Some macro thoughts + my very basic estimation.

- EPC dhanda will lead to further margin contraction. Stocks usually get positively re-rated when two triggers happen – margin expansion + growing volumes. Given only one trigger being hit next year, I think we can expect some consolidation after the stock settles from this knee-jerk reaction we’re seeing

- First order thinking would suggest some apathy towards the minority shareholders when management hikes the incentive to 3.5%. Second order thinking would suggest them seeing higher EPS in the future in a highly cyclical business

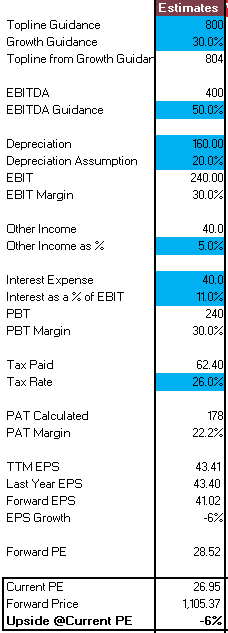

- A very conservative estimate shows EPS decline by 6% – I don’t think it’ll be anywhere close to that – but it helps visualize some margin of safety at current PE levels. Lower tending PE re-rating will throw this out of the window

- It’ll be interesting to see interest expenses over the quarters since the co is looking to gear up

- The stock remains a broader proxy to the infra theme. The “extrapolated” topline is also very conservative – unless something in the system breaks, we should be well beyond that

| Subscribe To Our Free Newsletter |