The time has arrived (Again)

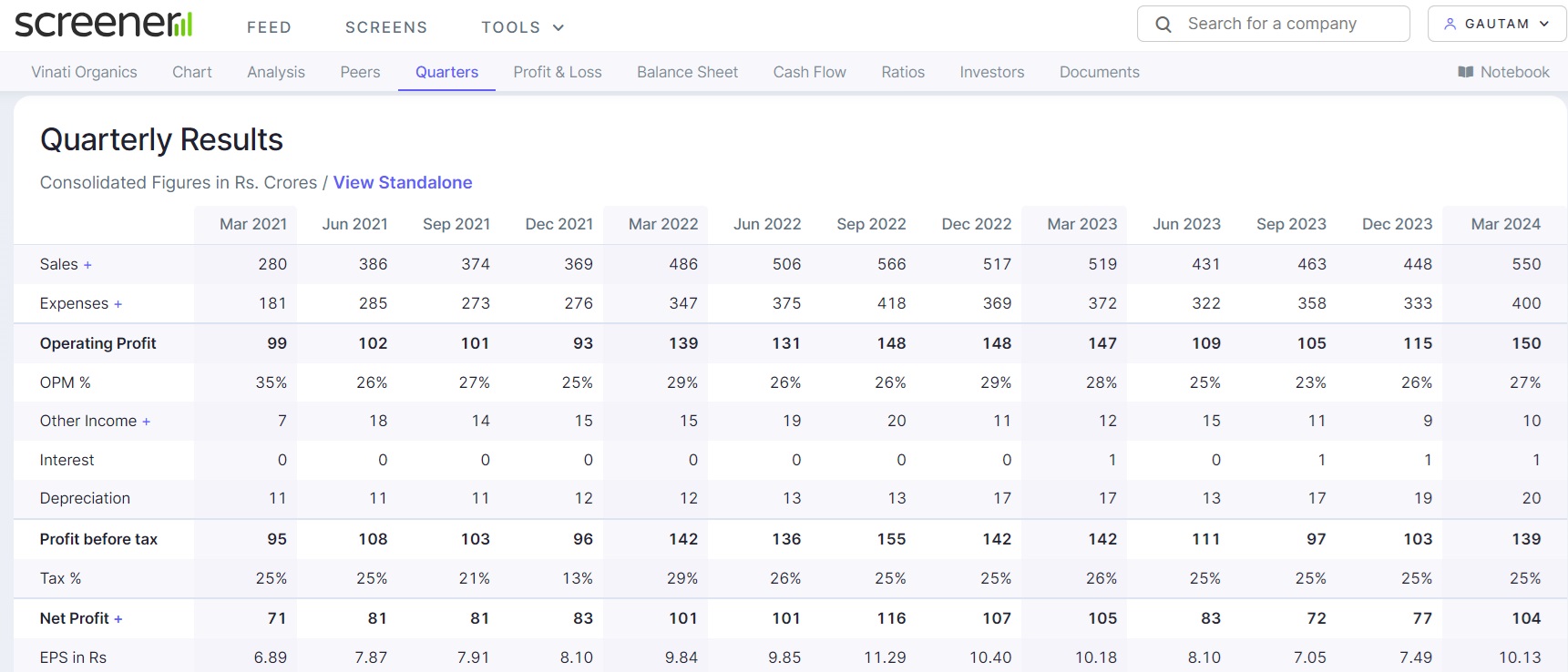

Vinati reported better than expected results in Q4FY24 with highest ever quarterly EBITDA. While YoY performance is flattish, there has been significant improvement sequentially. The company seems to be back on track after 3 quarters of weak performance. After 3-4 quarters of subdued demand in ATBS due to destocking by the customers, ATBS has shown strong recovery. Though the company has been diversifying into new products, ATBS still remains largest profit contributor.

Even if one conservatively assumes, no further sequential improvement in the quarterly profit for next 4 quarters, FY25 PAT could increase by 29% (to Rs.104.5crx4 = Rs.418 crore). There are further triggers for revenue and profit growth for forthcoming years due to expansion of ATBS (by 50% of existing capacity) as well as for few other products getting completed during FY25 and ramp up/recovery in other molecules.

Management has guided for 20% revenue CAGR for next 3 years and indication of stable EBITDA margins. This looks achievable with possibility of positive surprises in my personal view. The stock return has been zero during last 3 years due to subdued earnings, delay in expansion projects and significant jump in stock price in earlier years. However, worst seems to be already over and there is visibility of earnings growth resumption. TTM PE is 53x, 5-year median PE is 48, 10-year median PE is 36. Stock may optically appear expensive on TTM earnings (which were depressed); BUT demonstrated track record, cost leadership and more importantly visibility of decent earnings growth, make me positive about the prospects.

Disc: Invested. I am not SEBI registered Advisor/Analyst. My view may be positively biased. I am not suggesting any investment action. The information provided above is for education purpose only.

| Subscribe To Our Free Newsletter |