1b18582c-8e63-42ba-9410-d83b445daa7c.pdf (bseindia.com)Q4 and Fy24 results.

Subdued performance for many verticals including hi-tech manufacturing, IT services. While hi-tech and defence may pick up in future, not overall convinced with execution in these areas.

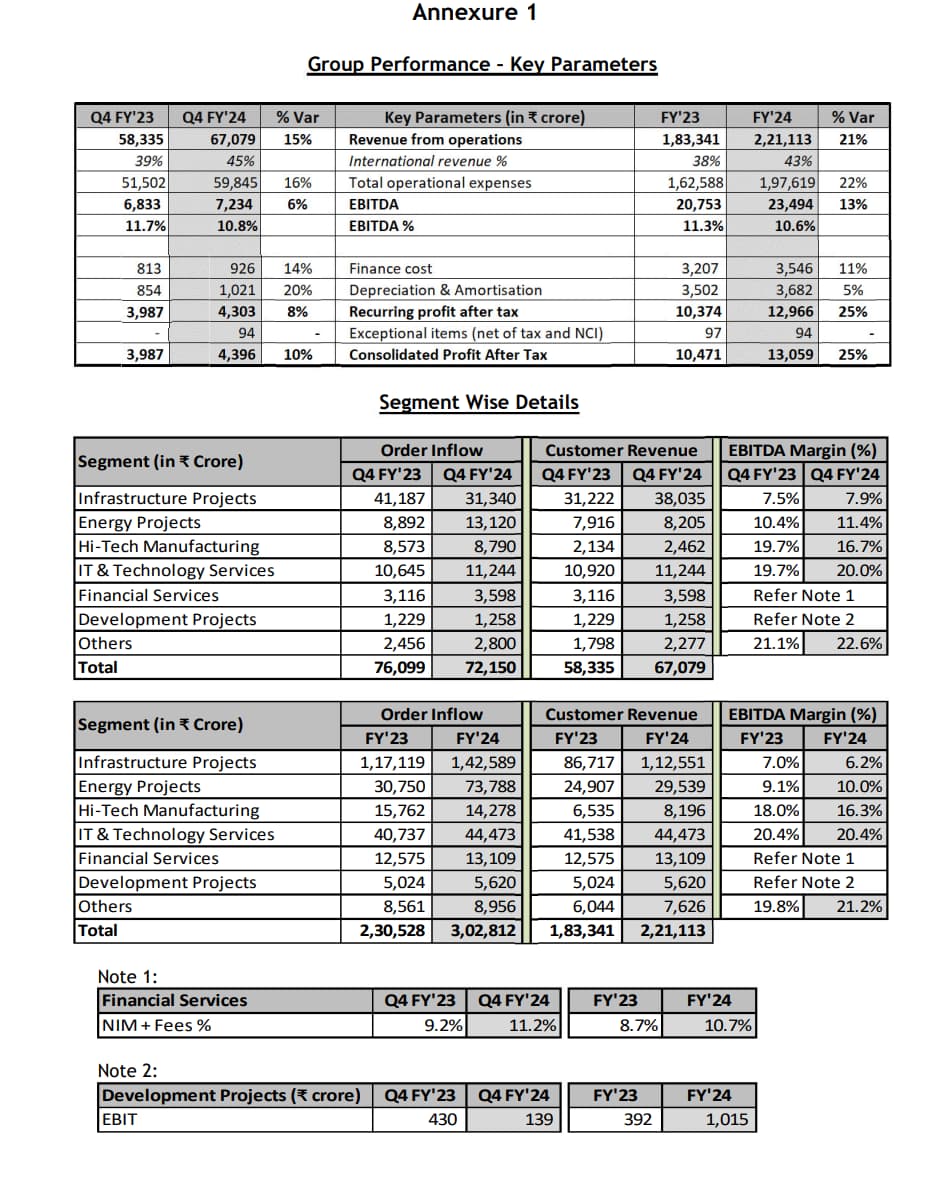

Decent performance on Infra and Energy divisions.

Exceptional profit in development projects due to sale of commercial land in Hyderabad Metro. Otherwise, dull results there

Finance vertical is picking up but I am not convinced with retail strategy here.

While Energy vertical has done well and shown 100% growth in order intake because of GCC orders, same may be subdued this coming year with slowdown in GCC orders. Saudi has cancelled NEOM projects, reduced spending on Oil & Gas. This is crucial bit to check.

Overall, no compelling reasons to buy at this price. More of a wait and watch mode.

Discl: Invested in Family A/cs at much lower price.

| Subscribe To Our Free Newsletter |