Q4 2024 and 2024 annual results were announced a couple of days back.

Core matrimony business topline is growing at ~8% CAGR in the last 3 years. The growth comes primarily from higher # of paid users, which have also increased by 8% CAGR. There does not seem to be a big shift in market share between the 3 players or a pricing change or offline→ online movement.

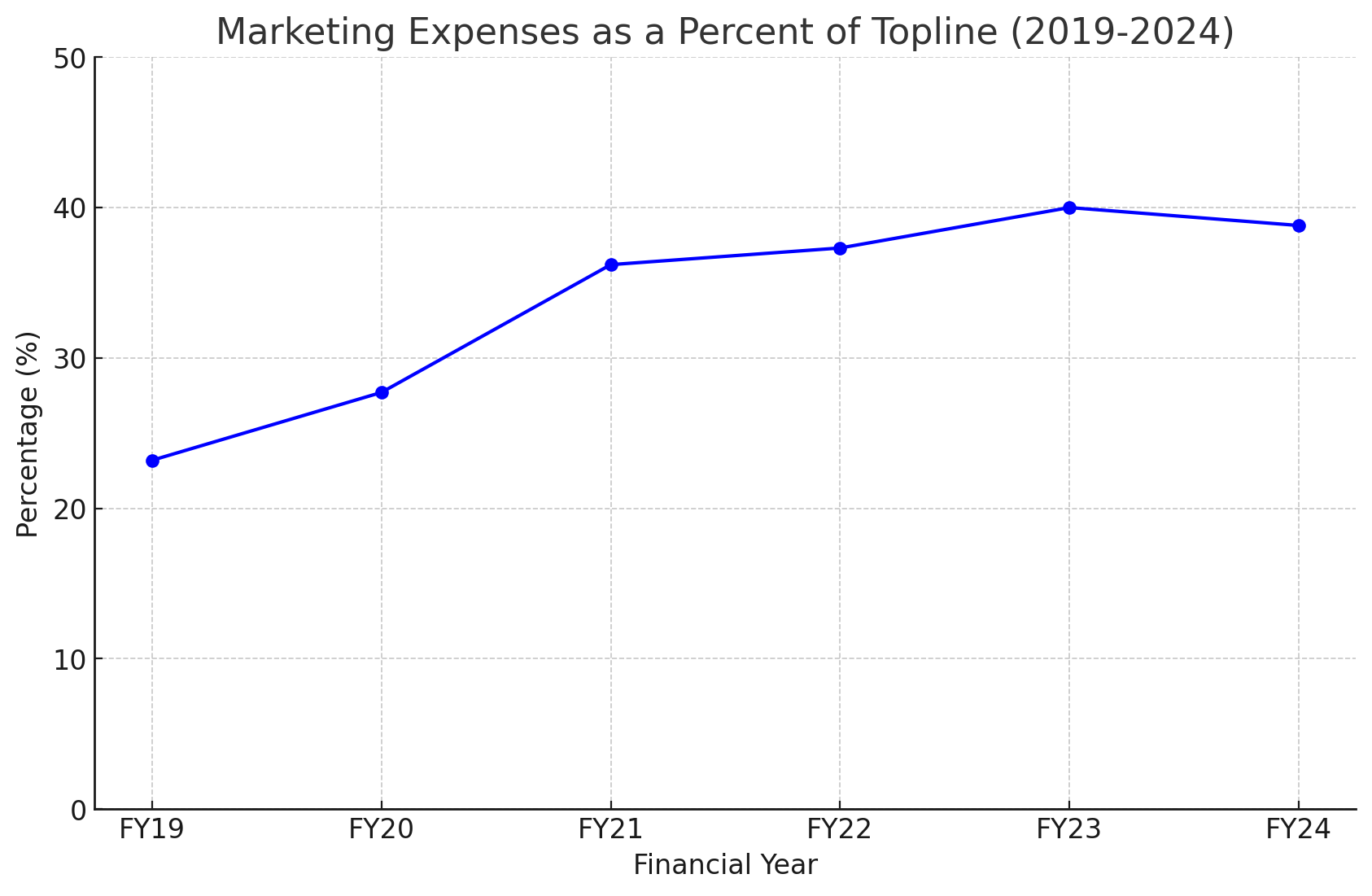

On the other hand, EBITDA has not kept pace with revenue increase because increased intensity on marketing expenses (increased from 22% to ~40%)

An interesting point to note is that out of the INR 50 Cr PAT in FY 2024; INR 26 CR is from interest income from their INR ~340 CR cash pile.

Potential triggers:

- Irrational competition reduces and marketing spending comes back to 20-30% range

- Able to re-invent and open new markets with Jodi or Luv (2+ years)

- Find a new revenue stream through ads/other partnerships

- Breakout with wedding services marketplace (looks unlikely as they have already invested 5 years)

I am going to stay invested for some more time. I believe consolidation will happen in this business and margins will improve. Plus they have a good shot at making other segments big.

Disclosure – Invested and hence biased

| Subscribe To Our Free Newsletter |