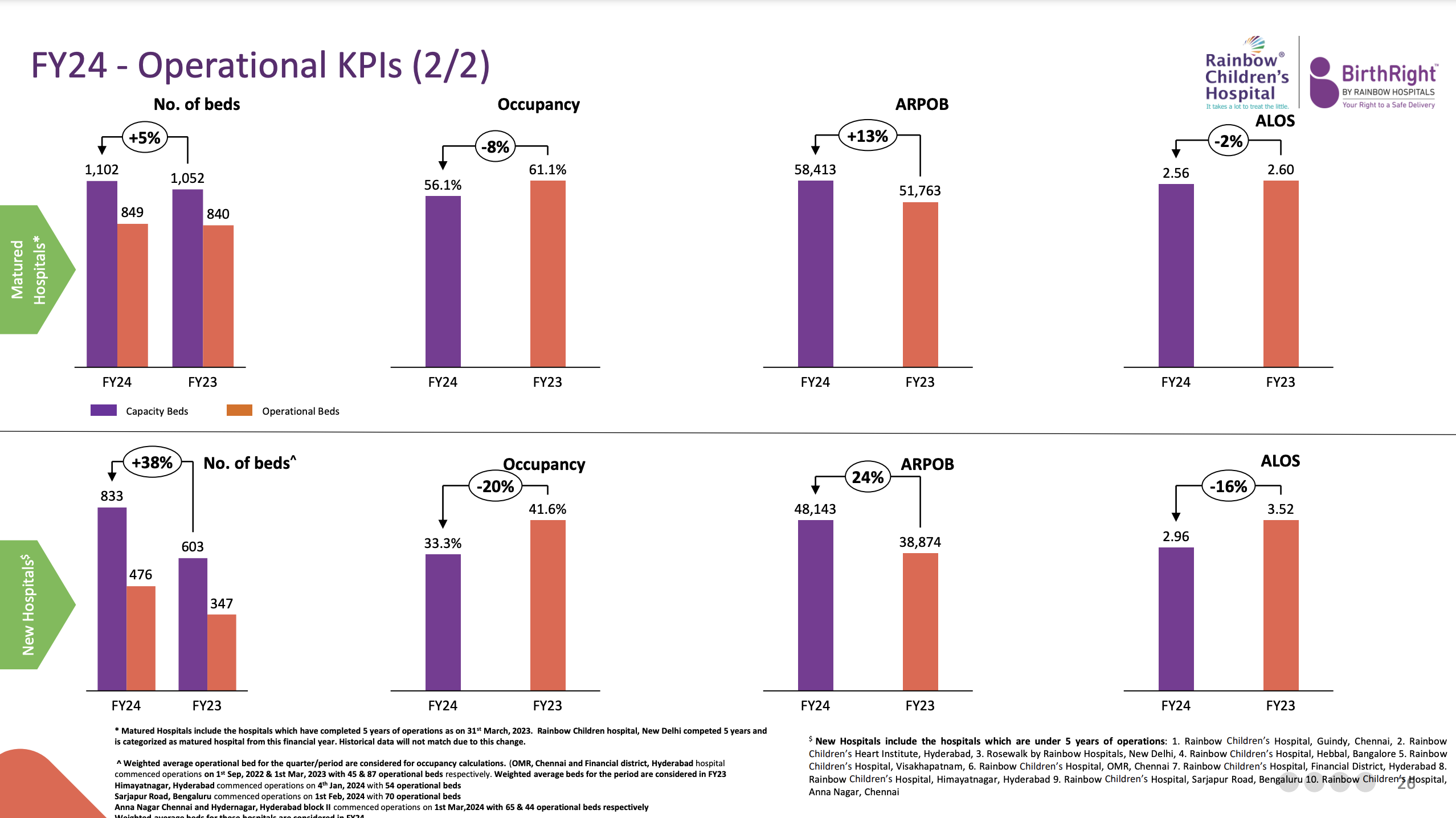

The main disappointment is around the growth in the matured hospitals. They had good amount of expansion and that was mainly in the new hospitals which is reflected in the bed count and occupancy and this is understandable as the cost is front ended in hospitals. But despite a good growth in ARPOB and some expanded capacity, the occupancy for matured hospitals dropped for various reasons.

EBITDA growth compared to revenue growth haven’t fallen off significantly and it is PAT growth that has dropped so no concern on the core business. This is mainly coming from additional depreciation due to front ended costs. A 15-18% topline growth is lower than the recent past (Last 3 years – 26%) so this signals a period of consolidation in the immediate coming quarters…?

Disc: Invested and biased. 3% of portfolio.

| Subscribe To Our Free Newsletter |