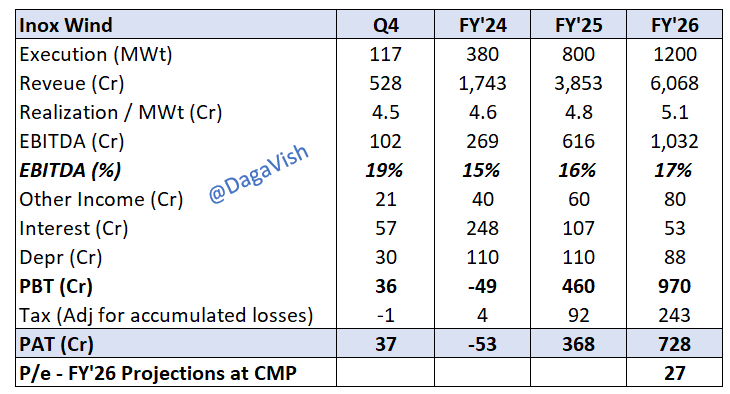

Basis the Q4 results & Management commentary on concall, have tried to extrapolate the financials for the coming years. Basis the same, at 20k Cr Mcap, it is valued at ~27x FY’26 projections. However, orderbook gives an opportunity to execute more + New order additions in FY’25 can add more to FY’26 topline.

Key assumptions:

- Realizations hold at Rs.5 / MWt for next 2 years

- EBITDA guidance of 15%+ for coming years

- Mgt. has guided for debt free by H1 of FY’25 and no further capex in the next 2 years considering capacity is already built for 2-2.5 GWt. Hence the overall interest and depr cost should start tapering down as we go ahead.

Disc: Invested

| Subscribe To Our Free Newsletter |