Disc: Invested and biased

First

why is it a proxy to Affluent India?

India is witnessing multiple opportunities which are empowering the country. One of the key opportunity which was highlighted by Goldman Sachs as well is the rise of Affluent of India.

the income or the number of individuals with a set amount of income is rising which allows them to look beyond daily needs. It allows them to spend on wants and invest for a better future.

Nuvama is rightly placed because the key market it caters to is HNI and UHNI. Moreover, its increasing emphasis on Asset Management makes it the right fit to play the bet on rising income levels.

Thesis

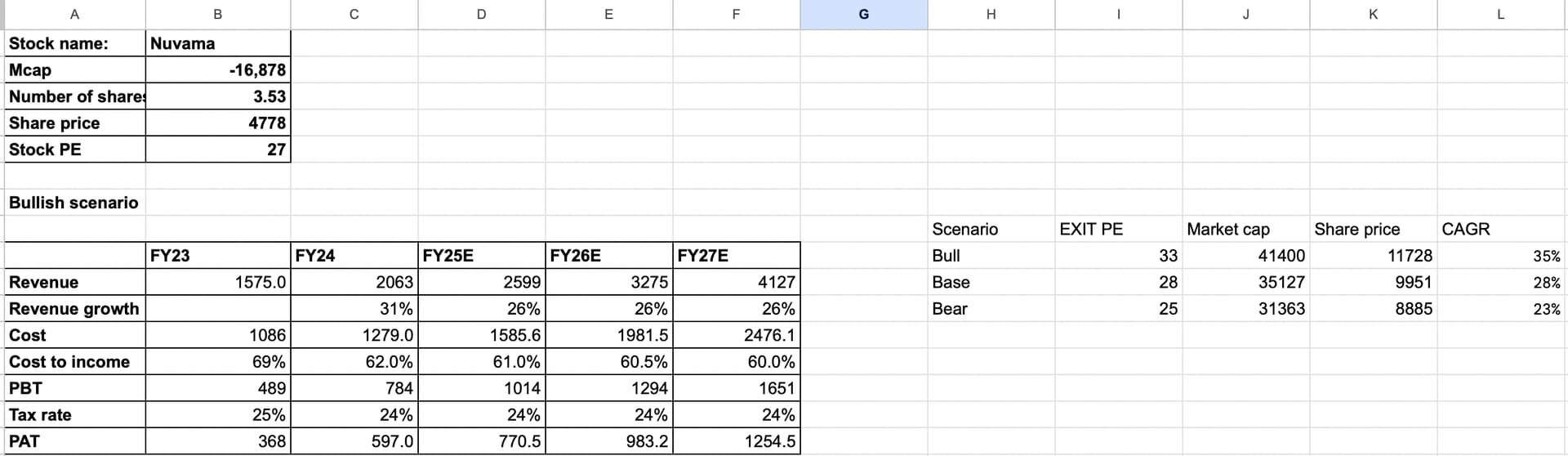

The financial model works a bit differently here. High emphasis is placed on Cost to income by the management and the statements issued by them show the same. and it makes it very simple to understand the key aspects of the business and also highlight the operating leverage at play.

Sales growth

Firstly, Increasing RM or relationship manager is basically the capacity expansion of a wealth management company. Currently, they are at around 1200 RMs and aim to make it 2000 in the next three years. This means a CAGR of 18.5% . Additionally, the revenue growth should outpace the growth in RMs as productivity increases. The second segment, Capital market too is expected to grow at around 2-2.25x in 3-5 years. A big driver of growth will be the asset management as the goal is to make the current AUM of 7000 7-8x in the next 5 years. Operating leverage will kick in as well. Hence, I feel like the growth assumed is moderate to conservative as there are a lot of levers of growth.

Cost to income

Nuvama is aiming to become a tech platform and one a stop solution. the Opex cost of the business will not be much in the coming years as the cost is already done before. The only cost that will rise steadily is staff costs as RMs are hired. Thus, Operating leverage will kick in as the variable costs are employee costs and their benefits.

The management has guided for Cost to income of 60% over the next three years, however it could be lumpy because that depends on the pace of hiring so keep that in mind.

Tax rate assumed is 24-25% as indicated in the past 2 FYs.

Anti thesis pointers

- Although I believe the story is structural, some of its elements of business are cyclical in nature and hence can lead to problems in revenue growth. For example, Capital markets which includes IB is highly cyclical and should be looked at with caution.

- a big part of their capital market revenue: it. is dependent on the volumes of contracts traded by big hedge funds and such companies. Volumes increase during a bull market so during a bear market, revenue and volume will go down.

- Nuvama Private caters to ULTRA HNIs who benefit a lot from IPOs and Real estate. Again, these are cyclical in nature

One thing to understand in operating leverage is if revenues do not grow, operating deleverage can. take place which is a possibility here so the PAT can fall drastically.

However, The management aims to keep a 75-80% of earning from Asset Management and Wealth Management which I believe are structural stories with elements of shallow cyclicality. If they succeed in doing this: rerating is possible and the worry of being cyclical goes away.

| Subscribe To Our Free Newsletter |