Transformer sector is one of the hot sectors these days due to shortage and strong demand from conventional and renewable sector. Bharat Bijlee is one of the lesser discussed names in the whole theme but a consistent performer. The company has posted very strong Q4FY24 results, possibly, the highest growth in the listed transformers’ space.

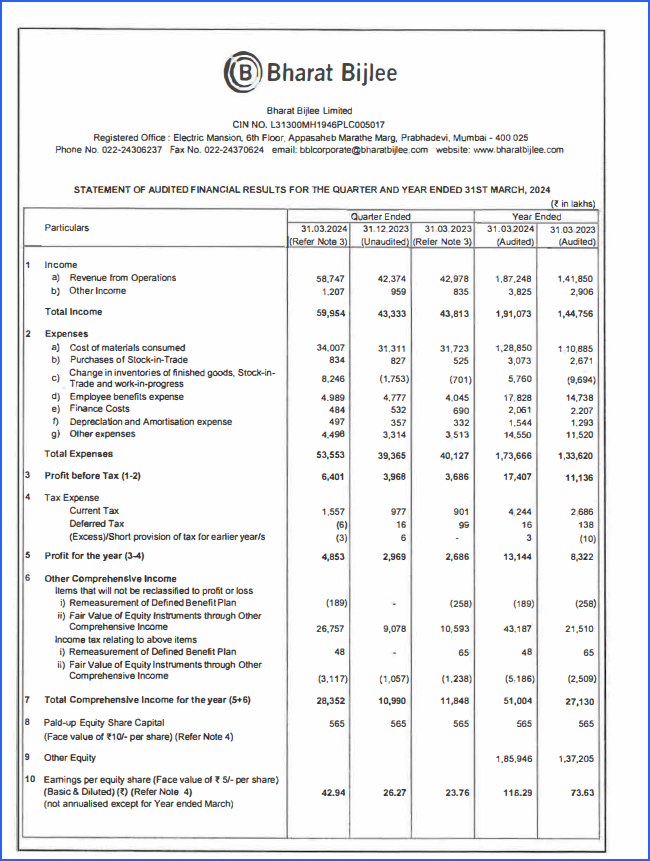

Net profit up 80.3% at ₹48.5 cr vs ₹27 cr (YoY)

Revenue up 36.7% at ₹587.5 cr vs ₹429.8 cr (YoY)

EBITDA up 58.5% at ₹61.5 cr vs ₹38.8 cr (YoY)

Margin at 10.5% vs 9% (YoY)

Net Cash flow from Operating Activities ₹241 crores

Dividend ₹35 per share (post split)

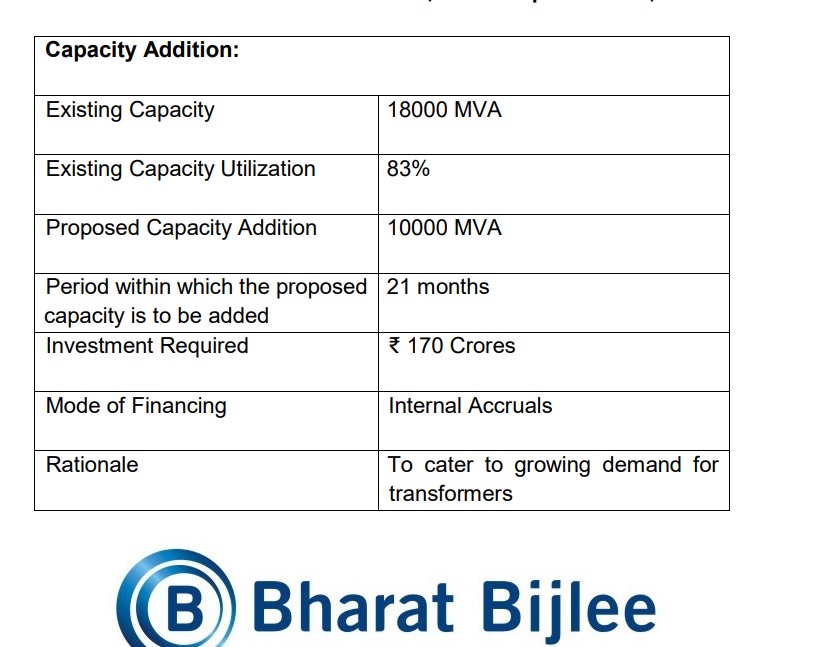

Company also announced capacity expansion from 18000 MVA to 28000 MVA for transformers to be funded through internal accruals

Current Market cap of the company is ₹4182 crores with a debt of Rs. 150 crores. Cash and cash equivalents stands at ₹380 crores as on 31st March 2024.

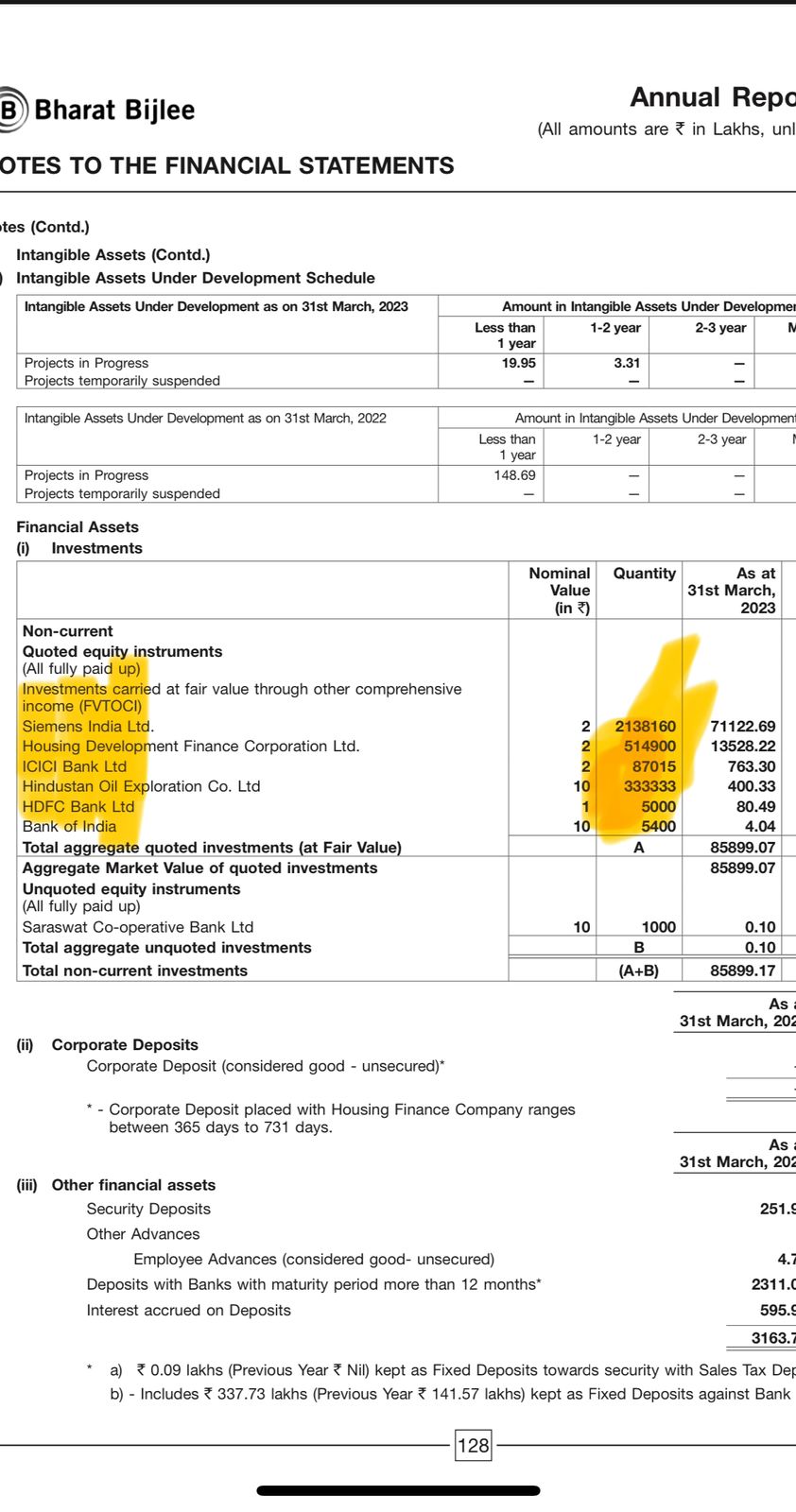

Interestingly, they have large equity investments, majorly in Siemens Limited and other listed companies which are valued more than ₹1700 crores as on today. They own more than 21 lakhs shares of Siemens Limited. So cash and investments are almost ₹2100 crores which is more than half of the current market cap. Enterprise value comes to around ₹2200 crores at EV/EBITDA of 12.

It is puzzling that with this much cash available what is the need of debt. It is also not clear as to what company plans to do with this much cash. Let’s hope company clears the air with better communication with the shareholders through concalls and presentations. With the growth and demands in the sector, Bharat Bijlee Limited seems to available at pretty cheap valuation when peers are trading at exorbitantly high multiples.

Disclaimer: Holding and biased.

| Subscribe To Our Free Newsletter |