Con Call Notes from Q4-FY24. CMP 154

-

EBITA Margin 17%

-

Interest cost not coming down in Q4 despite 1000 cr debt reduction in Q3-

- Overall rate has not come down

- Some interest on tax due to better outperformance (I did not get what it means, but it seems to be some sort of one-off part)

- Reduction in interest rate will contribute to lower interest rates in the future.

-

Capex of $87 million

-

Dahej capex is likely to come onstream by Q1-25

-

Investment in key starting material, debottlenecking for CHG

-

Capex will be similar to last year in FY25.

-

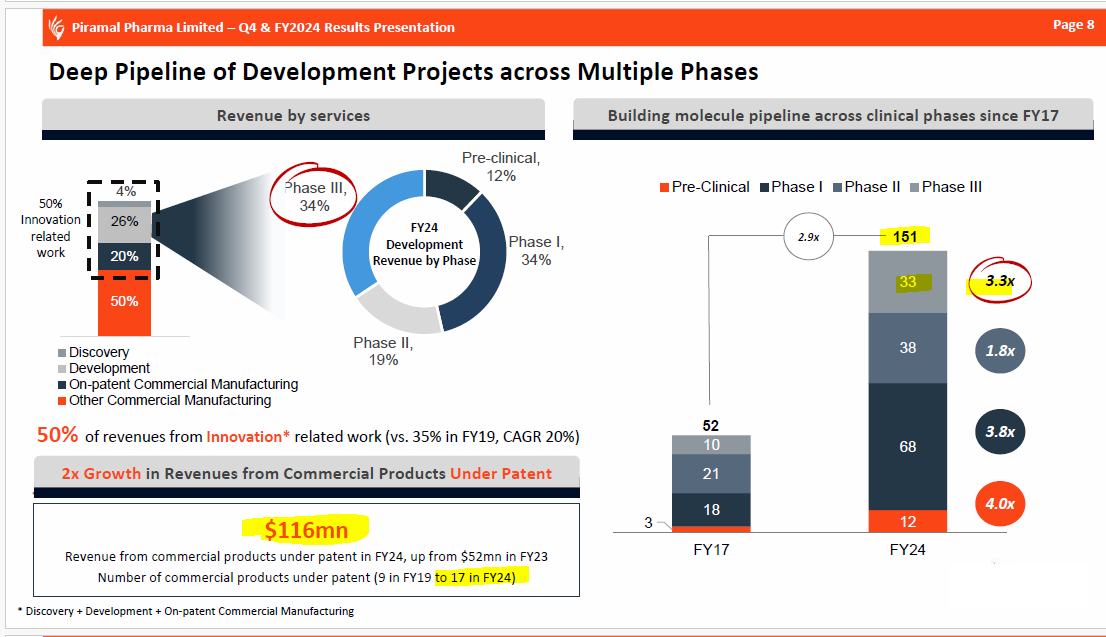

Innovative business 50%. Grown by 20 CAGR over last 3/4 years

-

40% of the order book is for integrated services (orders for more than one site)

-

Once biotech funding improves, growth will come back from emerging companies. This is not reflected in the current guidance

-

Visibility is higher than last year as compared to last yearly

-

Due to nature, PPL high inventory during Q1-Q3 but it goes off as proudct is shiiped to clients.

-

Peptide- Generic business is doing well and working towards getting into the on-patent business.

-

18 months back, PPL saw funding issues with Bio-tech and hence pivoted to big pharma. This pivot has helped in Fy24 with more business from big pharma.

-

PPL has been doing conjunction for over ten years

-

Biosecure has increased interest from clients in innovative patent work.

-

ADC- Number of large pharma visited in last six months. So expect to get business from them in the coming yearly

-

Most of CDMO’s capabilities are in place. So, future capabilities will be more brownfield.

-

Generic product capabilities are fungible for patent-related work if needed.

-

High fixed-cost business. Increased sales drive professionalism. CDMO and ICH will be drivers of the increase in profitability in the future.

India Consumer Business

- New products launches in e-commerce. Once they are successful then PPL will launch in general trade. They kill them if they do not meet target.

CHG (Hospital Generic)

- Incurring non-recurring expenses related to CHG, so cost – Cost of 8-9$ million

Outlook for Fy25

-

Early teen growth-

-

CDMO will be better than CHG

This is the best slide to track the company performance

My Take

I get the impression the company is keen on expanding on patient businesses. Last year, two companies announced the commercialisation of two products. I think their business would have been a major driver of the increase in revenue for the patent business. As they launch their product in the market, and as the product gets better accepted, it is likely that these two recently launched products will give more business. I think the CDMO on-patent business shall be higher significantly again in FY25, even if there is no more product commercialisation in FY25.

Note- Invested

| Subscribe To Our Free Newsletter |