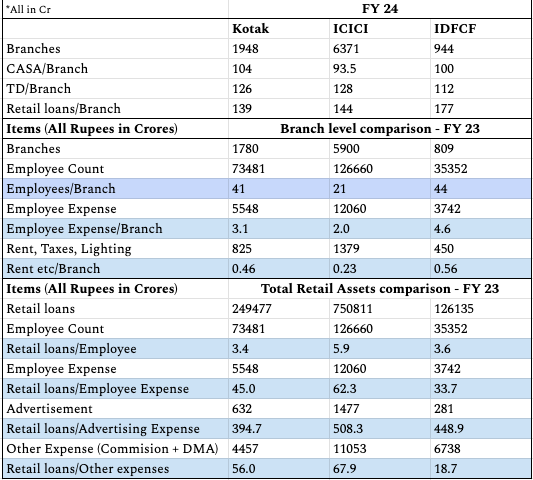

I looked at the operational performance of IDFC bank at branch level and compared it with Kotak and ICICI Bank. Please have a look and share your thoughts.

Branch level highlights of IDFCF:

-

IDFCF branches have similar or more average CASA than ICICI & Kotak. It will be interesting to understand the reason since almost 40% of branches are <3 yrs old.

-

IDFCF is distributing ~20% more retail loans/branch than Kotak/ICICI – although at much higher commission ratio (see point 7 for details).

Insights into higher Opex of IDFCF:

-

IDFCF has similar employees/branch as Kotak – but its average employee is paid almost ~40% more than Kotak’s. This difference can be slightly off as banks deploy employees differently but the general idea is fairly accurate.

-

IDFCF has ~20% higher rental etc expense per branch compared to Kotak and almost 2.5x that of ICICI – probably because most of its branches are in urban areas at good locales.

-

It is also interesting that IDFC’s per employee retail loan is similar to Kotak, but almost ~40% less than ICICI. Retail loans/Employee expense is a drag in Opex for IDFCF – it is almost ~30% lower, which should improve over time as the branches mature.

-

Advertisement expense is actually fairly similar to Kotak and sligly more than ICICI, relative to its retail asset and liabilities size.

-

Other expense – which mostly includes commissions is the biggest drag on Opex – IDFCF spends 3x more than Kotak and ~3.6x more than ICICI to generate same amount of retail loans.

-

Other Expenses should continue to be a major watchout for the investors as the commission expense per loan may not come down with scale. The bank will need to work hard and innovate in its distribution strategy to reduce this expense. Other expenses can also include different items for different banks, I have tried to make the comparison as fair as possible.

** Overall comparison with Kotak is more fair since its retail:corporate split is similar to IDFCF.

| Subscribe To Our Free Newsletter |