It was a milestone Q4 for Iris not only in terms of fantastic results but they crossed 100 Cr revenue for the first time this year. It is not only the growth in top and bottomline for Iris which is impressive, but also the quality of the earnings which comes across clearly from the concall which has been uploaded.

-

With EBITDA margin being 20%+ this quarter versus typically ~12% earlier, it is evident here how growth is leading to clear operating leverage. Even if the company continues to grow at a slower pace from now on, I believe the recent re rating is only a part of what the company deserves for such a transformation. Differences in valuations versus global and industry peers have already been highlighted earlier, and now, there is the additional element of fast growth in this business.

-

Whilst tracking this company since my investment in Nov’23, I have been very impressed by the management especially Mr. Swaminathan and Mr. Balachandran. This continues as all initiatives planning including prudent ESOP pool creation and hiring of top management (detailed below) is being delivered on. Additionally, I find it comforting that they are so conservative in their guidance. Results over the last 2 Qs have shown that this they like to underpromise and overdeliver.

-

Growth is Collect is mandate driven but it is fantastic. In the concall Mr Swami mentioned how still a majority of the world’s regulators (I think 70 countries) still need to adopt XBRL reporting, and this itself is a massive TAM ahead for the company. Additionally very good points were raised on how as they do more countries, they become much faster with specific reporting requirements that need to be built into the product depending on specific regulator requirements, as they have probably done it in another geography before. A large partner that left them in Europe to build their own product has also just joined them back realising the product strength of Iris Carbon.

-

Growth has also come in for Create this quarter and that is exciting as the SAAS growth trajectory could define a totally different future for an earlier mandate driven business. Even Mr Balakrishnan who is always very conservative to guide on growth showed a certain level of positivity on the concall for next year.

-

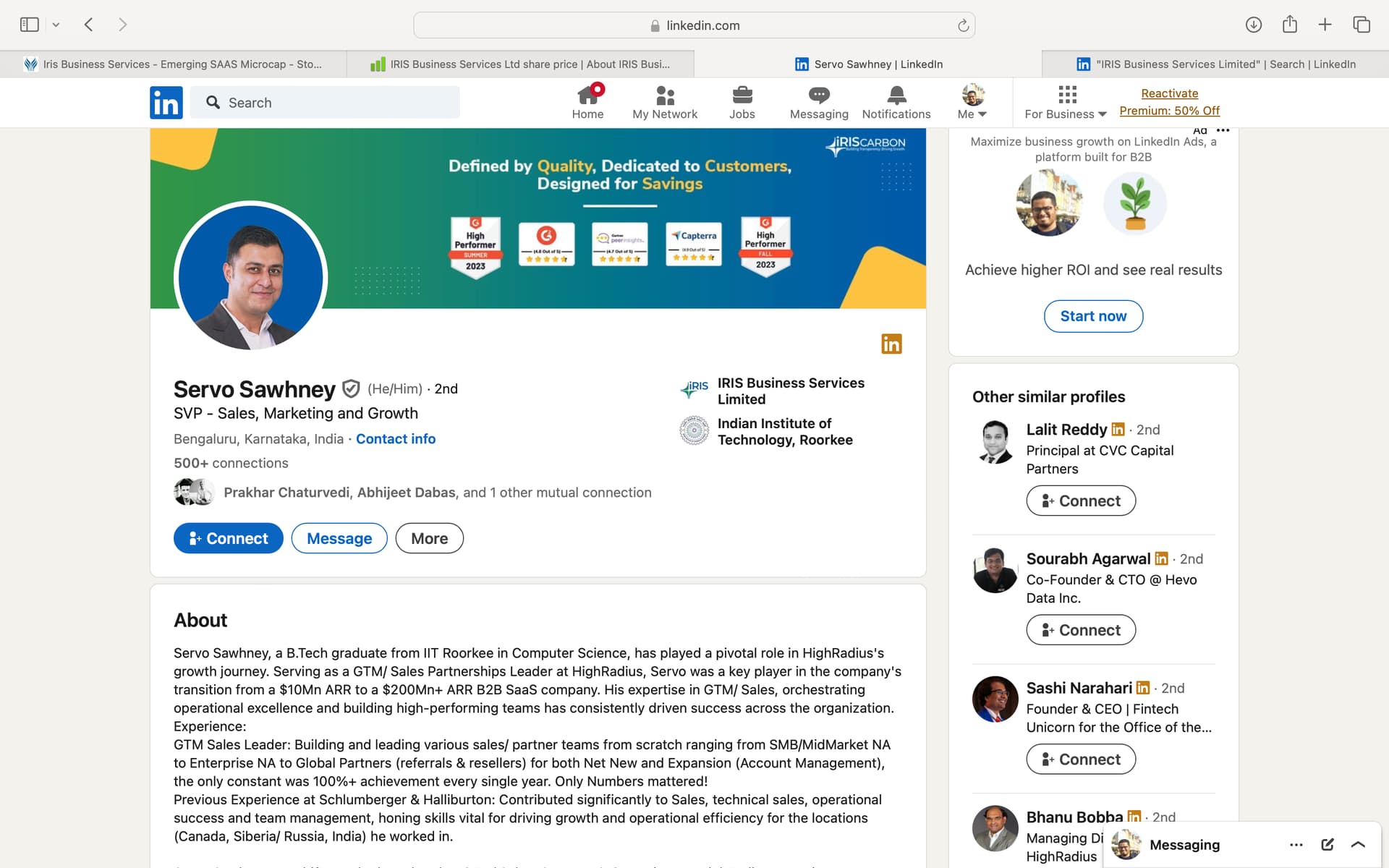

New senior leadership hire in Sales and Growth whose profile on LinkedIn looks impressive as per an initial glance and who was on the concall with some good answers. How he drives the business remains to be seen. Attaching a screenshot of his profile below.

-

Through the ESOP raising plan the company finally has a decent war chest to attract more leadership talent and expand. As the price has also seen significant appreciation, it finally also gives them headroom to raise capital when they need to as Mr. Swami was earlier rightly not doing so considering he did not feel market valuations at that time were ideal.

-

Apart from pricing and superior reviews on G2 which are very impressive, they also have a distinction versus Workviva which is they offer integration with MS Office for reporting which the competition does not. I like how the management thinks and differentiates and how they are gradually and surely tapping this niche growing market profitably.

-

Even at present this is at TTM 4.2x sales and TTM 26x EV/EBITDA for a niche product/SAAS business which has grown topline by 39% and EBITDA by 50% last year. Not as cheap as it was at 2.7x sales in Nov’23, but by no means does this seem crazily valued as well.

Disclosure : I continue to be fully invested in self and family accounts and have topped again slightly again today in family accounts. I am not a SEBI registered advisor and this is not investment advice. My view on the market is mostly to be in safety currently and be very careful at current valuations of several other companies, but considering that I value Iris higher in the long term, this is a rare case where in I continue to add to the investment rather than trimming.

| Subscribe To Our Free Newsletter |