. AIL is investing in creating new categories related to the aforementioned sectors, hoping to scale them in the future.

- What is the company’s investment in brands and reputation?

AIL has 15 brands which are market leaders in their respective segments, accounting for over 80% of our revenue. Their reputation is better than other generic pharma companies with competing products.

Doctors trust prescribing Abbott brands over competition. Duphaston is still the leading pill recommended by IVF clinics, where the stakes are high, although the brand may have lost market share in the gynac division (with comparitively low stakes for patients).

- How strong is the company’s architecture?

1/3rd of the manufacturing is in house, 2/3rds it outsourced, leaving AIL with an asset light model and a high fixed assets turnover ratio. It has excellent parentage which supplies AIL with new and innovative products for India which AIL doesn’t have to spend a dime (of royalty) giving it superior ROCEs in a growth market. It has good penetration in urban areas (esp metros) but reach into tier 2, 3, 4 towns is still lacking. It has also adopted the e-pharmacies channels in India. AIL can be thought of as a sales and distribution arm of Abbott Ltd. (USA) for India. It does not incur any PD/R&D costs and has a ready pipeline of products.

- Does the company own any strategic assets?

The key strategic assets for AIL are – Leading brands in categories they play in, excellent parentage resulting in a long product pipeline, doctor + pharmacist trust, category creating abilities. They also stay away from parts of the industry which are very heavily regulated.

- Does the company have ROCEs that are higher than the industry average?

Yes, AIL has ROCEs 2x that of the industry, consistenly well above its COC.

Miscellaneous

End consumers (patients) are dependent on doctor’s prescription or pharmacist’s recommendation in the selection of medication. Concerns about quality control and manufacturing practices at local generic manufacturers in India has led to the perception that only well known brands generally sold by MNCs are safe/ trustworthy to use. This allows branded generic pharma companies to charge premium prices on off patent/ generic drugs.

Lindy Effect – The Lindy effect (also known as Lindy’s Law) is a theorized phenomenon by which the future life expectancy of some non-perishable things, like a technology or an idea, is proportional to their current age.

Abbott India Ltd. was incorporated on August 22, 1944, so it has stood the test of time and most likely will be around for another 80 years or so. (It was called Boots Pure Drug Company then, but it has had operations in India from 1910 throught a pvt ltd. company.) I am long on the longevity of the business.

Disc – Bought in March 2017 at ~ Rs. 4500 at a PE of about 33x. Holding.

| Subscribe To Our Free Newsletter |